Yes, 100% LTV bridging loans do exist — so when and how can you obtain one?

Bridging loans have undoubtedly become the ‘new black’ in property finance, as more property investors understand how and when to use them to unlock opportunities.

One such example is when you’ve found a great project but are out of capital — with a 100% bridging loan, you can still make that project a reality.

However, 100% bridging loans are only available under certain circumstances, with only a limited number of lenders willing to offer them.

In this article, we explain when and how you could secure 100% funding and how Brickflow’s instant bridging comparison tool can help you find the right lender.

What is a 100% bridging loan?

A 100% bridging loan is a short-term funding solution where the lender offers 100% LTV (loan to value), i.e. you borrow the total amount of the property purchase price.

There are two circumstances when it is possible to secure a 100% bridging loan: by using additional securing assets or buying a below-market-value property.

Additional security

To secure a 100% bridging loan with a lender, you will need to offer additional assets as security — typically one or more properties. You can use properties with existing mortgages, but there needs to be enough equity available after the remaining mortgage debt.

In essence, a 100% bridging loan is a cashless deal that uses assets for the deposit rather than capital.

Buying below market value

In some circumstances, a lender will offer the full market value of the property even though the agreed sale price is lower, therefore any loan amount above the selling price acts as a deposit.

Typical examples of this include buying from friends and family or buying from a distressed seller.

Benefits and risks

Securing property without a capital contribution opens up a greater number of opportunities and enables you to purchase a property prior to receiving sales proceeds, either from your home or a development project.

However, this type of lending is higher risk and more work for lenders, involving multiple valuations. As a result, it typically comes with higher rates and fees. Crucially, all of the assets offered as security are at risk of repossession if things go wrong and you’re unable to repay the loan.

Eligibility criteria for 100% bridging loans

To qualify for any bridging loan, you will have to meet certain eligibility requirements.

Standard criteria include:

- Aged 18 or over, with some lenders imposing an upper age limit.

- A UK resident or UK national living abroad. There are options for non-UK residents, but they are limited.

- Employed, self-employed or retired.

Read more at 'Who Can Get a Bridging Loan? Eligibility & Criteria'.

Following this, eligibility then comes down to your exit strategy and how viable it is. If you plan to refurbish the property and sell it, lenders will need details on your works schedule, the team you're using and your previous experience.

If your exit strategy involves repaying the loan with sales proceeds from another property, lenders will consider its value, location, condition and desirability.

For 100% bridging loans, lenders conduct more in-depth due diligence, both on you as a borrower and your exit strategy. If using additional securing assets, all are valued individually.

Key information lenders need to consider a 100% bridging loan application include:

- Your income

- Your credit history and credit reports

- Your financial situation and statements

- Tax returns

- Documentation for each asset offered as security

Whilst low income and poor credit history are not normally a barrier to securing a bridging loan if you can prove you’re able to pay in a distress situation, it can be problematic when it comes to 100% bridging loans.

Your best chance to secure a 100% bridging loan is by speaking to a specialist debt advisor. At Brickflow we work with some of the UK’s best bridging loan brokers and are happy to connect you.

Use cases for 100% bridging loans

100% bridging loans are typically used when a borrower has no working capital but wants to purchase another property. Rather than a cash contribution, they can use equity from other properties.

For example, a borrower may have enough funds to carry out renovation work, but not enough for both the work and a deposit. Securing 100% funding enables them to progress the project without having to wait for liquidity from elsewhere.

Let’s look at how this works when buying below market value:

- Purchase price of property = £400k (agreed pre-work)

- Improvement works = £60k

- Post development value = £540k

- Raise finance based on 75% LTGDV = £405k loan

In this case, the lender could offer just over a 100% LTV bridging loan, meaning the borrower only needs £60k to fund the works, rather than a £100k deposit (75% LTV of £400k) plus £60k for works.

In the same scenario, using additional collateral to secure 100% of the purchase price, the borrower still only needs £60k.

Tips for securing a 100% bridging loan

As with any bridging loan, lenders look for a solid exit strategy.

Lenders love to see definitive exit plans, but some bridging loan lenders are comfortable with multiple viable exits.

Our top tips to improve your chance of securing a 100% bridging loan:

- A strong exit: If you can, get an agreement in principle for your next finance, such as a BTL mortgage. If you plan to sell the property, demonstrate market demand for your property, and show your marketing strategy if relevant.

- Inspire lender confidence in you: Present your portfolio of past successful projects, in particular any similar projects. Show your team’s skill and ability to complete the project on time and on budget.

- Create a perfect projection presentation: Lenders willing to offer 100% bridging loans want to see a comprehensive proposal, with detailed costings and timelines, and relevant market research. They have zero interest in half-baked ideas with no proper due diligence.

- Get your documents in order: Lenders often request additional information during the application process. Have your documents ready, and respond promptly - delays in producing required documentation can lead to frustration on all sides.

When you apply for a bridging loan through Brickflow, our Smart Appraisal(™) covers everything lenders need to know. Complete your application with your intermediary - you can save your progress and log back in at any point. You can also upload and store documents, including your CV, which will automatically update with each project you complete.

Read more about the application process in The Smart Guide to Bridging Loans.

Alternatives if a 100% loan is not available

If you want to proceed with a project but lack capital and a 100% bridging loan isn’t available, there are some alternative options:

- Second-charge loans: In some circumstances, you can take a smaller, secondary loan, referred to as ‘mezzanine debt’ or ‘stretched senior’.

- Bring in an investor: Leverage your networks and bring in the right partners for your project in return for a profit share.

- Development finance: If your planned project involves heavy or large-scale refurbishments, development finance might be a more appropriate option. It’s specifically orientated to property development and you could borrow up to 100% of the build costs.

How Brickflow can help

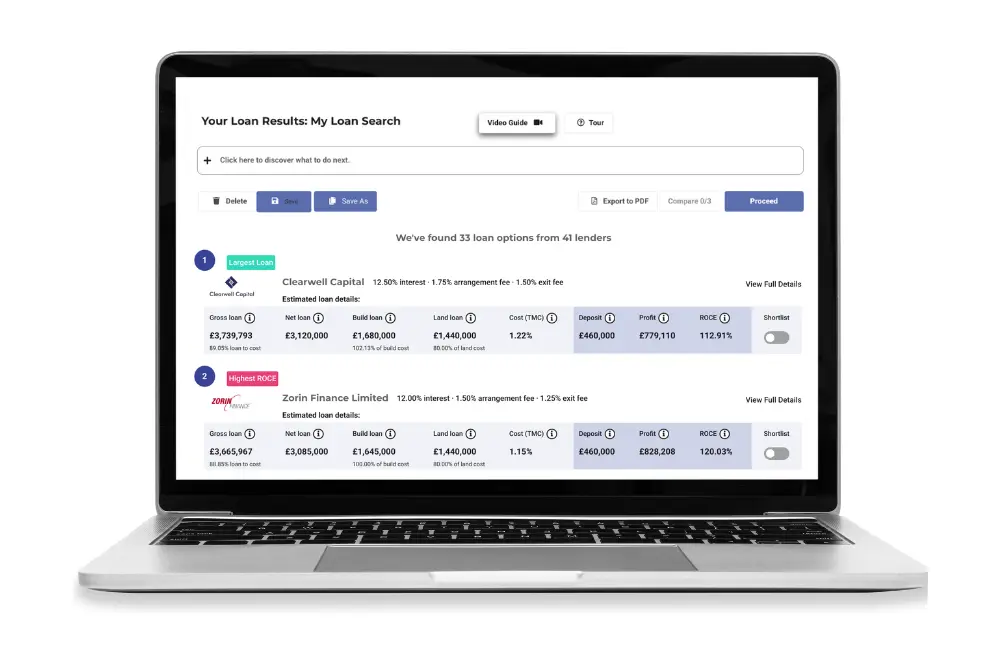

At Brickflow, you can instantly compare bridging loans from the breadth of the market to see exactly what you can borrow and how much it will cost.

Financing makes or breaks deals. Our instant loan search offers you tech-powered due diligence in under 60 seconds, so you’ll never waste time pursuing unviable projects.

Here’s how Brickflow works:

- ENTER your project criteria and model your deals

- COMPARE live loans from 100+ lenders in seconds

- APPLY with your intermediary

If you want to secure a 100% bridging loan, tell your broker about Brickflow and apply directly from the platform. You’ll receive multiple DIPs (Decision in Principle) within minutes of requesting terms, and you can apply to multiple lenders with just 1 digital application. If one says no, simply apply to another with one click.

Secure your 100% bridging loan today

The circumstances in which you can secure a 100% bridging loan are quite specific, and only a limited number of lenders offer this type of funding.

Your options for purchasing a property without a cash deposit contribution are either to use additional collateral or purchase below market value.

Before any property investment, make sure your deal stacks against actual borrowing options. When you compare bridging loans on Brickflow, you see all available loans for your project, showing like-for-like details on:

- Maximum LTV

- Interest rates

- Fees

- Gross and net loans

- True monthly costs

Search for your next bridging loan on Brickflow.

If you want to know more about 100% bridging loans, run your numbers through Brickflow’s instant bridging loan comparison tool and speak to our preferred intermediary partner. Alternatively, connect with one of Brickflow’s specialist bridging loan brokers.

FAQs

What is the maximum amount of a bridging loan?

In certain circumstances, you can secure a 100% bridging loan. They require additional assets as security and are not available to every borrower. The number of lenders offering this type of finance is also limited.

Can you get a bridging loan with no deposit?

Yes, it is possible to secure a bridging loan without a cash deposit in some circumstances. Instead, a lender might accept additional security, essentially offering a cashless deal.

Is it hard to get a bridging loan?

If you have a viable exit strategy, whether that is the sale or refinance of another property, or the sale or refinance of the property you are buying, getting a bridging loan can be straightforward.

If you intend to carry out development work on the property, you need to provide a detailed proposal of the work involved, as well as your ability (and your team’s, if relevant) to deliver the proposed plan.