Borrower Tips

How much money do you need for property development?

How much money do you need for property development, what are the deposit requirements, and is it a worthwhile venture?

Borrower Tips

Borrower Tips

Bridging loans are becoming increasingly useful in property investment and development. In order to secure a bridging loan, you’ll need a deposit.

How much is required for your bridging loan deposit can be anything from tens of thousands to hundreds of thousands of pounds.

Many factors affect your bridging loan deposit contribution, from lender criteria to your experience in property investment. Understanding bridging loan deposits, and how and why they vary so much, is key to securing the right loan for your needs.

This short guide covers how much bridging loan deposit you typically need, strategies for funding it and how you can reduce your equity contribution.

In short, yes, all bridging loans require a deposit contribution, which typically range from 25% - 40% or more of the purchase price. There are situations where you can borrow up to 100% of the purchase price, but this is normally for Below Market Value (BMV) opportunities or where an additional security is offered.

Each bridging loan lender has their own lending caps, which are determined by various factors. The key metric is the loan-to-value ratio (LTV), and it's the lender's criteria that determines the LTV % applied to.your project.

LTV is a calculation used to measure how much money is lent compared to the value of the property. Depending on the type of bridging loan, maximum LTVs (on a gross loan basis) are typically as follows:

In some circumstances, you might be able to secure a 100% bridging loan by offering collateral rather than a cash deposit. Also, your deposit can be significantly reduced if a lender offers you 75% loan-to-market-value on a property you are purchasing for below market-value (from a family member for example).

While the bridging LTV is the core of your deposit requirements, lenders calculate on a gross loan basis, so the net loan (the actual amount made available to you) is the true figure that determines your equity contribution.

Let’s look at an example:

Even though the LTV is 75%, the deposit is not simply £50,000 (25% of £200,000), but over £57,000.

With a different rate, the deposit requirements change again, as per the next example loan.

To find out exactly what bridging loan deposit you need, run your project figures through Brickflow’s instant bridging loan calculator.

Factors influencing the deposit amount

Bridging loan deposits are very nuanced and affected by multiple factors.

The level of risk the loan carries for the lender will shape their lending parameters, and influence both rates and maximum LTVs. Therefore, any of the following can increase or decrease your deposit requirements:

Logically, the higher the purchase price the more deposit required.

If you think of a lender as an investor, you’ll understand that they’re looking to invest their money wisely. In-demand properties, in prime locations and at the right price, give lenders the confidence and flexibility to offer higher LTVs, or better rates and terms.

Your LTV directly impacts your bridging finance deposit, but it can also affect the interest rate lenders offer – generally with LTVs of 60% or lower, (therefore 40% deposit or more) rates are better.

Heavy refurbishment projects inherently carry more possibility of going wrong, over budget and over time. Therefore, lenders perceive higher risk and accordingly charge more.

As well as considering your creditworthiness, assets, liabilities, income and current financial position, lenders look at your previous property experience.

If your bridging finance is to fund a project, lenders want to see similar successful completions. First-time developers or borrowers with poor credit history may still be able to secure a loan, but it will limit the choice of lenders and make it harder to access the best rates and higher loan-to-value ratios.

Naturally, a lender is primarily concerned with how you’ll repay the loan.

A solid exit strategy, for example, an agreed completion date for a property sale or a mortgage in principle for refinancing, de-risks the loan for the lender. In this case, you would have a closed bridging loan. Open bridging loans tend not to have a fixed date for redemption, just a maximum loan term, and the loan could be secured with multiple viable exits. Open-ended loans tend to cost more than closed.

Bridging loans are short-term, so it's key that you can achieve your exit within the agreed timeframe.

If you send the same project to 5 different bridging lenders, you’ll get 5 different loan offers: different rates, different LTV, different T&Cs.

The differences in costs, at a minimum, are thousands of pounds, but often tens or hundreds of thousands pounds, highlighting the importance of performing a comprehensive market search.

Lending parameters depend on things like how a lender is funded, whether or not they are pegged to the base rate, their current loan books and market conditions.

Other than using personal savings and capital, there are options for funding your bridging loan deposit. Exploring alternative options can provide flexibility and better returns on your investment.

Some options include:

For more about structuring your debt and preserving your cash, read The Smart Guide to Bridging Loans.

Brickflow has partnered with Deallocker, a specialist finance platform for second-charge and equity requirements. You can access Deallocker directly from Brickflow once you've secured your most competitive senior loan terms - start your search now, it takes under 30 seconds.

Costs and Fees

If alternative second-charge or equity financing isn’t available to you, there are still plenty of things that can help reduce your bridging finance deposit requirements.

This should be first and foremost. It’s highly unlikely that walking into your high street bank and taking the first loan you’re offered will achieve the best loan with the highest LTV and good rates.

Use Brickflow’s instant bridging loan comparison tool to see loans from across the breadth of the market that are available for your situation.

Specialist bridging loan brokers have behind-the-scenes knowledge on factors like new lender funding lines, negotiable terms, and the best-fit lender for each project type. Many bridging lenders don’t work directly with borrowers, so to secure the best loan with the lowest deposit contribution, leverage the expertise and networks of a broker.

Also, leverage yourself as a trustworthy borrower. If you have a good credit history, successful past projects, and a strong financial position and can demonstrate why you and your project are a worthwhile investment, it can help improve your loan T&Cs.

If you already own the property and want a bridging loan to fund refurbishments, having planning permission in place first can help de-risk your project. Likewise, light refurbishments to your property can add value and increase your borrowing power.

If you’re asset-rich (but cash poor), utilise it. Some lenders will consider a ‘cashless deal’ that enables you to offer assets as your deposit. The additional collateral will have to meet or exceed the deposit requirement.

Read more on 100% Bridging Loans.

Before arranging any bridging loan, consider the risks associated with this type of borrowing. As an asset-secured loan, your assets can be repossessed by the lender in the event the loan goes wrong and you are unable to repay the debt.

If you use additional assets in a cashless bridging deal, every asset is at risk.

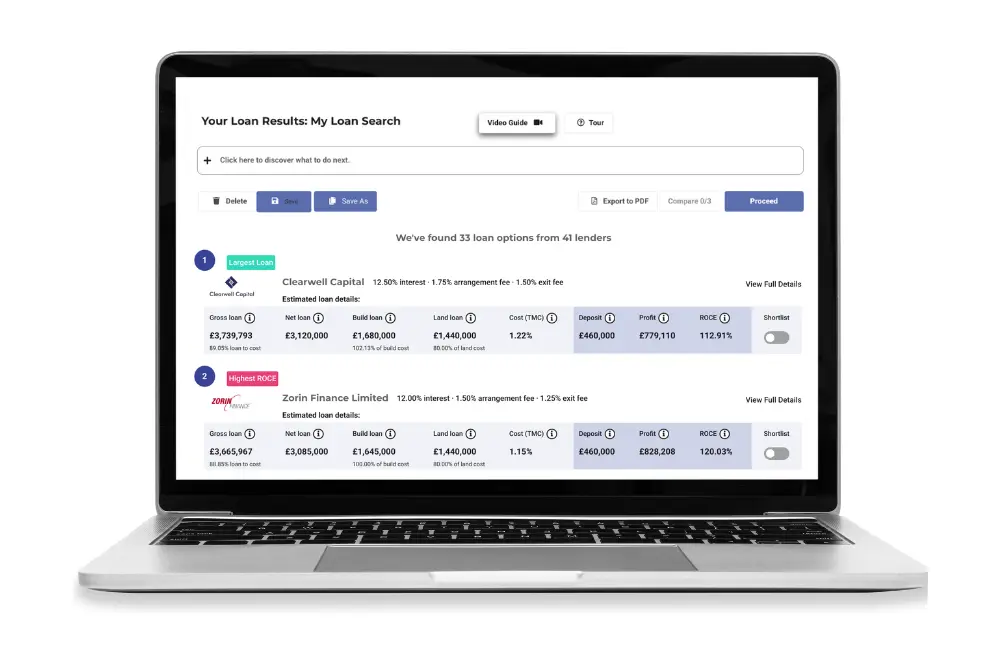

When you compare bridging loans on Brickflow, you can instantly see the bridging loan deposit requirements for every available loan. Consider if you have the financial capacity to contribute that amount of capital.

Depending on your circumstances, securing a bridging loan with a higher LTV and therefore lower deposit is generally favourable. However, consider the overall cost of the loan, and if the higher rates and fees often associated with lower deposit input are outweighed by borrowing more.

Brickflow is the quickest and easiest way to find the best bridging loan on the market. Our bridging loan comparison tool lets you compare loans from the breadth of the market, instantly, with details on rates, fees, LTVs and bridging loan deposit requirements.

It takes seconds to enter your property details and loan requirements so you can find out exactly how much you can borrow, what it will cost and what you will need in deposit.

You can filter and sort your results by the largest loan or smallest deposit, enabling you to potentially access property opportunities with a lower initial investment.

Here’s how:

The amount of equity required for your bridging loan deposit can make or break a potential property deal for you.

Whilst every bridging loan will need some deposit contribution, properly searching the market enables you to find lenders with more flexibility, higher lending caps, higher LTVs and therefore lower deposits.

A few seconds on Brickflow’s bridging comparison tool can help you secure the best bridging loan, reduce your deposit and save thousands. In some cases, your deposit can be reduced by enough to allow you to invest elsewhere simultaneously, which significantly helps you increase your return on investment (ROCE).

Knowing your finance and bridging loan deposit contribution before you commit to any property investment is key and prevents you from pursuing unviable deals.

The answer to this is essentially, ‘How long is a piece of string?’ How much deposit you need depends on several factors:

In some circumstances, lenders might accept additional collateral rather than a cash deposit, but it is not that common.

Speak to a specialist bridging loan broker to explore this further.

Almost all bridging loans are secured with an equity contribution, and the loan itself is secured against the property being purchased or other (sometimes additional) assets.

The risk with every bridging loan is that your exit strategy fails and you are unable to repay the bridging loan. In this case lenders can repossess the assets, meaning you can potentially lose both the asset and your equity. Borrowers will also be asked to provide some form of personal guarantee, which could be called upon if the property sale doesn't cover the loan amount outstanding.

How much money do you need for property development, what are the deposit requirements, and is it a worthwhile venture?

Learn the deposit requirements for commercial mortgages, key factors that affect them, and how to secure the best financing for your business.

A detailed example demonstrating how bridging loans work, with rates, fees and net loan size, and how to secure the best value loan with Brickflow.