True Cost of a Commercial Mortgage

Commercial mortgages work in much the same way as residential mortgages, with similar costs involved.

Typically, the costs that can be expected throughout the commercial mortgage process include:

- Interest charges: Rates typically range from 4+% (BTL) to 18% depending on loan size, LTV, property type, and lender (Q2 2026). Use Brickflow to see live rates for your specific deal.

- Arrangement fees: Around 2% of the loan amount

- Legal fees

- Valuation fees

When you search for a commercial mortgage on Brickflow, you can see accurate total repayment costs over the fixed term, including interest and capital repayments.

.png?width=1600&height=360&name=unnamed%20(24).png)

Similar to a residential mortgage, what you pay back will be considerably more than what you borrow, but this has to be weighed up against rental yield as well as potential capital growth.

Brickflow’s commercial property mortgage calculator can instantly show you whether or not your next investment property is viable.

Commercial Mortgage Example: How a Commercial Mortgage Works?

Commercial mortgages are a long-term finance solution that is repaid monthly with interest. The property that is acquired using the commercial mortgage acts as security for the lender, so if you default on the mortgage (stop paying it), the lender can repossess your property after a certain period of time.

A commercial mortgage is serviced using the income generated from the property, i.e., the monthly rental income. Lenders stress-test affordability by comparing the rental income with the monthly mortgage payment. This is unlike a residential mortgage, which is supported by the borrower’s income.

For owner-occupied commercial mortgages, the loan serviceability is tested against the business strength and trading accounts.

The term of the mortgage can be up to 30 years and will be decided when the loan is arranged. Monthly repayments will be determined by how much you borrow, how much deposit you put down, and the interest rate of the loan.

Commercial mortgages can be repaid as interest only or capital & interest. Interest can be fixed, typically for 2, 3, or 5 years. Alternatively, they can be secured on a variable rate meaning that they might rise and fall over the mortgage term.

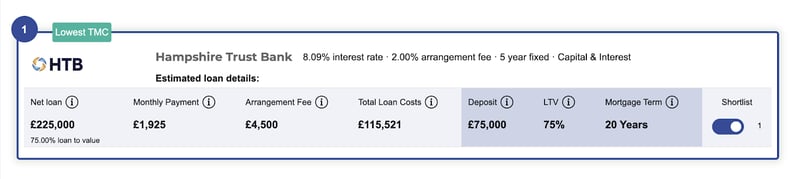

Looking at the below example helps to demonstrate how a commercial mortgage works:

- Purchase price of the property: £300,000

- Purchase costs: £15,000

- Mortgage term: 20 years

- Product type: Fixed for 5 years

- Repayment type: Capital & Interest

- Rental lease: 3+ years

- Gross monthly rental: £4000

Using the above numbers with Brickflow’s commercial mortgage calculator gives us an example loan of 75% LTV, with a 2% arrangement fee and an 8.09% interest rate. In this case, the monthly repayments would be £1925.

An owner-occupied example:

- Purchase price: £600,000

- Purchase costs: £30,000

- Mortgage term: 20 years, 5 Year Fix

- Repayment type: Capital & Interest

- Property type: Light industry, Midlands

- Adjusted annual EBITDA: £180,000

- Gross monthly rental: £4000

- Business trading: 2+ years accounts

These figures are indicative only. Use Brickflow’s commercial mortgage calculator to model your specific deal with live lender data.

"The benefit of Brickflow is instant information in a snapshot. You can see what various lenders are going to offer you, meaning you can move more quickly on deals and put an offer in."

"This is incredibly useful technology. Twelve months ago, we knew what lenders' pricing and appetite was - but today, in an ever changing market place, it's incredibly difficult to keep up."