Bad credit can be a hindrance for many finance options. When it comes to bridging finance, however, it's still possible to secure short-term bridging finance with a less than favourable credit score.

Throughout this guide, we will:

- Demonstrate that it is possible to secure bridging finance with bad credit

- Discuss how securing a bridging loan can help to improve your credit score

- Advise as to the criteria that you need to secure a loan with bad credit

- Explain how to secure a bridging loan with bad credit using innovative means like

- Brickflows bridging loan comparison tool

Read on to find out more.

Bridging loans explained

Bridging finance is a handy form of short-term funding, typically ranging from 1 to 12 months, that is mostly used to plug funding gaps between buying, selling, and refinancing a property.

One of the defining factors of bridging loans is that they are quick to organise, taking as little as three days depending on the scenario. Comparatively, other types of finance such as development finance, commercial mortgages, and residential mortgages take much longer to complete.

The amount that can be borrowed ranges from £10,000 to £10 million, providing resources for projects big and small. Bridging loans provide a versatile solution with a range of uses, these include the acquisition of land, the purchase of refinancing of a property, property refurbishment, developer exit, auction purchases and more.

To learn more, take a look at our dedicated bridging finance page.

Can you get a bridging loan with bad credit?

The short answer to this is yes, you can get a bridging loan with bad credit.

Although your poor credit situation may make it harder to secure a loan and you may have to pay slightly higher rates, bridging lenders are generally more interested in your exit strategy. If you are able to clearly demonstrate how they will be repaid, they are more likely to approve your bridging loan application. This makes factors such as credit history, income, or cashflow less important when compared to a residential mortgage for instance.

For example, if the intended use of the loan is to buy a house at auction, refurbish the property, and then sell it, the exit strategy is clear-cut, and a fixed completion date for the sale will bolster your chance of approval. The property acts as security in the event that you don’t secure a sale and default on the loan.

However, if the plan is to keep the property and remortgage, this would pose a much higher risk for a lender because obtaining traditional mortgages with bad credit can be difficult. Therefore, bridging loans for bad credit borrowers may not be approved in these circumstances.

Whereas some lenders will be willing to lend to applicants with bad credit, not all bridging lenders will, and some might stipulate a minimum credit score.

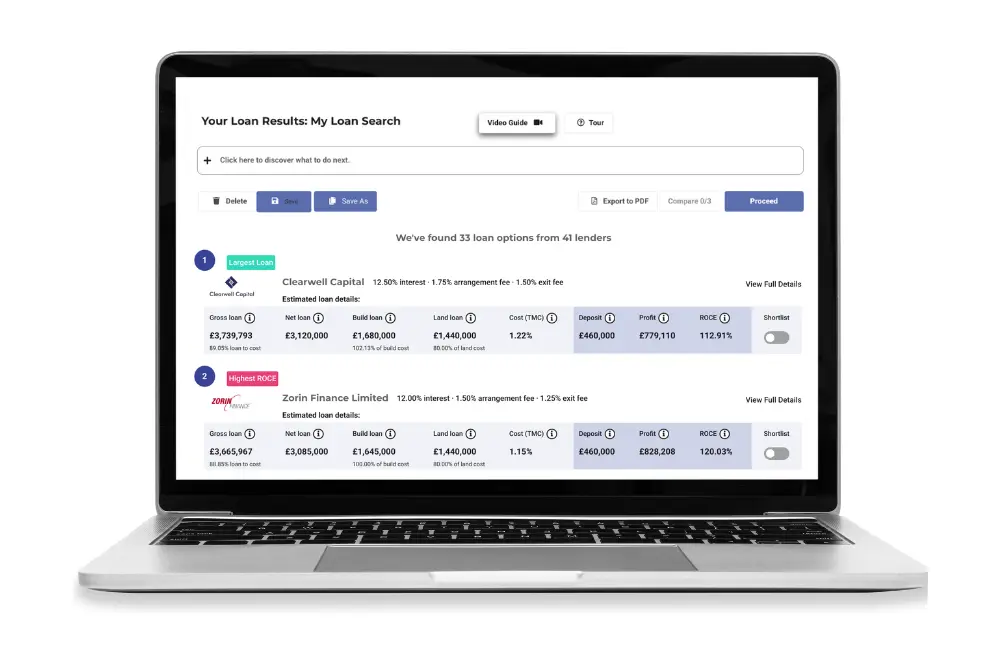

To narrow down lenders that suit your credit circumstances, use Brickflow’s live bridging finance calculator to compare bridging finance from over 50 UK bridging lenders, and filter out lenders that can’t meet your requirements.

Bad credit circumstances that bridging lenders may overlook

Getting the best bridging loan for your credit rating starts with finding the right intermediary. Every lender will differ, but many bridging lenders accept these credit problems:

- County Court Judgement (CCJ)

- Previous bankruptcy

- Defaults and late or missed payments

- Debt management plans

- Debt relief order

- Home repossession

- History of payday loans

- Low or no credit scores

Bridging loan requirements for borrowers with bad credit

As we’ve established above, the primary consideration for most lenders is your exit strategy. There are however other key areas that lenders will take into consideration before approving a bridging loan application. These include:

- The Borrower: You’ll need proof of identity, proof of address, and three months worth of bank statements. They’ll also look at your property portfolio and development experience.

- The Property: Lenders will carry out valuation reports (at your expense) of the purchase property and securing assets, to determine the value of the property in its current condition.

- Loan Purpose: Understand how the loan will be used. For instance, If it’s a commercial property, they will examine the business viability

- Exit Strategy: As we’ve covered above, they want to know how and when they’ll be repaid. Typically, exit strategies might include remortgaging, refurbishing and selling for profit (flipping), or clearing the loan with an alternative asset sale

- Deposit size: Deposit requirements are determined on a case by case basis, but most UK bridging loan lenders are limited to 75% LTV on a gross loan basis, meaning you will need a deposit of at least 25% of the property value plus interest costs and lender fees.

How much can you borrow with bad credit?

Lenders on the Brickflow platform offer bridging loans between £25,000 and £100 million. How much you can borrow depends on a few key factors, including:

- The value of the property

- The lender you apply to

- The maximum LTV available for your property

- The exit strategy

- Your net asset value and collateral

- How much capital you have available

Could a bridging loan help my credit history?

Paying off a bridging loan on time can positively impact your credit history, much like any debt repayment. Conversely, failing to repay on time will worsen your credit issues. This is why having a clear exit strategy and thorough lender scrutiny of your property proposal is crucial.

How much your credit score will improve depends on the severity of your credit history and efforts to improve it. A County Court Judgement (CCJ) can affect your credit for up to six years, and bankruptcy for up to ten years, so a three-month bridging loan will have minimal impact.

Your credit file helps lenders assess your borrowing behaviour and risk. Lenders want to know if you’ve borrowed under similar circumstances before. While a previous bridging loan may not significantly improve your credit score with agencies, it could make you more appealing to new lenders.

Next Steps: Securing a bridging loan with bad credit

Securing a bridging loan with bad credit is possible, and if you think it’s the right type of finance for your next property investment, run your numbers through Brickflow to find out how much you can borrow.

Use Brickflow

Leverage the power of technology and use Brickflows bridging loan comparison tool.

In a matter of seconds you can search over 50 bridging lenders, from banks to specialist lenders and compare live market options, including LTV’s, rates, fees and more.

Once you’ve found your deal, with your intermediary, or we’ll connect you with a Brickflow partner, you can secure the best bridging loan on the market. Our intermediary partners know the market inside-out and can help identify the right lenders for your current credit situation.