The UK bridging market is currently estimated to be worth a hefty £13.7 billion, as more property investors take advantage of the speed and flexibility of bridging finance.

Whether used as temporary liquidity or funding an entire property project, bridging finance is now a go-to financial solution across the industry.

Read on for bridging loans explained in simple terms, including how they work, when they can be used and their risks and benefits. Enabling you to explore all the finance options available for your next project and navigate the loans process smoothly.

What is a bridging loan?

A bridging loan is a short-term secured loan, typically up to 24 months, paid back with interest and commonly used in UK property transactions.

They can alleviate temporary funding gaps between buying and selling/refinancing property. A key feature of bridging loans is the speed at which they can be arranged; in some circumstances, it can take just a matter of days.

Bridging loans can also finance quick turnaround property projects, such as ‘fix and flip’ projects, fund land acquisitions, or facilitate a development exit.

Secured against the property being purchased and/or additional assets, in the event of a default, the bridging loan lender can repossess these assets.

How bridging loans work

Unlike homeowner mortgages, bridging loans are assessed against the asset values, the strength of the project/investment and the exit strategy (how the loan is repaid), rather than income and affordability.

Interest is typically charged daily and rolled-up, so at the end of the loan term, you pay back the amount borrowed plus the accrued interest. If a lender charges interest monthly, you’ll be charged for the entire month even if you exit part way through. Some lenders offer monthly servicing (pay the interest each month) but it’s not that common. Bridging loan interest rates depend on:

- The property value, type, location and market demand

- The loan to value ratio (LTV)

- Borrower profile (credit history, property investment experience, financial position)

- The exit strategy

Lenders assess the exit strategy through various layers of due diligence, such as independent valuations, market comparable research, quantity surveyor report on the project (if applicable), and borrower credit profile.

Examples of a strong exit strategy would be having a fixed date for a property sale completion, or having a mortgage in principle for a refinance.

How Lenders Assess Bridging Loan Applications

Bridging loan underwriting is primarily asset-led, not income-led, with lenders focusing on whether the property provides sufficient security and whether the exit strategy is credible and time-bound.

While most lenders do not require proof of income in the way a residential mortgage does, assessing a borrower's credit profile will still be part of the application process. If your exit is to refinance, but you have a CCJ or poor credit history, securing a mortgage can be difficult, making it problematic for bridging lenders to accept your exit.

Risk appetite varies significantly between lenders. Some will lend on non-standard properties (mixed-use, short leases, refurbishment), while others restrict lending to straightforward residential assets at lower LTVs. Borrower experience also matters: seasoned investors may access higher leverage or flexible terms due to proven delivery.

Typical bridging loan amounts

There is no specific typical amount for bridging loans. Lenders on the Brickflow platform offer bridging finance across a vast scale, stretching from £25,000 up to £350 million.

The loan amount will depend on the value of the asset/assets, the amount of deposit input from the borrower and the lender’s LTV (Loan to Value) caps.

Bridging Loans for Commercial and Development Property

Bridging finance is widely used beyond residential purchases, particularly for commercial and development-led transactions.

Typical scenarios include:

- Commercial purchases (offices, retail, industrial, mixed-use) where the property is vacant, partially let, has short leases, or requires repositioning before long-term commercial mortgage finance is available.

- Refurbishment or change-of-use projects, where works prevent immediate mortgage eligibility (e.g. converting office to residential, fix and flip projects, improving EPC ratings, or securing planning).

- Development exits, using a short-term bridge to repay development finance while units are sold.

Assessment differs from residential lending because decisions are based on asset value, commercial demand, and the exit timeline, not personal income. Lenders analyse lease terms, market rents, planning risk, and resale liquidity.

Read more about commercial bridging loans here.

What are the criteria to get a bridging loan?

While monthly income and outgoings don’t play a huge part, there are still certain bridging loan criteria that borrowers need to meet to get a loan.

Basic criteria include being aged 18+, a UK resident with proof of address and ID, and employed / self-employed / retired.

Loan approval is always down to lender discretion, so even if all criteria are met, there are other factors that can influence a lender’s decision, including:

- Loan amount: Minimum considered is £25,000, but lenders are more likely to engage on loans applications of £150,000+

- Property type: Suitable collateral required (usually property) equal to the value of the loan. Not every lender will consider loans for every property type. Credit score: As an asset-secured loan, credit history is less important than with residential mortgages, but having clean credit can help to secure better rates or bolster an application.

- Proof of income: Bridging loans are typically repaid in full at the end of the term, so a fool-proof exit strategy rather than strong income/affordability is key, but likewise, it can help to bolster an application.

- Deposit: Most lenders offer a maximum of 75% gross LTV. Interest and fees will be deducted from the gross loan (unless you're servicing the loan), but deposits of around 40% can help secure better rates.

- A clearly defined exit strategy

Full eligibility criteria is explained here: Who Can Get a Bridging Loan? Eligibility and Criteria.

How People Access Bridging Loans

Borrowers typically access bridging finance through one of three routes:

- Direct to lenders

Some borrowers approach lenders directly. This can work for straightforward cases but limits access to the wider market, as each lender has fixed criteria around property type, LTV, and exit strategy.

- Specialist brokers

Brokers assess the deal and place it with lenders whose underwriting appetite fits the asset, works, and exit. This is common for complex cases involving refurbishment, commercial property, or tight timelines.

- Finance platforms

Brickflow is the leading market platform for specialist finance, providing instant access to the bridging loan market so you can compare multiple bridging lenders side-by-side, filtering by criteria like asset class, leverage, and exit type.

Bridging loan pricing is not inherently cheaper or more expensive through any channel. Rates and terms are driven by risk, leverage, asset quality, and exit certainty, not how the loan is accessed. However, Brickflow enables you to shop the breadth of the market and source all deals available for your needs which inevitably leads to cheaper, or better funding.

How bridging loans are arranged

If you think a bridging loan is the right option:

- Shop the market: Before applying to any lender, it’s crucial to shop the breadth of the market. There are hundreds of bridging loan lenders, from banks to specialists, all offering different products, fees and rates.

- Application: Prepare your documentation, including ID, proof of address, financials, CV, etc., and create a professional presentation of your project (if applicable) and how the loan will be used.

- Approval: When the lender has all the necessary information, they complete the underwriting process and formally offer. Respond to any request from the lender promptly. Solicitors are engaged on both sides, and your loan manager (broker/intermediary) will ensure you’re happy with the loan T&Cs.

- Receive funds: Once approved, funds are transferred, typically on the same day.

Bridging lenders are equipped to process loans quickly, with the typical timeframe from application to loan drawdown being 2-4 weeks. Loans can be completed in a few days when lenders use Automated Valuation Models (AVMs), or ‘desktop valuations’, and forgo legal searches in favour of title indemnity insurance. Lenders typically only use this when lower leverage is requested and there is little to no renovations to be done.

How long do you get to pay back a bridging loan?

The typical loan term for bridging finance is 1 – 24 months for unregulated bridging loans, and up to 12 months for regulated bridging loans. (Regulated bridging loans, explained in short, are where the loan is secured against the borrower’s or their immediate family’s main home or a property that they will use as their home in the future).

On Brickflow, some lenders offer terms up to 30 or 60 months, though these are less common and only apply in certain circumstances.

Common use cases for bridging loans

Some common examples of bridging loan uses case:

-

Property chain breaks: If one buyer or seller pulls out of a property chain, bridging finance can enable the purchase of the new home to continue before the completion of the sale of your existing home.

-

Buying at auction: When buying at auction, you are typically required to pay a 10% deposit upfront and complete the purchase within 28 days – traditional finance can’t meet this short timescale.

-

Acting fast: Prime sites at good prices will naturally attract many buyers. With a fast bridging loan, you can act as a cash buyer to secure a faster sale and pip the competition.

-

Renovation projects: Smaller-scale projects that don’t require planning permission can be funded with refurbishment bridging.

-

Buying land: Funding a land purchase can be pretty difficult using traditional financing routes. Planning bridging can facilitate the purchase of a site with or without planning and partially cover associated pre-construction costs involved in property development.

- Development exit: For development projects at PC (Practical Completion), development exit bridging can enable you to extract equity and move on to another project or repay the development finance lender if your project overruns to reduce the pressure on sales.

Often, bridging loans are explained as a temporary funding solution in between buying and selling property. However, they can be far more pliable and used for a myriad of property transactions.

Pros and cons of bridging loans

Bridging loans explained without covering potential downsides can’t help you make informed finance decisions. In addition to understanding the benefits and how to use bridging finance, there are risks to be aware of.

Below is an overview of the upsides and downsides involved, but you can read more in-depth about the pros and cons of bridging loans here.

|

Pros

|

Cons

|

|

Creates market opportunities

|

Short-term only

|

|

Can complete quickly

|

Higher interest rates and fees compared to traditional borrowing

|

|

Interest deducted upfront or paid on loan redemption, beneficial for borrowers with low disposable income

|

Compounded interest, so interest is paid on interest

|

|

Typically no exit fees or early repayment charges

|

Higher default interest rates if the loan is not repaid by the end of the term

|

|

Available for residential, commercial, land, properties that don’t qualify for traditional mortgages

|

Requires a personal guarantee (if borrowing through a corporate entity), leading to personal liability for the debt

|

|

Unregulated options provide lender flexibility and faster arrangement, whilst regulated bridging enables borrowing for your own home

|

Regulated bridging can take as long as a residential mortgage to arrange due to more stringent criteria and bureaucracy

|

|

Applications focus on property value, project viability, and securing assets, so poor credit, low income, or cash flow issues are less of a barrier to approval

|

Potential repossession of assets in case of default |

How Brickflow can help

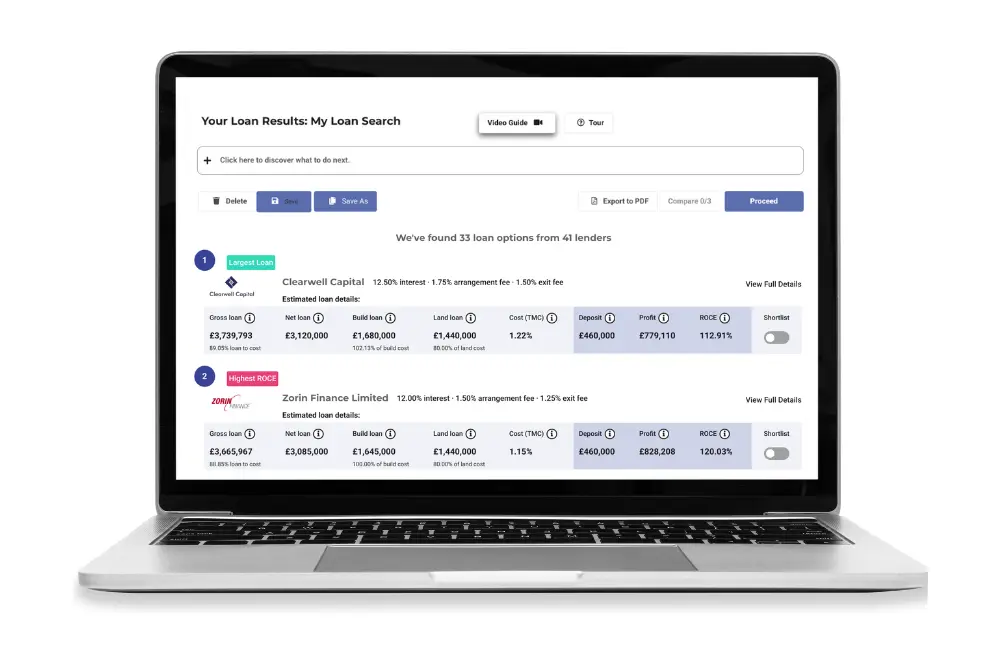

Brickflow’s bridging loan calculator offers the quickest, most efficient way to shop the breadth of the bridging loan market, delivering real-time loans from a network of trusted lenders, from banks, non-banks and specialist lenders.

Knowing your borrowing costs up-front is game-changing for any property investor or developer, as it prevents you from pursuing projects with a profit margin that is too small or altogether unviable.

Our award-winning tech, combined with a specialist broker, can help you to secure the best loan on the market quickly and easily.

Next steps: Ready to explore bridging loans?

Now that you know all about bridging finance, it’s easier to understand how they work and how they could benefit your next property investment.

To determine what bridging loans are available for your next project, run your numbers though Brickflow’s bridging loan comparison tool. It takes seconds and could save you tens to hundreds of thousands of pounds.

For bridging loans explained in more detail, you can read our other articles:

FAQs

How much interest will you pay on a bridging loan?

Interest rates for bridging loans vary depending on several factors:

- The market and the Bank of England base rate (for lenders pegged to base rates)

- The loan-to-value ratio

- The loan term

- The property type and condition

- The project, if applicable

- The exit strategy

The quickest and most accurate way to find out how much interest you will pay on a bridging loan is to run your numbers through Brickflow’s live bridging loan calculator. It takes seconds and enables you to see actual interest rates and charges on loans from across the market.