Timing is everything when it comes to bridging loans. Whether you're buying at auction, renovating a property, or covering a short-term cash gap, fast access to funding is key.

So, how long does it actually take to get a bridging loan? In many cases, funds can be released in as little as 48 to 72 hours, but more commonly, the process takes 1 to 4 weeks. For regulated loans, such as residential purchases, it can take 6 weeks plus.

In this guide, we’ll break down what affects bridging loan timelines, what can slow things down, and how to move things along quickly. You’ll also learn how to prepare your application for speed and how Brickflow can help you secure a bridging loan with minimal hassle.

How quickly can you get a bridging loan?

Bridging loans are a form of short-term finance designed to ‘bridge’ a gap in funding when you're waiting for long-term financing. Whether you're using a bridging loan to buy a property or fund renovations, speed is usually the whole point. . But just how fast can you expect a bridging loan to be approved?

Whether you're using a bridging loan to buy a property or fund renovations, speed is usually the whole point.

In the UK, a bridging loan can complete in as little as 48 hours in the right circumstances, typically where the loan is unregulated, the lender accepts automated valuations and title insurance, and the exit strategy is clear.

Most UK bridging loans complete within two to four weeks, with regulated bridges taking four to six weeks due to FCA compliance requirements. The biggest factor affecting speed is how quickly you identify the right lender from the 200+ active in the UK market.

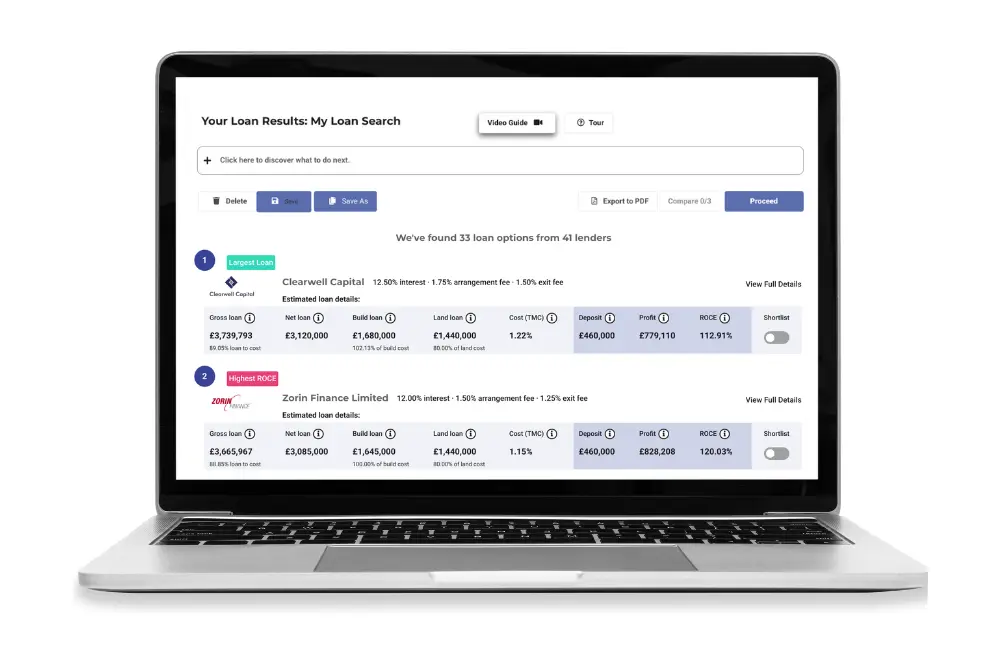

Brickflow removes that bottleneck: search 160+ UK bridging lenders in under 60 seconds, receive same-day DIPs, and apply to multiple lenders simultaneously through Smart Appraisal, so the lender search takes minutes rather than days.

Typical Bridging Loan Timeframes

The speed of approval varies depending on the lender and your specific circumstances.

For standard bridging loans, the process might take anywhere from 1 to 4 weeks, the latter end when more checks and paperwork are involved. If the loan is regulated, such as when you’re purchasing a residential property, it can take 6 weeks or more, similar to the timeframe for a traditional mortgage.

In the best-case scenario, funds can be released within 48 to 72 hours. If you need a fast bridging loan, use Brickflow's bridging loan calculator to find the right lender in seconds. Your broker can then secure the best deal for you, fast.

When Can Bridging Loans Be Processed in 48 Hours?

In certain scenarios, bridging loans can be processed extremely quickly, such as:

- Unregulated loans: If you're borrowing for property development or buying land without planning permission, approval times can be much faster. These loans are often unregulated, which simplifies the process. If you’re buying from an auction, a bridging loan can be used to secure the property quickly.

- Simple property transactions: If the property is straightforward, with no legal complexities or major issues, and you have all your documentation in order, you could receive a bridging loan approval, meaning a formal lender agreement in principle, within 48 hours from the time of application submission.

To find out more, take a look at our guide that discusses fast bridging finance in detail.

How to Speed Up the Bridging Loan Process

While certain factors may be out of your control, there are several ways to expedite the bridging loan process:

- Choose a Fast Bridging Loan Lender: Some lenders specialise in fast bridging loans and can process your application more quickly.

- Use a Specialist Broker: Working with a specialist broker or platform can help you find the best lenders who are equipped to approve loans quickly.

- Prepare Documentation in Advance: Having all your paperwork ready to go will prevent unnecessary delays.

- Provide a Clear Exit Strategy: Lenders want to know how you’ll repay the loan. The more detailed and realistic your exit strategy, the faster the process will be.

Step-by-step bridging loan application process

The process of applying for a bridging loan typically involves several key stages. Understanding what happens at each step and how long each phase takes will help you navigate the loan application more efficiently.

Step 1: Initial Enquiry and Pre-Approval

The first stage of any bridging loan application is making an enquiry. During this phase, you’ll provide the lender with initial details about the loan, such as the amount you need and the purpose of the loan. The lender will then assess your eligibility and may provide a Decision in Principle (DIP), which gives you an indication of whether you’ll be approved for the loan.

This stage can take anywhere from a few hours to a few days, depending on how quickly the lender handles your enquiry. However, brokers on Brickflow can provide you with a Decision in Principle (DIP) in as little as 6 minutes. Start your search now to quickly find the best loan options for you.

Step 2: Application Submission

Once you’ve received your DIP, you’ll submit your formal application. This involves providing detailed financial information and documents, including proof of identity, proof of address, and information on your property and exit strategy.

The application submission typically takes around 1 to 3 days for you to prepare the necessary documentation.

Step 3: Property Valuation and Legal Checks

The lender will require a property valuation to assess the risk associated with the loan. This is usually done by a surveyor who will visit the property to evaluate its market value and condition. Additionally, legal checks will be carried out to ensure there are no legal issues with the property, such as disputes over title, and legal documentation will need to be drafted too.

Step 4: Formal Approval and Loan Offer

Once the valuation and legal checks are complete, the lender will review all the information and decide whether to formally approve the loan. If approved, you’ll receive a loan offer outlining the terms, interest rates, and repayment schedule.

Step 5: Completion and Funds Release

Once you’ve accepted the loan offer, the final step is completion, where the funds are released via your solicitor. This is when you can access the funds for your property purchase or project.

This usually takes 1 to 3 days, but again, delays can occur if there are issues with documentation or last-minute checks.

What affects bridging loan approval speed?

Several factors can influence how quickly your bridging loan is approved, including your financial situation, the property in question, and the lender you choose.

Common Reasons for Delays

- Incomplete or Inaccurate Application Information: If the application is missing key details or contains errors, this can delay the process.

- Property Valuation: A delay in scheduling or receiving the property valuation can slow down the approval process.

- Legal Issues: Properties with legal complications or unclear titles may require additional investigation, causing delays.

- Credit History: If you have a poor credit history, lenders may need to review additional documentation, extending the process.

- Changes in Financial Situation: Any changes in your financial situation during the application process could affect the timeline.

Additionally, more complex deals, such as those involving regulated residential properties, auction purchases, or properties with legal complications, often require extra checks and documentation.

While auction purchases should, in theory, be quick (typically requiring completion within 28 days), borrowers still need to secure funding within that timeframe, which makes efficiency absolutely critical.

If you're working with a lender who is managing a high volume of applications or has a backlog, this can further delay decision-making. These factors can increase the overall time it takes to secure approval, so it's important to plan for potential delays when navigating more intricate loan scenarios.

How Lenders Assess Risk and Eligibility

Lenders use a combination of factors to assess the risk of your loan application, including the property’s value, your credit history, and your exit strategy. Some lenders have more stringent requirements than others, and this can affect how quickly they can process your application.

How Brickflow Can Help with Fast Bridging Loans

At Brickflow, we understand how important speed and efficiency are when it comes to securing a bridging loan.

Our platform allows your broker to compare a wide range of lenders in minutes, filtering out those who don’t meet your criteria so that you can find the best loan for your needs. Our brokers work closely with fast-moving, reputable lenders who specialise in bridging finance, ensuring that your application is processed quickly and efficiently.

Get Your Bridging Loan Processed Fast

Bridging finance offers a flexible, fast solution to a variety of financial challenges, but understanding the process and knowing how to speed things up is key to securing the funding you need. By preparing your documents in advance, working with the right professionals, and choosing the best lender, you can ensure a smooth, fast application process.

FAQs

Are bridging loans difficult to get?

Bridging loans are not inherently difficult to obtain, but they do require thorough documentation, a solid exit strategy, and a good understanding of the application process. Working with a broker or lender who specialises in bridging loans can make the process much smoother.