The UK housing market can be tricky, navigating property chains or trying to secure your dream home before selling your existing home. Bridging finance has become a key solution, offering temporary liquidity that can prevent you from missing out on market opportunities .

In this guide, we look at using a bridging loan to buy a house, how it works, the costs involved and how Brickflow’s bridging loan calculator can help you make sure your deal stacks and secure the best bridging finance on the market.

How do bridging loans work when buying a house?

Using a bridging loan to buy a house works in the same way as any other bridging finance - it's short-term, usually up to 24 months, secured against the property being purchased (or other/additional assets) and fast to arrange.

They are agreed on the basis that the borrower will soon have liquidity, either from the proceeds of an upcoming sale or through refinancing onto a longer term mortgage. Your specific exit strategy will be agreed with the lender at the outset and they will monitor whether or not it is proceeding to plan throughout the loan term.

A well-defined exit strategy, such as an agreed completion date for a sale, will make it easier to secure a bridging loan and most likely with better terms and rates.

When using a bridging loan to buy a house, it’s key to understand the difference between regulated and unregulated bridging finance:

- Unregulated bridging loans: Can be used for both commercial, residential and mixed-use investment properties, including things such as buy-to-let flats or houses, HMOs or a refurbishment project.

- Regulated bridging loans: Used when the property being purchased (or used as security) will be the borrower’s, or an immediate family member’s, home. Regulated bridging finance offers borrowers protection if they’re sold an unsuitable product or given misleading advice from lenders or brokers, with possible compensation if eligible. It is regulated by the Financial Conduct Authority (FCA) and carries the same rules as a residential mortgage. As such, they are not as fast to arrange as unregulated loans.

Scenarios where bridging loans are used when buying a house?

Bridging finance has become relatively mainstream as a solution for buying a house or property. They are fast and flexible enough to suit a diverse range of borrowers and can therefore provide a solution in many property scenarios.

Some example scenarios when bridging loans can be used:

Buying a new property before selling an existing one:

Since they first came to market in the 1960’s bridging loans have rescued many home buyers who haven’t secured a sale for their own home, or a sale has fallen through, but want to continue the purchase of their next home.

Breaking a property chain:

In parts of the UK, multiple home purchases and sales can be linked together, meaning a buyer pulling out somewhere along the chain can affect everyone involved. Bridging finance means you can act as a cash buyer and break that chain and the associated risks. As above, it allows you to buy before selling.

Buying at auction:

For homebuyers with a limited budget or out-priced from their local area, or investors looking to capitalise on below-market-value properties, bargains can often be found at auctions. But the 28-day completion timescales rule out traditional finance.

Investors buying at auction can use unregulated bridging finance, whilst homebuyers would have to take out a regulated bridging loan. Find out more about regulated vs unregulated bridging here.

Renovation and sale:

Some properties, and often those found at auction, are not eligible for traditional finance because they are considered uninhabitable. This typically includes properties that are structurally unsound, or without working kitchen and bathroom facilities. A refurbishment bridging loan can finance part of the purchase and up to 100% of the work costs, before either selling, or refinancing.

Alternatively, if the refurbished property will be the borrower’s home, the bridging loan can be repaid by selling their existing home.

Acting fast:

- Seizing opportunities: Sometimes opportunities unexpectedly present themselves and securing the funding quickly can help to trump the competition.

- Urgent Relocation: Individuals who need to relocate quickly for a new job might use a bridging loan to buy a house in the new location before selling their current home.

Read our in-depth guide for more information on fast bridging loans, timescales for approval and tips for securing a loan quickly.

Mortgage delays:

If there is a delay in securing a mortgage for a new property, a bridging loan can cover the purchase cost until the mortgage is approved and funds are disbursed.

What types of property can you buy with a bridging loan?

Bridging loans can facilitate a huge range of property purchases. Here are just a few examples of the types of property you can buy with a bridging loan, but the list is by no means exhaustive:

- Commercial properties, such as education facilities, medical buildings, care and retirement homes, retail and leisure, hotels, student accommodation, etc.

- Residential properties, including flats, houses and new builds

- Mixed-use residential and commercial properties

- Mixed-use commercial

- Buy to let investments

- House in Multiple Occupancy (HMO)

- Multi unit freehold block (MUFB)

- Renovation projects

- Properties at auction

- Properties where you will convert its primary use

- Land, with or without planning permission

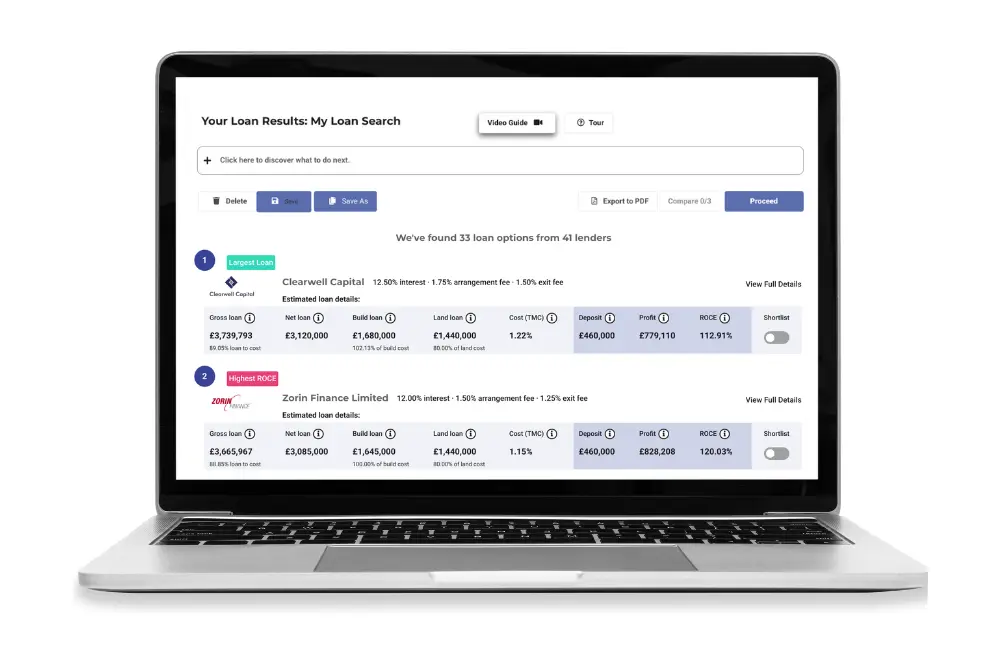

If you want to know if you can fund your next property purchase with a bridging loan, enter the details into Brickflow’s live bridging loan calculator. You’ll instantly see how many lenders will offer a loan, how much you can borrow and what it will cost you. You can then filter your results to match your specific circumstances.

It takes seconds, and offers the most comprehensive financial due diligence for your property investment, enabling you to instantly see whether your deal stacks or not.

Find out more about bridging loan eligibility criteria and what you need to apply.

Process of securing a bridging loan when buying a house

The process for securing a bridging loan for a house purchase is similar to any bridging finance:

- Search the market: To find the best deal for your circumstances, you have to shop around. At Brickflow, you can search over 50 bridging lenders, instantly.

- Submit your project appraisal: Your application should comprehensively cover your property details, plans for the property and demonstrate a viable exit strategy.

- Terms offered: Lenders will return a Decision in Principle (DIP). At Brickflow, you can receive multiple DIPs within minutes of applying, allowing you to choose your preferred loan and progress to approval in the same day.

- Approval: The lender will conduct due diligence on you as a borrower, the property being purchased and any additional securing assets. For unregulated bridging, approval typically takes around two weeks depending on the lender’s valuation report and the legal searches. Where lenders work with an AVM (automated valuation model) and accept title insurance, no searches are required, so completion can be in just a few days. Regulated bridging requires more checks and paperwork, and similarly to a mortgage, can take up to 12 weeks to complete.

- Loan drawdown: Once the loan completes, funds are immediately available for drawdown.

At Brickflow, we’ve streamlined the process for securing bridging finance into a single digital journey, where you can instantly search & compare bridging loans, receive multiple same-day DIPs, and apply with your intermediary, directly from the platform.

Costs associated with a bridging loan

The costs associated with a bridging loan will typically be higher than traditional long-term finance. This is because they are perceived to carry more risk to lenders, and they are fast and flexible - as with everything, you pay for convenience.

Additionally, as a type of specialist property finance, the loans are often tailored to your needs rather than being an ‘off-the-shelf’ product like most mortgages are.

Knowing the cost of your bridging loan before you commit to any house purchase is essential - run your numbers through Brickflow’s live bridging calculator to avoid wasting time on deals that don’t stack.

The typical costs are:

Interest charges:

Most lenders offer rolled-up interest (paid at the end of the loan), so there are no monthly payments involved, however the interest paid is therefore compounded.

Interest is calculated daily, so you only pay interest on the duration of your loan, even if you exit the loan early or midway through a month. Your final redemption payment (to pay off the loan) will include the original amount of capital borrowed plus accrued interest.

The rate of interest on your loan will depend on:

- The property: Its value, location, condition and desirability.

- Your planned project: The more involved the project, the more risk for lenders.

- The LTV (Loan to Value): A lower LTV can help secure lower interest rates, but it would typically require a 40% deposit or more for better rates to kick in.

- Your exit strategy: Lenders love solid exit strategies, such as an agreed date for a sale completion. Regulated bridging requires a defined exit whilst unregulated loans can have multiple potential exits can strengthen an application and in some cases, lower rates.

- You as a borrower: Including your credit file, asset net worth and experience in investing in similar properties.

Other fees:

- Valuation or survey fees: Lenders will arrange for a surveyor to assess the property. Survey costs depend on the property value, type, location and complexity. Lenders should provide quotes from more than one firm and let you choose your preferred option. Your bridging loan intermediary should be able to help you with this.

- Legal fees: The lender’s legal fees, as well as your own.

- Broker fees: Normally paid by the lender.

- Arrangement fees: Up to 2% of the gross loan.

- Exit fees: Not that common for bridging finance. Almost none of the lenders on the Brickflow platform charge exit fees, but they instead might stipulate a minimum loan term – between 1 & 6 months normally.

Using Brickflow to find the best bridging loan for a house purchase

If you commit to a property investment before you know what you can borrow and what it will cost, you run the risk of taking on a losing project. By modelling your deals on Brickflow, you can help avoid that scenario - and it only takes a few seconds.

Just like with a residential mortgage, you need to shop the market to find the best bridging loan for a house purchase. Use Brickflow to compare bridging loans from across the market and when you’ve found your deal, apply online with your intermediary.

It's really this easy:

1. ENTER your project criteria and model deals

- It takes seconds to enter your property details & search loans from banks, non-banks and specialist bridging lenders

- Financing makes or breaks deals - find out exactly how much you can borrow and how much it will cost before you pursue a project

2. COMPARE loans from 50+ bridging lenders

- Compare max LTVs, rates, fees, deposit requirements & more

- Filter and sort your results, and shortlist your preferred loans

- Save your search and log back in later

3. APPLY directly with your intermediary (or a Brickflow broker partner)

- Secure a same-day Decision In Principle (our record is 7 minutes)

- Use our Smart Appraisal(™) tool, the only application that connects directly with lenders, and covers everything they need to know to make quick, reliable credit decisions

- Complete one appraisal and apply to multiple lenders, so there’s zero repetitive paperwork

Smart developers and investors don’t wing it - make Brickflow a funding habit, and carry out your tech-powered financial due diligence in under 60 seconds.

FAQs

Does your current property need to be valued in order to get a bridging loan?

Yes, if you intend to repay the bridging loan with the sale of your current property the bridging loan lender will want to know the market value of the property, as well as how much mortgage debt is outstanding on the property.

If you’re using your current property as the securing asset for the bridging loan, the lender will also carry out a valuation.

Is it possible to get a 100% bridging loan to buy a property?

In some circumstances it is possible. If for example, you buy a property that is below market value, but the lender is willing to lend up to 75% of market value, it could equate to 100% of the purchase price.

Alternatively, some lenders might be willing to accept additional security rather than equity input, in a kind of ‘cashless deal’. Lenders will only consider a cashless arrangement on a case by case basis. A specialist bridging loan broker can help you.

You are at risk of losing all assets used to secure the loan should you default.

Does a bridging loan cover any refurbishment work that I want to do to the property that I am purchasing?

Yes, there are many lenders that will cover up to 100% of the proposed work.

Search for bridging loans on Brickflow to find out exactly what you can borrow for your project.

Can bridging loans be used to pay stamp duty?

Technically, yes a bridging loan could be used to cover stamp duty, when arranged as part of the overall bridging loan to buy a house.

Is it possible to turn a bridging loan into a mortgage?

Yes, it is possible to exit a bridging loan by refinancing the property with either a residential mortgage or a commercial mortgage.

If refinancing is your exit strategy for your bridging loan, lenders will need to know that you can secure a traditional mortgage for the appropriate amount - a mortgage decision in principle is favourable.

Conversely, borrowers with bad credit can struggle to secure a residential mortgage, which will be problematic for the bridging loan lender.

What’s more expensive, a bridging loan or a mortgage?

A bridging loan for a house purchase will typically be more expensive than traditional long-term finance. This is not only because they are fast and flexible finance, but because they will typically carry more risk to lenders than a long-term amortising loan.

Additionally, whilst bridging loans are now mainstream, they are still a type of specialist property finance, and often tailored to your needs rather than being an ‘off-the-shelf’ product that most mortgages are.

Read more in Bridging Loan vs. Mortgage.

How long does it take to buy a house with a bridging loan?

For unregulated bridging, funding typically takes around two weeks to be released from application, depending on the lender’s valuation report and the legal searches. If a lender works with an AVM (automated valuation model) and accepts title insurance, therefore meaning no searches are required, completion can be in just a few days.

Regulated bridging, which is subject to the same regulations as a homeowner mortgage, can take up to 12 weeks to complete.