Borrower Tips

Commercial Mortgage Terms

Essential commercial mortgage terms to help borrowers make better decisions, compare lenders, and choose the best solution for their investment...

Borrower Tips

Borrower Tips

Are you considering applying for a commercial mortgage? One of the main considerations for many borrowers is the deposit amount needed. Whether you're expanding your business or investing in property, understanding deposit requirements is key to understanding if you are able to afford a loan, and secure the best deal possible.e.

According to recent trends, commercial mortgage demand is soaring as more investors jump on property opportunities. But how much deposit do you actually need? Getting it right can be the difference between securing a great deal or missing out.

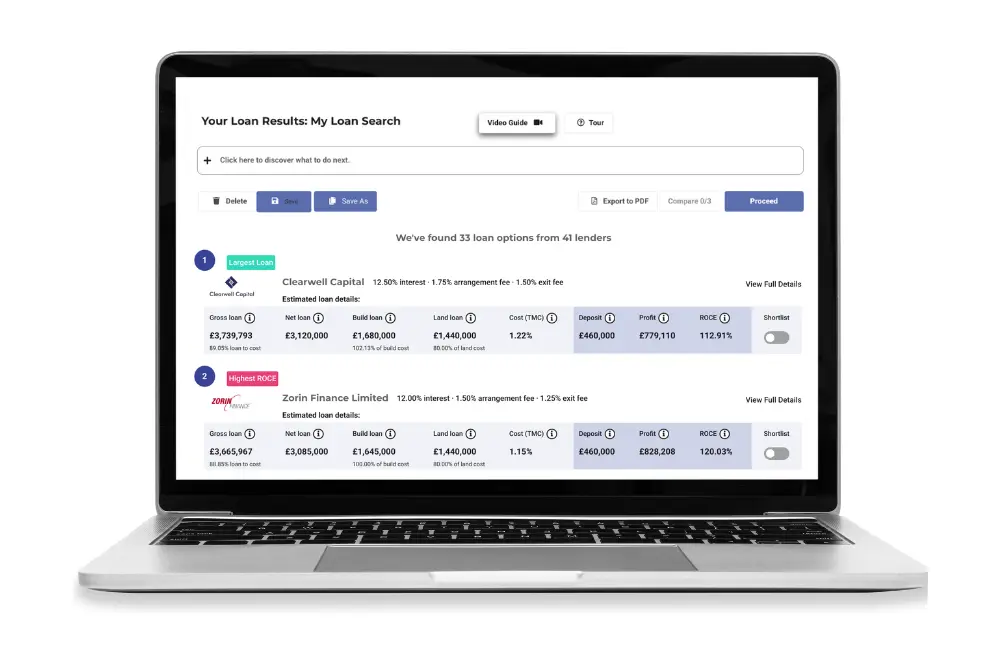

Let’s explore innovative ways that you can compare and identify the best commercial mortgage deal possible by using tools like Brickflow.

A commercial mortgage deposit is the initial sum of money that a borrower contributes toward the purchase of commercial property. This deposit helps secure the mortgage loan and reduces the risk for the lender. Think of it as the key to unlocking your mortgage loan. A commercial mortgage deposit is typically higher than a residential mortgage deposit because lenders perceive commercial properties to be riskier investments.

Unlike residential mortgages, which may require a deposit of as little as 5-10%, commercial mortgage deposit requirements are usually between 20% and 40%, depending on the lender and the property type. The larger the deposit, the more likely it is that you will secure better interest rates and terms.

But here's the good news: It’s often the case that the bigger your deposit, the better your chances of securing a great deal with lower interest rates and more favorable terms. So, putting down a bigger deposit not only secures the property but can also unlock better opportunities for your future investments. However, there are lots of factors that contribute to what offer you receive. It’s all about stacking the odds in your favour!

So, how much deposit do you need for a commercial mortgage? The amount typically varies based on the Loan-to-Value (LTV) ratio. Lenders usually prefer an LTV ratio of 60-80%, meaning you would need to pay a deposit of 20-40% of the property value. This can vary depending on the property type, the borrower’s financial health, and the lender’s specific criteria.

For example:

While these numbers might seem daunting, they’re not set in stone. Some lenders offer more flexible options, and government-backed schemes can sometimes reduce upfront costs.

The key is knowing where to look — and that’s where a tech-savvy, market-wide search comes in handy. Instead of wading through endless lender criteria, why not let Brickflow do the heavy lifting? Compare commercial mortgage lenders, understanding their respective criteria and the various deals that you’ll be able to achieve given your circumstances. The best thing about all of this, using Brickflow’s platform reduces a process from weeks to minutes!

Several factors can influence the deposit amount for a commercial mortgage, and understanding them can help you secure the best deal possible.

Each of these factors plays a crucial role in determining the final deposit amount. It’s important to remember that there’s no one-size-fits-all rule, with each project unique in so many ways. With the right lender and deal structure, you can secure more favourable terms, so make sure to discuss this with your broker. Chances are, they’ll be using the Brickflow platform, which will allow them to scour the length and breadth of the commercial mortgage market to find you a solution that is tailored to your needs.

Paying a larger deposit can work wonders for your wallet—and your property investment goals! Here’s why:

For savvy property investors, these perks make a larger deposit a no-brainer. It’s not just about securing the best deal—it’s about setting yourself up for long-term success!

If you don’t have the full deposit required for a commercial mortgage, there are still options available to you:

A question that our team is often asked is "Can I buy a commercial property without a deposit?" Whilst it’s rare, some lenders might offer deals with minimal deposit requirements for strong candidates or high-value properties.

Raising the necessary deposit for a commercial mortgage may require some creative thinking and financial discipline. Here are a few practical tips:

Navigating the commercial mortgage deposit process can be daunting, but Brickflow simplifies the experience. Brickflow’s platform connects borrowers with lenders across the length and breadth of the market, allowing you to identify those that are offering competitive deposit requirements and flexible terms. Whether you're a first-time buyer or an experienced investor, Brickflow’s intermediary partners can quickly match you with the best deals.

Try Brickflow's Commercial Mortgage Deposit Calculator to get a better understanding of your deposit requirements. Using the Brickflow platform allows you to find tailored financing solutions that fit your specific property needs.

To recap, understanding commercial mortgage deposit requirements is key to securing the best financing for your property. Whereas a larger deposit can help you secure better terms and lower rates, alternative financing options like bridging loans or investor partnerships can help you overcome deposit challenges. It’s essential to fully understand the type of finance that you are agreeing to, including your obligations, before signing anything!

At Brickflow, we’re committed to helping you navigate the commercial mortgage process, providing you with the tools and resources you need for success. Start your journey with us today and take the first step towards securing the perfect commercial mortgage.

Ready to find out more? Check out Brickflow’s Best UK Commercial Mortgage Rates Compared, so you can secure the best deal for your project.

Essential commercial mortgage terms to help borrowers make better decisions, compare lenders, and choose the best solution for their investment...

Avoid costly mistakes in property development and investment with these six essential financial tips to optimize your returns and secure better deals.

How to find the best commercial mortgages by comparing banks & alternative lenders effectively, understanding deal specifics, and avoiding costly...