In the property industry, bridging loans are now a staple tool for investors and developers, facilitating more market opportunities than otherwise available.

But how exactly do bridging loans work, what costs are involved, and how much can you borrow? In this article, we run through a detailed bridging loan example to demonstrate costs, fees, rates and loan sizes.

The most common use of bridging loans, accounting for 23% of all transactions in Q2 2024, is buying a property before selling to prevent a property chain collapse. So in this article, we'll detail a purchase bridging loan example.

Introduction to bridging loans

Bridging loans are short-term funding secured against the property being purchased or other assets.

They can be arranged quickly and can be used for a vast range of property types, including:

- Residential, commercial and mixed-use

- Derelict buildings and renovation projects

- Land with or without planning

- Property developments at Practical Completion (PC)

- Auction purchases

Lenders assess and approve applications primarily based on the exit strategy (how the loan is repaid), which typically involves selling the property after value-add work, selling your existing home or another property or refinancing onto long-term finance.

The loan is repaid in full at the end of the term. For unregulated bridging, the maximum loan term is typically 24 months, although some lenders on the Brickflow platform offer 30 and 60-month terms in certain circumstances. Regulated bridging is commonly a maximum of 12 months.

Read more about Unregulated vs. Regulated Bridging Loans.

Most UK bridging lenders cap their lending at a maximum of 75% LTV (Loan to Value), with the borrower contributing the rest in deposit. Our dedicated bridging finance page goes into greater detail. For further information about bridging loan costs, head to our blog, How Much Does a Bridging Loan Cost?

What is an example of a bridging loan in action?

Securing a bridging loan follows the same process as other property loans:

- Shop the market: First things first - shop the breadth of the market. There are hundreds of bridging loan lenders, from banks to specialists, all offering different products, fees and rates.

- Application: Prepare your documentation, including ID, proof of address, financials, CV, etc., and create a professional presentation of your project (if applicable) and how the loan will be used. Your bridging loan broker will help you with this.

- Approval: When the lender completes the underwriting process, they make a formal offer. Solicitors are engaged on both sides, and your loan manager will ensure you’re happy with the loan T&Cs.

- Receive funds: After loan approval, funds are typically transferred on the same day.

- Repayment: The loan is repaid in full by either selling the property the loan is secured against, liquidating other assets or refinancing onto a long-term mortgage/development finance/re-bridging.

To see how this works in practice and the actual costs involved, let’s look at a bridging loan example for the most common scenario – purchasing a house while awaiting the sale of an existing one.

The details:

- Purchase price of new property: £350,000

- Property details: Main residence (therefore regulated bridging), Midlands

- Loan term: 4 months

- Exit strategy: Sale of existing home, on the market for £280,000

Here, the lender offers 75% Gross LTV, with total interest charges and the arrangement fees deducted from the gross loan. This leaves £248,211 net loan available to the borrower.

To fully fund the new house purchase in this bridging loan example, you will need to contribute £101,789 in deposit.

The bridging loan lender is repaid using the sale proceeds of the existing house. In this bridging loan example it has enabled the borrower to continue with the purchase of their new home at a cost of just over £14,000.

Breaking down the cost of a bridging loan

We can further break down the costs involved from the above bridging loan example:

Interest charges

Typically, interest is charged daily, so you only pay for your actual loan term.

Some lenders charge monthly, meaning you pay an entire month's interest if you exit partway through the month. It’s important to find this out up-front as avoiding monthly interest charges can save you thousands of pounds.

Interest is either:

- Rolled up: The total interest charge is either deducted from the gross loan or paid on load redemption at the end of the term. It is compounded, making the final interest charges larger than serviced interest.

- Serviced: Paid monthly, like a regular mortgage, with lenders assessing affordability and monthly income upfront. This is much less common.

Arrangement fees

Lenders cover administrative costs for processing an application by charging an arrangement fee. In our bridging loan example, the rate of the arrangement fee is 2%, which is standard. They are typically deducted from the gross loan in the same way as interest charges are.

With Brickflow’s real-time bridging loan calculator, you can find out exactly what lenders’ arrangement fees are.

Exit fees

Exit fees are not common in bridging finance. Almost none of the lenders on the Brickflow platform charge exit fees. Instead, there may be a minimum term, typically between 1 and 6 months, and exiting before this period would incur a charge.

How much can you borrow on a bridging loan?

How much you can borrow depends on several factors, but lenders on Brickflow offer bridging loans from £25,000 - £100 million. There are fewer options at the lower end of the scale, with lenders far more likely to engage in loan applications starting at £150,000.

All bridging loan lenders have different lending parameters and lending caps, but there are key metrics to help determine how much you can borrow:

- The value of the property or securing assets

- The LTV

- The rates you are securing, affecting your net loan

- The property type, location and condition

- The scale of the project, if applicable

- Your exit strategy

LTV is a calculation used to measure the loan size compared to the property value. Depending on the type of bridging loan, maximum LTVs (on a gross loan basis) are typically as follows:

- Purchase/refinance bridging: 75%

- Refurbishment bridging: 75% on the purchase price, up to 100% of refurb costs

- Land/planning bridging: 50% on land with no planning; 75% on land with planning

- Development exit: 75% of the open market GDV (Gross Development Value), less costs of remaining work

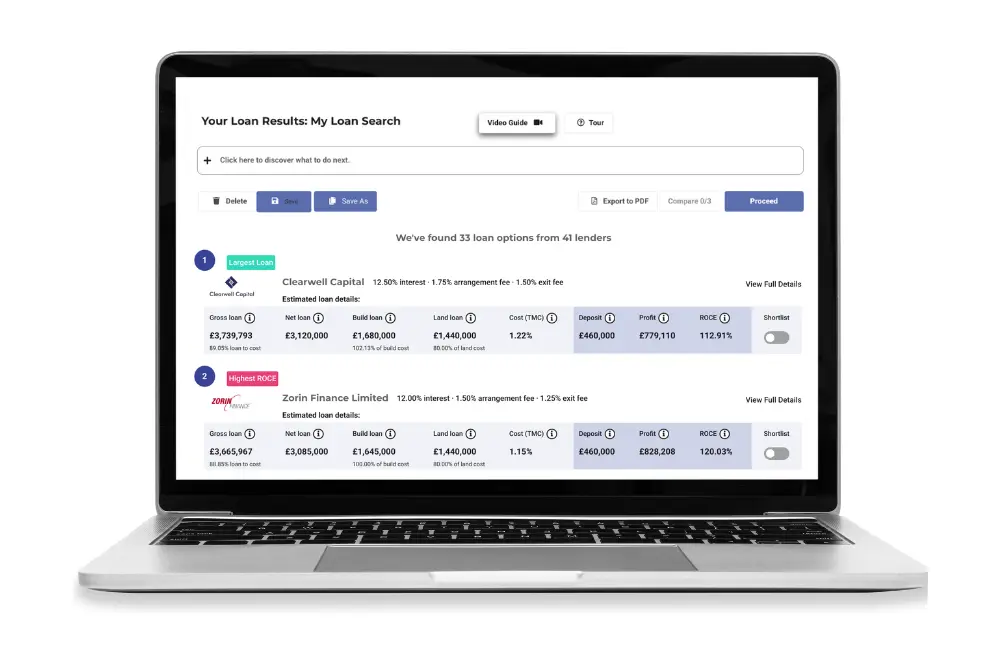

A refurbishment bridging loan example

For refurbishment bridging, how much you can borrow is calculated slightly differently – you can borrow up to 100% of the build costs and up to 75% LTV of the site.

In the below refurbishment bridging loan example, you can see how this works:

Depending on the scale of your project, development finance might be more suitable. It is specifically tailored for ground-up developments, property conversions or heavy refurbishment projects. Brickflow’s lender partners offer development finance loans up to £300 million.

The quickest and most accurate way to find out how much you can borrow is to run your numbers through Brickflow’s real-time bridging loan calculator.

Common use cases for bridging loans

Common scenarios where bridging loans are used include:

- Buying a house before securing proceeds from a sale

- Buying at auction

- Buying unmortgageable properties, such as:

- Uninhabitable houses due to having no working kitchen or bathroom or severe structural problems

- Properties of non-standard construction

- Properties priced below £50k

- Buying land without planning permission, with only outline planning or planning that needs to be enhanced/altered

- Property renovation

- Exiting an existing development loan

- Quick transactions, where being a cash-buyer is advantageous

Bridging loan lenders are equipped to arrange loans quickly, with typical timeframes being between 1 and 6 weeks (in some circumstances, loans can be arranged within days). They are flexible enough to facilitate land purchase without planning or uninhabitable properties, for example. Traditional finance cannot meet many of the requirements for these types of transactions.

How Brickflow can help

With Brickflow, you can search the breadth of the bridging market instantly and compare loans from banks, non-banks and specialist lenders.

Before pursuing any project, use our bridging loan calculator to model your deal and ensure it stacks against real-time borrowing costs.

Here’s how it works:

- SEARCH & COMPARE loans from across the bridging market

- RECEIVE a same-day DIP & shortlist your preferred lenders

- APPLY for a loan with your intermediary or a Brickflow partner

It’s the quickest and most accurate way to see actual bridging loan examples for your project, giving you precise details on borrowing costs, rates and fees.

Find the best bridging loan on Brickflow

By looking at bridging loan examples for various scenarios, you can better understand how they work and the costs involved.

Running your project numbers through Brickflow lets you know your costs from the outset. This means you can instantly see if the deal is viable, if the profit outcome is what you want to achieve, and whether or not the property or site is overpriced.

Take advantage of Brickflow’s award-winning tech to instantly and accurately model your deals, know your finance at the outset and never waste time pursuing unviable projects again. Find out more today.