True Cost of a Development Finance Loan

Until you understand the actual cost of a development finance loan, you can’t accurately calculate profit, and therefore how do you know what the site is worth?

Any investor should concentrate on determining the residual land value, or fair value for the site before they make an offer.

The residual land value is calculated by subtracting the build costs, funding costs and developer profit from the GDV.

If you think the GDV of a site is £ 10m, your build costs are £ 4m, and you want to make a profit of £ 2m (20% of GDV), that leaves £ 4m for the land value. However, you still need to deduct the funding costs and every investor underestimates their funding costs.

If you estimate your funding costs at £ 500k, then you might offer £ 3.5m for the site. If you later work out your funding costs are closer to £ 1m, this means you have overpaid for the site.

You can avoid this common pitfall by modelling your site on Brickflow.

The costs involved in a development finance loan include:

- Interest: The interest rate that lenders charge for borrowing money, is rolled up and paid off at the end of the term. Lenders determine their rates based on their cost of funding, the size of your loan, the LTV ratio, the strength of the project and demand for this particular property type in this location, your experience of successfully delivering similar projects, and your equity contribution.

- Arrangement fees: A one-time fee to cover the lender costs of setting up the loan, typically between 1% and 3% of the gross loan amount.

- Exit fees: Typically between 1% and 2%, and payable at any time (so not the same as an early repayment charge on a regular mortgage). Not all lenders on the Brickflow platform charge this, but most do. If you repay the loan early, the exit fee will not change, but you could reduce overall interest costs by repaying early.

- Valuation fees: Lenders will instruct a professional valuation of the site as it is, and the future project to determine its finished market value. The borrower meets this cost.

- Legal fees: You will have to pay legal fees, yours and the lenders, for drawing up the loan agreement and for carrying out the necessary searches and checks on the property.

- Monitoring fees: During the development process, the lender will require regular updates and reports before they advance monies to meet the build costs. This is outsourced to an Independent Monitoring Surveyor (IMS), and there will be fees charged for this monitoring service and for the upfront appraisal of the site.

The rates and fees that you pay will vary with every lender, and so will your deposit requirements, as each lender has different lending limits. Brickflow’s development calculator is the easiest and most accurate way to understand the cost involved.

We also use the metric ‘True Monthly Cost’ (TMC) as a way to fairly compare loan options, which is calculated as below:

(Interest Rate / 12) + (arrangement fee + exit fee) / number of months = TMC

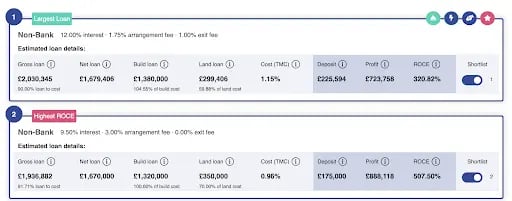

- E.g. (10% / 12) + (2% + 1.5%) / 18 = 1.03% per month

TMC gives an overall representation of what each loan costs. The costs involved are shown on every Brickflow search for development finance.

In this example, you can clearly see the 2nd option, once the interest rate and the arrangement & exit fee is considered, is 0.19% cheaper per month (2.28% per year) - which would mean a saving of nearly £ 23k per £ 1m borrowed.

Development Finance Example: How a Development Finance Loan Works?

Development finance loans are complex and take time to arrange, with every loan tailored to each individual project. As well as the lender, there are additional third parties involved.

Once you have submitted your documentation and development appraisal presentation to the lender, they will confirm credit-backed terms and instruct their Independent Monitoring Surveyor (IMS) and valuer – these fees must be covered upfront, even if the loan does not complete.

The valuer will:

- Confirm site value and suitability for security

- Run a high-level sense check on the build costs

- Confirm the GDV of the end units

The IMS will:

- Closely examine costs and construction methodology

- Assess the developer and their team's ability to deliver the scheme on time and within budget

- Agree a build loan drawdown schedule

Legal work: Once the lender assesses the reports, solicitors will be appointed to deal with the construction and loan documentation -development finance lenders will prefer you to use a solicitor with construction expertise in-house.

Drawdown: When the lender is happy with all valuations and reports and their solicitor is satisfied that all development finance criteria have been met, funds will be sent to the borrower’s solicitor to initiate the loan.

Development finance is allocated in phases; phase 1 is for site acquisition, and phase 2 is to fund the construction. Phase 2 is paid in stages (called tranches) at agreed milestones throughout the construction process. The specifics of the tranches (how much and how often) are agreed from the outset to align with the build schedule, but each tranche can only be drawn when signed off by the lender’s monitoring surveyor.

The loan is drawn in stages because it protects the lender and avoids funds sitting unused in the bank accumulating interest charges for the borrower.

A worked example of a development finance loan:

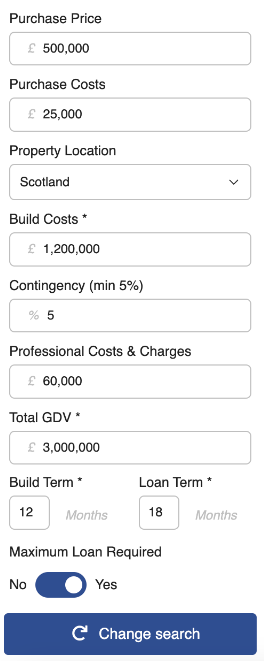

We can look at an example scheme with a £525,000 total purchase costs, £1.2m build costs + £60k contingency and £60k professional costs to see how a development loan works in practice.

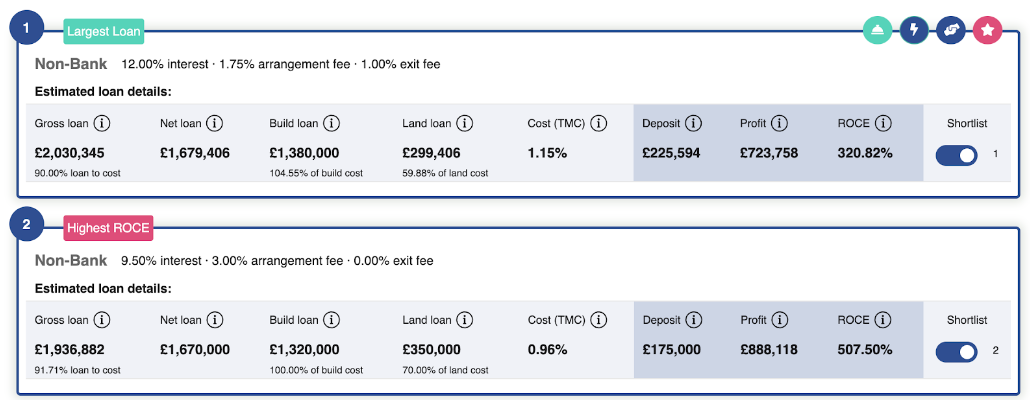

Two potential loan options in this scheme look like this:

A lender’s maximum lending limits, including the land LTV, can affect your deposit requirements by tens or hundreds of thousands of pounds – in these two examples, there is a difference of over £50,000.

Enter your project numbers into Brickflow’s Development Finance calculator today – it takes less than 2 minutes and gives you the clearest, most accurate demonstration of how development finance works and how much it costs.