There are numerous ways to finance property investments, from buy-to-let and commercial mortgages, to development finance. Another financing solution that has become a critical component in the UK investor or developer's financial toolkit is bridging finance.

From seasoned property professionals to first-time developers, bridging loans provide a short-term financing solution, usually up to 24 months, helping to alleviate any immediate funding gaps. They are generally used in the buying, selling, and refinancing of property.

In the article below, we explore bridging loan pros and cons, and the risks involved when using this type of finance, providing you with the information you need to make an informed decision.

What are the benefits of a bridging loan?

So let's begin with the all-important question - what are the benefits of a bridging loan?

The most notable bridging loan benefits are:

- Quick arrangement, from 2-3 days – 4 weeks, with c. 14 days being most common for a bridging loan to complete in the UK. Find out more on our ‘Fast Bridging Loans’ page

- Alleviates funding gaps when buying, selling, or refinancing a property

- Provide borrowers with an immediate cash injection

- Bridging loans can be unregulated, meaning less bureaucracy to get through

- Enables purchase of properties that would be ineligible for regular mortgages, such as uninhabitable housing (no kitchen and bathroom facilities)

- Ensures homeowners don’t miss out on their dream home due to a broken property chain

- It can be used for both commercial and residential properties

- Doubles up as auction finance, where completion times are as short at just 28 days

- No early repayment charges (although some bridging lenders may include a minimum loan term)

- They can be used as an effective tool when purchasing land. To find out more, take a look at our land bridging loan page

- Provide property developers with a quick solution when looking to raise finance for property refurbishments)

Having access to this kind of fast, flexible financing offers property investors more flexibility in their decision-making, creating more opportunities.

Most people will be aware of the UK’s housing shortage – bridging loans can get development moving and add property options to the market. Uninhabitable properties that sit neglected for years can be transformed in months if developers can access the right finance.

Furthermore, considering the short-term nature of bridging finance – between 1 and 24 months – bridging loans promote a quick turnaround of sites, getting property to market sooner.

Bridging finance also allows developers to grab a good deal, like when a prime site is reduced for a quick sale. Moreover, bridging loan lenders approve applications based on the property value and viability of the project rather than the borrower’s capacity to make the repayments. So, if a developer has prepared a viable financial plan, low-income or cash-flow shortages shouldn’t prevent them from securing funding and completing a scheme.

To learn more about securing a bridging loan, take a look at our guide, which covers the eligibility requirements needed to secure a bridging loan.

What are the Cons of Bridging Loans?

With such an extensive list of bridging loan benefits, it’s also good to understand the flipside and ask what the cons of bridging loans are.

The most notable bridging loan cons are:

- Higher borrowing costs: Bridging loans are quick and convenient finance arrangements, so lenders charge accordingly. Interest rates tend to be high in comparison to other funding options. However, borrowers have options for repaying the interest, including paying monthly or opting for rolled-up interest that's paid at the end of the loan.

- Secured loans: Bridging loans are secured against an asset, usually property. Additionally, all bridging loans require a personal guarantee, meaning the borrower has personal liability. If the borrower defaults, the lender can force the asset to be sold. If there's a shortfall between the property's selling price and what the lender is owed, they can call on the personal guarantee, potentially resulting in the loss of other assets.

- Unregulated loans: While unregulated loans allow for fast completion times, flexibility, and accessibility for those with less-than-perfect credit, they come with risks. Unregulated borrowing arrangements lack the protections the Financial Conduct Authority (FCA) provides. A regulated bridging loan process gives borrowers protection if they are sold an unsuitable product or receive incorrect advice from lenders or brokers, with possible compensation for eligible cases. When bridging loans are unregulated, they have none of this protection.

- Short repayment period: Bridging loans are specifically designed as a short term finance solution. Extending beyond the agreed term or re-bridging can be costly.

While the answer to 'What are the cons of bridging loans?' is shorter than the pros, they must be considered by anyone taking out bridging finance.

Additional risks of using a bridging loan

When it comes to property, it’s more common than not for refurbishments or developments to overrun, for sale completion dates to get pushed back or finance arrangements to get held up. On top of that, the property market can change overnight, reducing projected sale values.

What happens if a borrower can’t repay their bridging loan on time depends on the bridging loan lender, the T&Cs of the loan and the circumstances of why the timeline has slipped. Some bridging loans can be extended if a sale is delayed, but will incur further fees and increased interest charges.

If a borrower goes over the loan term without communicating with the lender, they will likely face penalty charges, potential harm to credit scores and a faster repossession process.

What are bridging loans commonly used for?

The question that interests most developers is, what are bridging loans commonly used for?

Bridging loan finance is a highly versatile form of funding that can be used for many purposes across residential, commercial or semi-commercial properties. More commonly, they are used to bridge funding gaps between the buying and selling of property – hence the name.

Typical examples where bridging loans for residential property would be used include:

- Buying or building a new home before selling the current one

- Broken property chains

- Investors looking for a fast financing solution to secure a property that has been purchased at auction (often within 28 days of purchase)

- Uninhabitable properties (no working kitchen or bathroom) that are ineligible for traditional mortgages

- Funding substantial property renovations that can be completed in a short time, rather than applying for a full development finance package

- To take advantage of market conditions, like a reduction in price on land or a site

- Buying land pre-planning, or varying existing planning, before selling for profit or converting to a development loan to build the project yourself

- Fund property refurbishments using a refurbishment bridging loan

There are also some additional uses where a bridge loan mortgage could be applied in commercial transactions:

- Brownfield sites or run-down commercial premises that might not be eligible for traditional mortgages

- Buying new business premises before selling the current one to allow an uninterrupted business transition

- Funding a start-up venture

- Providing a business with working capital

- Buying equipment and machinery

- Financing tax liabilities

When a bridging loan may not be suitable

Bridging loans are powerful tools in specific situations, but there are times when they may not be a suitable solution.

Examples include:

Unproven or conditional exit strategy

Being reliant on future planning consent, speculative refinancing without a lender in principle (especially where poor credit is an issue), or open-market sales with no defined timeframe introduce uncertainty that lenders will either price heavily or decline.

Likewise, properties with non-standard construction, limited resale demand, or characteristics that make them difficult to mortgage can restrict both buyer demand and refinance options.

Unpredictable project timelines

Schemes involving major structural works, complex planning consent or several third-party dependencies will often overrun, leading to default interest, extension fees or the need for a costly re-bridge.

Borrowers with limited experience and no specialist support

Bridging lenders expect accurate costings, realistic timelines and a clear understanding of risk. Small misjudgements can have disproportionate consequences.

How to get a bridging loan?

The number of lenders offering bridging finance has increased to meet the market's growth, so it’s essential to understand how to get a bridging loan properly.

Most bridging loans are limited to a maximum of 75% loan to value (LTV), with the amount loaned depending on the property type and business plan for that asset. Typically, higher deposits and better LTV make securing a bridging loan easier, and usually with better terms.

The key to any application is providing concrete assurance to lenders that it can be repaid, i.e., there’s a valid exit strategy. Therefore, the borrower must know from the outset whether they will sell or refinance after the works are completed.

The steps to apply for a bridging loan are:

- Determine the type of bridging finance: Decide whether residential, commercial, or semi-commercial bridging finance is most appropriate for your needs. If you’re not sure, get in touch with our team, who will be able to help

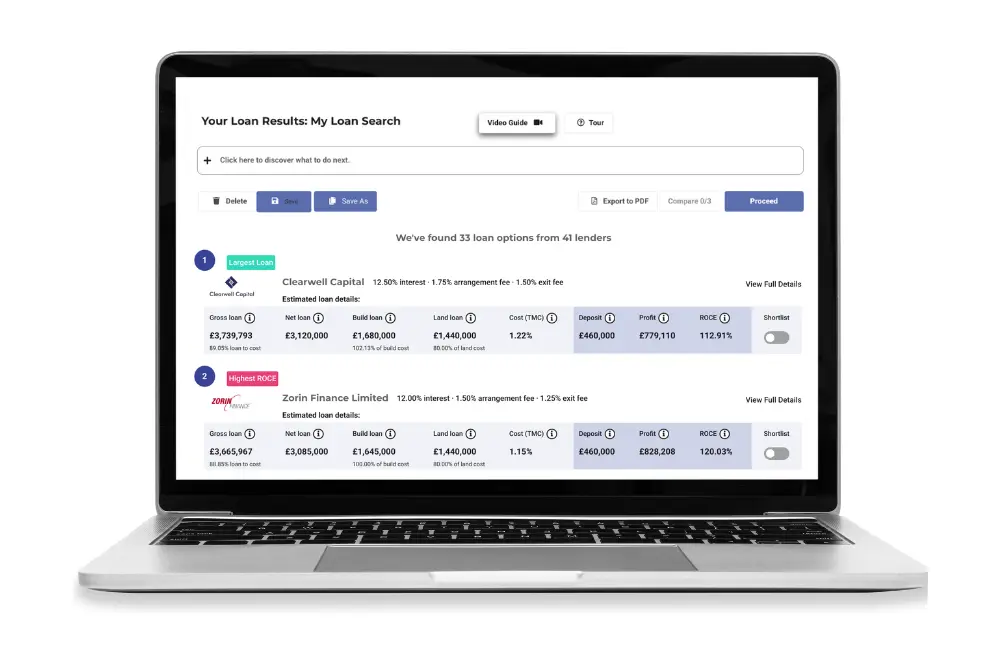

- Determine how much you need to borrow: Using a tool like Brickflow’s bridging loan calculator will help you compile all the necessary information for the next step. It compares over 80 bridging finance lenders across the UK market, ensuring you find a solution that suits your needs

- Prepare a detailed presentation: Show relevant experience and exact details on how the loan will be used to deliver a profitable outcome. Ensure building costs, timescales, and selling prices are realistic – lenders know the industry, so fudging prices will lose lender trust (and interest). If the loan doesn’t cover all costs, provide cashflow information to show how the exit strategy will be reached

- Ensure a valid exit strategy: The borrower must know from the outset whether they will sell or refinance after the works are completed. This assurance is crucial for lenders.

Next steps?

If you’re in the market and looking to secure a bridging loan for your next project, use Brickflow's bridging loan calculator to understand how much you can borrow whilst also identifying the best deals across 80+ bridging lenders in the UK.

If you’re keen on learning more, take a look at our bridging finance page, which provides a detailed explanation of bridging loans. Alternatively, feel free to contact our team who are more than happy to answer any questions you might have.