Whatever your property development plans, bridging finance is a fast, flexible way to fund your project. But alongside the opportunities comes risks, so we’re looking at both sides of bridging finance, as well as how to get the best deal.

Should I apply for a bridging loan?

Bridging loans can undoubtedly be a useful solution for quickly accessing capital, so you might be thinking, should I apply for a bridging loan? Whether or not a bridging loan is the right financial product for you depends on your specific circumstances and financial goals.

Before beginning the bridging loan application process, take time to consider the following:

- How much funding do you need and for how long?

- Have you exhausted all other funding methods? Bridging finance is typically more expensive to borrow than long-term finance, so check if your project and circumstances meet eligibility criteria for other, cheaper borrowing.

- What is your exit strategy?

- Refinancing onto a long-term mortgage

- Selling the subject property

- Selling another property

- A cash injection from elsewhere

- Do you have a fixed date that you will be able to repay the loan?

- Closed-bridge loans are used when the borrower knows the exact date they will be able to repay, like when they have an agreed completion date for a property or business sale

- Open-bridge loans are used when there is a proposed exit strategy but no fixed date, for example when bridging is used to buy and renovate a property to sell

- Are you confident in your exit strategy? Bridging loans require personal or corporate guarantees, so if you are unable to repay the loan, and the lender makes a loss if they sell the property for you, they can make a claim against your other assets.

For any bridging loan application, you will need to provide detailed information about your financial situation, including your income, expenses, and existing debts. You will also need to provide information about the property or asset that you are using as collateral.

Opportunities Provided by Bridging Finance

Across the property market, the opportunities provided by bridging finance are sizeable, and for most developers, bridging loans are a key financing tool. So let’s look at some of the benefits offered by bridging finance solutions and what property opportunities they can fund.

Benefits:

- Quick access to capital: provides borrowers with an immediate cash injection, ideal for completing a property purchase before selling.

- Flexible repayment terms: repayment can be tailored to suit the borrower's needs, including the length of the loan term and the repayment method.

- Interest options: interest charges can be paid monthly or more typically rolled-up and paid at the end of the term.

- Versatility: Bridging finance UK wide can be used for a range of purposes, including property purchases, renovations, business expansion and short-term projects.

- Bridging the gap: can bridge the gap between when a borrower needs funds and when they have access to longer-term funding, typically over a period of 1 – 12 months.

- Speed and efficiency: can be approved and completed quickly, from 3 days to 3 weeks

- Loan to value ratios: can provide high LTV ratios (up to 80% gross), allowing borrowers to secure significant funding based on the value of the assets being used as collateral

- No early repayment charges: though most will carry a minimum term (typically 1 to 3 months, but can be higher - check this with your lender and / or broker).

Bridging finance opportunities:

- Brownfield sites: sites previously developed but now disused often have high upfront costs to prepare the land for reuse, such as planning, demolition and / or removal of environmental liabilities

- Land without planning: use a bridge loan to purchase land with no planning, outline planning, or planning that you wish to vary. Once planning is obtained, you can decide to sell or refinance and build.

- Auction properties: auction purchases require 10% deposit upfront and completion within 28 days - a timescale no other finance type will meet

- Uninhabitable housing: houses without a working bathroom or kitchen are deemed uninhabitable and ineligible for traditional mortgage

- Can be used for both commercial and residential properties: most bridging lenders lend against residential property only, even if you have permission to convert to residential, but there are a number of lenders that will lend against commercial properties, think; light industrial, retail, commercial, care homes, hotels, etc.

Risks of bridging finance

As with all large-scale borrowing, there are pros and cons involved, so before arranging your property loan, it’s important to know the risks of bridging finance:

- Higher interest rates: typically have higher interest rates, which makes them more expensive than other types of loans.

- Secured loan: secured against assets, usually property, but can be other high-value assets such as artwork or jewellery

- Risk of default: If you are unable to repay the loan within the agreed repayment period, the lender can force the loan security to be sold

- Personal guarantee: most bridging loans require a Personal Guarantee, i.e. the borrower has personal liability. If there’s a shortfall between the property selling price and what the lender is owed, they can call on the personal guarantee

- Complex terms and conditions: can come with complex terms and conditions which can be difficult for some people to understand and manage

- Unregulated finance: when borrowing against assets that neither you or your family plan to live in then the loan will be unregulated. Whilst this can be a benefit because it allows for quick, flexible borrowing, an unregulated loan offers none of the consumer protection that a loan regulated by the Financial Conduct Authority has, such as compensation when sold an unsuitable product or given incorrect advice from lenders or brokers.

All bridging finance brokers UK wide have an obligation to inform you of the risks of bridging finance. Always seek bridging loan advice and speak to a broker to secure the best loan for your project. At Brickflow we work with some of the best brokers in the market – if you’d like to be put in touch with someone for your next project, get in touch.

How do you get a bridging loan?

If you think it’s the right type of finance for you, the next question to ask is how do you get a bridging loan?

Getting a bridging loan involves the following steps:

- Determine your eligibility: You’ll be required to provide information about your financial situation, including your income, expenses, and existing debt. However, a strong exit strategy is more important than borrower affordability, so poor credit history or low cashflow won’t always prevent you from applying for a bridging loan. But the stronger your financial position the easier it will be to secure a loan and usually with better terms.

- Shop around for lenders: Bridging finance is offered by a range of financial institutions, including banks, building societies, and specialist lenders. Compare the rates and T&C’s offered by different lenders to find the best deal.

- Prepare your application: To apply for a bridging loan, prepare a presentation detailing how the loan will be used to deliver a profitable outcome. Building costs, timescales and selling prices must be realistic – lenders know the industry. If the loan doesn’t cover all costs, show how you’ll reach the exit strategy.

- Submit your application: most lenders will have an application form that you (or your broker on your behalf) will complete - make sure all the details are accurate and that you provide all of the relevant supporting documents to boost your chance

- Wait for approval: If your application is approved, the lender will provide you with a loan offer, which will outline the T&C’s of the loan. You’ll then proceed to valuation and legals.

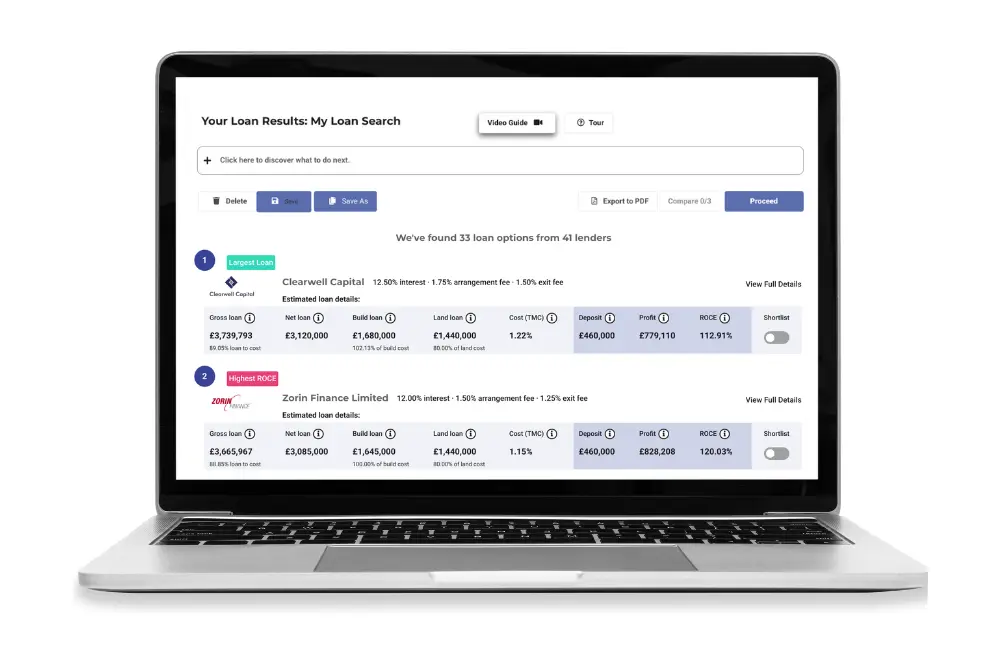

Before accepting an offer, carefully consider the terms and conditions of the loan, including the interest rate, repayment schedule, and any fees or charges. There’s over one-hundred bridging lenders, so talking to a specialist broker is the best way to navigate the market. At Brickflow we’ve created a tool for brokers and borrowers to search and compare the entire breadth of the market in minutes and source the best bridging finance deals available.

To find the bridging loan company offering the best deal for your situation, register with Brickflow or tell your broker about us, and see how we can help with getting a bridging loan.

If you’re a broker, sign up today and have a DIP on your desk by tomorrow.