Bridging loans are fast, flexible finance that can facilitate a huge variety of property transactions – and as with everything, you pay for convenience.

However, whilst bridging loan interest rates tend to be higher than a traditional mortgage, they might not be as expensive as is commonly believed.

In this article, we’re looking at UK bridging loan interest rates, factors influencing your bridging loan rate and how Brickflow’s instant bridging comparison tool can help you secure the best value loan.

What is the interest rate on a bridging loan?

As of Q3 2024, in the UK, bridging loan interest rates were between 0.75% and 1.4% per month (0.67% to 1.4% in Q2 2024), with an average monthly rate of 1.04% (1.05% in Q2 2024).

The average rate is taken from all bridging loan products offered by all lenders on the Brickflow platform. Our lenders span the breadth of the market, from high-street banks to specialist lenders.

As a short-term loan, sometimes arranged for as little as one month, bridging loan rates are almost always calculated monthly, unlike the annual rates quoted on a mortgage.

Bridging loan rates are set by the lender at the outset and are typically fixed. This means the interest rate is the same for the duration of the loan.

Factors influencing bridging loan interest rates

Bridging loans are usually bespoke finance products created to meet your specific situation and property transaction. Therefore, the rate you secure is influenced by a number of factors:

- The total loan size: The amount you wish to borrow

- The Loan to Value (LTV): Bridging loans are often limited to 75% LTV. The higher your LTV, the higher the rates. Better rates typically kick in on loans with 60% LTV or less.

- Property type, location and condition: The level of perceived risk in a loan helps determine rates and loan T&Cs. Therefore, a prime location property with a higher likelihood of resale will typically have lower rates.

- Your planned project: Again, based on associated risk, large-scale and heavy refurbishment projects can have higher rates than a straightforward purchase.

- Your exit strategy: Is your sale completion date set? Do you have an agreement in principle for your refinance? A strong exit strategy can reduce rates.

- You as a borrower: Having bad credit or a lower income doesn’t necessarily prevent you from securing a bridging loan. However, borrowers with strong creditworthiness, high net asset value and a track record of successful property investments can help derisk the loan for lenders and secure better rates.

- The market: The Bank of England’s base rate, the current demand or dip in property transactions and other housing and property trends can affect rates.

Your bridging loan interest rate also depends on which lender you use – every lender will have different rates, lending limits and criteria.

How do bridging loan interest rates work?

Bridging loan interest rates work in much the same way as interest rates on other property debts – the rate is set by the lender and added to the debt. To repay the loan, both the capital and the interest charges have to be paid.

How is interest repaid on a bridge loan?

A key difference is how interest is repaid on a bridging loan. While long-term mortgage interest is repaid in small instalments, bridging loan interest is typically paid in one lump sum.

This is known as rolled-up interest, meaning the interest charges for the duration of the term are calculated and typically deducted from the gross loan. Fees and charges are also deducted from the gross loan, with the remaining amount made available to the borrower (the net loan).

Some bridging loan lenders offer serviced interest, meaning it is paid monthly, but it is much less common.

How long do you pay bridging loan interest for?

With bridging loan interest, you only pay for the duration of your loan, which is typically calculated per day. This means if you exit the loan part way through a month, you will only pay for the days that you had the loan.

Most bridging loan lenders don’t charge early repayment or exit fees. So if your originally agreed term is ten months, but you repay the loan after six months, you will only pay six months' interest charges.

Comparing bridging loan rates to other loan types

Average bridging loan interest rates tend to be higher when compared to mortgages and personal loans due to their short-term nature and faster approval process.

Currently, UK mortgage interest rates average between 4% and 6% annually, significantly lower than bridging loan rates, which range from 0.75% to 1.4% per month. Though bridging rates are always shown monthly, for the sake of comparison, this would equal approximately 9%-17% annually.

Personal loans in the UK generally have annual rates ranging from 6% to 12%, also below the cost of bridging loans. The higher rates of bridging loans reflect the convenience of short-term borrowing and the speed at which funds can be accessed, often within days.

|

Loan Type

|

Interest Rate (Annual)

|

Interest Rate (Monthly)

|

|

Bridging Loan

|

9% – 17%

|

0.75% – 1.4%

|

|

Mortgage

|

4% – 6%

|

0.34% – 0.5%

|

|

Personal Loan

|

6% – 12%

|

0.5% – 1%

|

Bridging loans are often necessary when time is critical, which usually outweighs the higher costs involved.

Additional costs of bridging loans

When taking out a bridging loan, there are additional fees beyond interest rates to be aware of. These costs can vary on a case-by-case basis but will typically include the following:

Arrangement Fees

Lenders cover their administrative costs of setting up the loan by charging arrangement fees, which typically range from 1% to 2% of the loan amount. They are generally added to the loan and paid at the end of the term or deducted from the gross loan.

Exit Fees

Though uncommon in bridging finance, some lenders charge an exit fee when the loan is repaid, especially if repaid early. There will usually be a minimum term, though, for exiting without incurring fees, such as 1, 3 or 6 months.

Almost none of the bridging loan lenders on Brickflow charge exit fees.

Valuation Fees

Most lenders require a property valuation before granting a bridging loan. This fee is around 0.1% of the property’s value, depending on factors such as property type and condition.

Valuation fees are paid upfront and are non-refundable, even if the loan doesn’t go through.

Legal Fees

You need to cover both your legal fees and the lender’s, with costs starting around £2,500 + VAT. Legal fees are paid upfront and are unavoidable as they are required to process the loan and secure the lender’s rights.

Broker Fees

Brokers usually charge fees for arranging a bridging loan, but they are typically paid by the lender as part of the arrangement fee. Some brokers may add an additional fee - it's important to clarify this early on.

Fee Comparison Table

|

Fee Type

|

Bridging Loans

|

Traditional Mortgages

|

|

Arrangement Fee

|

1% - 2%

|

Often waived

|

|

Exit Fee

|

Rare (if exiting early)

|

Early repayment penalties

|

|

Valuation Fee

|

Approx. 0.1% of property

|

£300 - £1,500

|

|

Legal Fees

|

£2,500+ + VAT

|

£0 - £1,500

|

|

Broker Fees

|

Often covered by the lender

|

Sometimes applicable

|

Understanding these costs helps you better budget the total amount needed to secure a bridging loan and help to determine how much deposit you’ll need.

How much can you borrow on a bridging loan?

Lenders on the Brickflow platform offer bridging loans between £25,000 and £100 million.

How much you can borrow depends on:

- The lender and the rates and terms of the loan

- The LTV

- The property value, type and condition

- You as a borrower, including your creditworthiness and property investment experience

- Your exit strategy

- Your deposit

Lenders typically have the following maximum loan to value ratios, depending on the type of property you’re funding with the bridging loan:

In the below example, you can see two potential bridging loans from two different lenders when offering on a £300,000 purchase property.

Whilst option 1 offers more than 75% LTV, therefore reducing the deposit requirement by nearly £2000, this has to be weighed up against the total lender costs.

How to find the best bridging loan interest rates

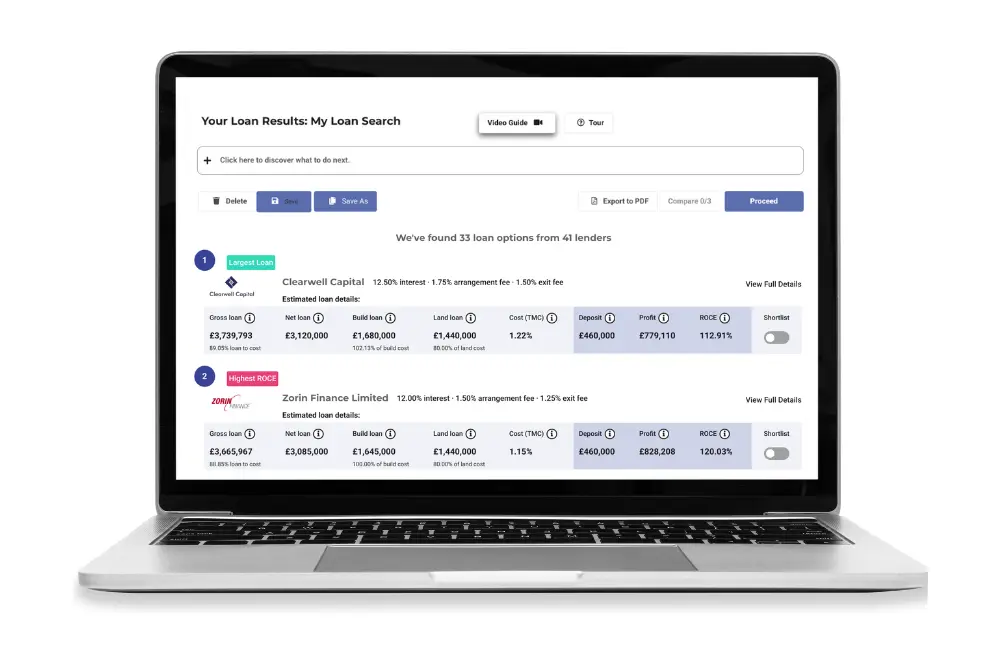

Like with residential mortgages or car/home/travel insurance, the only way to find the best bridging loan interest rates is to shop the market and obtain quotes for your specific requirements (rather than generic bridging rates).

Seeing the actual borrowing costs from multiple lenders, tailored to your property investment, is the only way you can be sure you’ve found the best value loan.

Brickflow’s instant bridging loan comparison enables you to do exactly that.

How Brickflow can help

Our award-winning tech has made the process of finding competitive bridging loan interest rates and better-value loans ultra-efficient.

Here’s how it works:

- ENTER your project criteria and model deals|

- It takes seconds to search for loans from banks, challenger banks, non-banks and specialist bridging lenders

- Find out exactly how much you can borrow and how much it will cost

- COMPARE loans from 50+ bridging lenders

- Compare LTVs, interest rates, fees & deposit requirements

- Filter & sort your results, and shortlist your preferred loans

- APPLY directly from the platform with your intermediary or a Brickflow partner

- Get multiple same-day DIPs back (our record is 7 minutes!)

- With your intermediary, apply using Brickflow’s digital Smart Appraisal(™), the only tool that directly connects with lenders

Lenders love a Brickflow application because it covers everything they need to know to make quick credit decisions – but if one lender says no, you can apply to another with one click.

To understand all the costs involved in your bridging loan and to compare bridging loan interest rates and fees, use Brickflow’s instant bridging calculator today.

Ready to secure the best bridging loan rate?

Finding the right bridging loan doesn’t have to be complicated.

In this article, we’ve covered everything from what bridging loan interest rates are and how they work to the factors influencing your rate and how to compare these loans effectively.

By understanding the total cost of borrowing, including interest rates and additional fees, you can make an informed decision that best suits your property project.

Brickflow’s bridging comparison tool makes it easy to explore loan options from over 50 bridging lenders instantly, helping you find the most competitive bridging loan rates. Our same-day decisions-in-principle and seamless loan application process can help you get your project going sooner and take the stress out of securing finance.

Ready to get started? Use Brickflow’s instant bridging loan comparison today and apply for a loan with your intermediary or a Brickflow broker partner.

FAQs

What is the exit fee for a bridge loan?

Exit fees are uncommon in bridging finance, but some lenders might charge an exit fee when the loan is repaid, especially if repaid early. There will usually be a minimum term, though, when exiting without incurring fees, such as 1, 3 or 6 months.

Almost none of the bridging loan lenders on Brickflow charge exit fees.