Property development often seems like a business venture for people with wads of disposable cash. But realistically, how much money do you need? We’re discussing deposit requirements and if getting into property development is worthwhile.

How much money do you need for property development?

Starting a property development business takes a bit of courage. As with any high-value investment, there’s the risk of losing everything you put in. Having in-depth market knowledge (like accurate sale and rental prices) of the area you’re planning to invest in, plus accurate build and finance costs, will reduce the risks of overspending on the initial purchase or miscalculating profits.

Ultimately, how much money needed to get started depends on many variables.

The vast majority of projects are funded with a development finance loan, where deposit requirements differ with every lender. Small-scale projects, like inhabitable housing requiring extensive renovation, could be funded with a traditional or buy-to-let mortgage, or bridging finance. All of which require a deposit as well as cash for the renovation work. Some lenders offer buy-to-renovate mortgages, where funds for both the property and renovations are loaned.

The first project is likely to be small-scale when starting property development. Comprehensive costings of the work (down to the last bag of tile grout), sticking to budget and shopping around for quotes are crucial to the profitability of the development.

Bigger developments would logically need bigger deposits, and assembling a team with relevant experience, including a project manager, could be needed to secure development finance.

Therefore, how much money is needed for property development comes down to the:

- type of development

- project costs

- type of finance taken

- Individual lender criteria

How much deposit do you need for property development?

So, how much deposit do you need for property development? Well, how long is a piece of string? As with the previous question, deposit requirements depend on the type of finance, project costs and lender. The developer’s personal circumstances (credit history, experience, project shareholdings) are a factor too.

Property development in UK towns, cities and countryside usually involves ground-up construction, repurposing old buildings, or complete renovations. Deposit criteria for each development depend on the type of loan:

- Buy-to-let mortgage – 25% minimum deposit. Most BTL mortgages are interest only, so at the end of the term, the mortgage has to be paid in full.

- Buy-to-renovate mortgage – lenders consider purchase price and estimated value after completion to determine the loan amount. A 25% deposit of the estimated value is required. For example, if purchasing a £200,000 property, spending £70,000 on renovation and achieving an estimated value of £350,000, a lender could provide £262,500 (75% of estimated value) with an £87,500 deposit requirement.

- Bridging loans – mostly limited to 75% Loan to Value (LTV) including arrangement fees and interest (i.e. gross loan) so at least 30% deposit is required.

- Development loan – split into two parts; the first to purchase the site, the second for build costs. Lenders have vastly different parameters, but day 1 leverage is typically limited to 65%, meaning a £200,000 site requires a minimum deposit of £70,000. Up to 100% of build costs will be loaned, so capital isn’t needed for the development stages.

As the projects get larger, deposit sizes will increase proportionally. However, it's common practice for developers to work with investors to help supplement the deposit. Most lenders prefer the developer to have some skin in the game, so borrowing all of your deposit is unlikely to be acceptable, but a developer has just financed a £ 8.1m development project through the Brickflow platform with only £ 200k of their own money.

Any property development loan UK wide will also have set-up fees and interest, plus solicitor, valuation and monitoring surveyor fees are needed on top of how much deposit you need.

Is it worth getting into property development?

With often hefty deposit requirements, is it worth getting into property development? Different experiences will lead to different answers and there are undoubtedly people whose property development ventures turned out to be less than fruitful. It’s common to run into unexpected costs during development, from material shortages delaying construction to uncovering rotten floor joists whilst replacing bathrooms in a period house. A contingency of between 10% and 20%% should be set aside on top of the required equity.

Property development also takes time; if developing a house to live in, it can take years to complete it to the desired finish, meanwhile you have to live on a partial building site. If you’re getting into UK property development as a business, it can take years before obtaining a profit, meaning any capital invested is also tied up for years. Hence, anyone starting out will likely need to have a supplementary income whilst the development is in progress.

Although there are downsides, most people in the industry when asked is property development worth it would say a categorical yes.

At Brickflow, our personal experiences with property development have definitely been worth the investment of both money and time. Brickflow’s founder and CEO, Ian Humphreys has developed multiple ground-up projects since 2015, from single-units to multi-unit schemes around London and the South-East. So, from our point of view, is it worth getting into property development? We’d definitely say yes.

Who can become a property developer?

So, if property investment is in fact worthwhile, the next question is who can become a property developer? The good news is anyone can – there’s no accredited education or formal qualifications required, just extensive market knowledge, creative vision and the courage to plunge hard-earned capital into a project. You will need some experience though, and if you don't have it, then you need to surround yourself with people that do.

The greenest property developers are often first-time buyers, who opt for a run-down property due to budget constraints. As they renew kitchens, replace cracked windows and remove polystyrene-tiled ceilings, the property increases in value. However the first project arises, the satisfaction of transforming a dilapidated building into a home can be addictive, prompting people into becoming a property developer on a full-time basis.

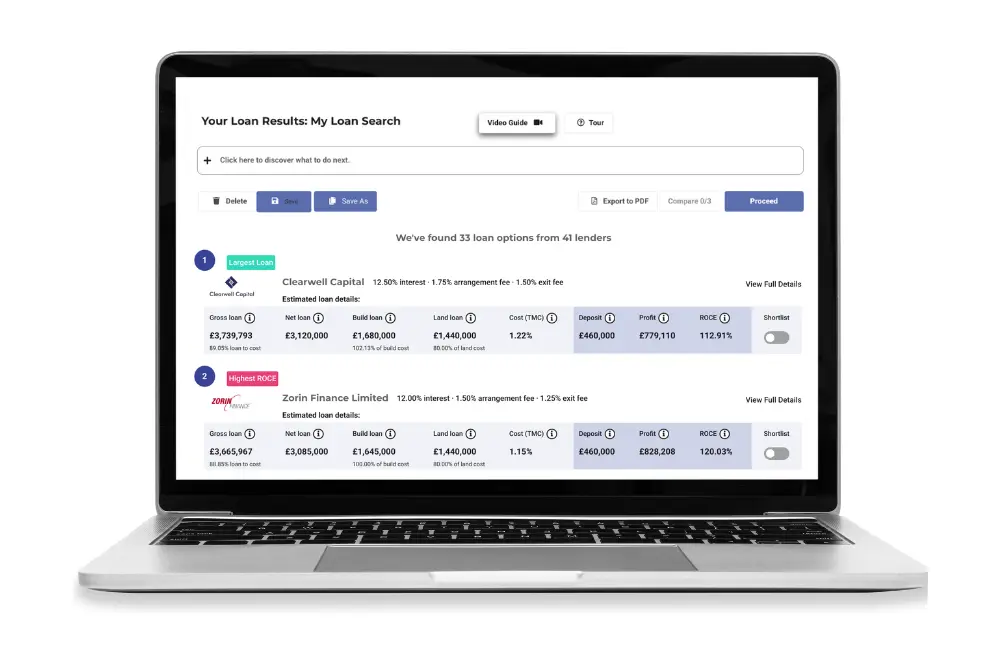

When drilling into the figures of potential properties, understanding property development finance options helps to calculate whether a project is viable or not. Brickflow’s comparison technology is the most comprehensive way to run the financials of a potential site and compare lending options. Being able to see (and scrutinise) all the funding options available means equity requirements can be calculated and borrowing costs can be factored in, meaning you’re less likely to overpay for the site.

As a marketplace for development finance and bridging loans, Brickflow can connect you with the UK’s best brokers, who are experts at finding funding for every project, including for the novice building developer. Our incredible software allows brokers to search and compare loans from over 80 lenders in minutes. And when presenting an application through our Smart Appraisal™ securing a Decisions in Principle takes under and hour (a process that usually takes weeks). If you’re ready to become a property developer and get your project off the ground, register with Brickflow, or tell your broker about us.