Commercial mortgage terms play a central role in long-term deal performance, so we're looking at how lender fit and flexibility can shape outcomes.

Commercial Mortgage Terms: What Borrowers Need to Know

Understanding commercial mortgage terms helps borrowers compare lenders properly and improve decision making. Interest rates, term length, repayment structure, fees, covenants, early exit charges and refinancing flexibility can all affect the true cost and suitability of a commercial mortgage.

This guide covers the key commercial mortgage terms, how they differ across lender types, and what property investors, landlords and business owners should prioritise to suit their investment strategy.

What are commercial mortgage terms?

Commercial real estate mortgage terms are the set of conditions that define how the loan is structured, priced, repaid and managed.

Key terms include:

|

Term

|

What it means

|

|

Loan duration

|

The full commercial mortgage term lengths, typically 5–25 years

|

|

Interest type

|

Fixed, variable or tracker. Fixed rates give certainty for a set period, often 2, 3, 5 or 10 years. Variable rates can move during the loan term. Tracker rates usually follow a benchmark, such as the Bank of England base rate, plus a lender margin.

|

|

Repayment structure

|

Interest-only, or capital + interest

|

|

Amortisation period

|

The period used to calculate repayments

|

|

LTV

|

The percentage of the property value the lender will fund

|

|

Fees

|

Arrangement, valuation, legal and broker fees

|

|

Covenants

|

Conditions the borrower must maintain throughout the loan

|

|

Break clauses

|

Agreed points at which the loan can be reviewed or restructured

|

|

Early repayment charges

|

Fees for repaying before the agreed date (also known as exit fees)

|

|

Refinancing flexibility

|

How easily the borrower can move to another lender

|

Terms vary significantly depending on whether you’re borrowing from a high-street bank, challenger bank, specialist lender or alternative finance provider. Two loan offers on the same property can look very different once the full structure is compared.

How commercial mortgage terms vary between lenders

Different lender types have different characteristics on what commercial mortgage loan terms are available and which deals qualify.

Here’s what you can typically expect from each type of commercial mortgage lender:

Traditional high-street banks

- Longer terms and lower rates on qualifying deals

- Stricter underwriting, lower LTVs, stronger tenant covenants, established borrower track records

- Less flexibility on structure, property type or borrower complexity

- Better suited to stable, income-producing assets with straightforward ownership

Challenger banks sit in the middle ground:

- Moderate flexibility on structure and borrower profile

- Competitive rates, often faster credit processes than traditional banks

- More comfortable with limited companies, SPVs and properties that sit outside standard bank policy

- Useful where the deal is strong but the borrower or structure doesn't fit high-street criteria

Specialist lenders focus on deals mainstream lenders decline:

- Flexible underwriting and bespoke loan structures

- Comfortable with mixed-use, semi-commercial, complex portfolios and value-add strategies

- Higher rates and fees, but can offer stronger leverage and faster certainty

- Often the right fit where asset quality is good but the situation is non-standard

Alternative and private lenders prioritise speed and customisation:

- Most flexible on structure, often willing to lend where others won't

- Higher cost, but useful where timing, deal complexity or asset type rules out other options

- Can bridge gaps in the market for transitional or unusual assets

The right lender category depends on the deal, not just borrower preference. A lender that is competitive on a prime office investment may be the wrong fit entirely for a mixed-use block with a short lease

Which lenders are best for long-term investment holdings?

For portfolio landlords, pension-style investors and stable yield buyers, the priority is usually different from those chasing short-term returns. Long-term, semi-passive commercial holders typically care about stability, predictability and cashflow preservation.

Key features to look for if you’re holding commercial property long-term:

- Longer repayment terms: Fixed rates over longer periods offer predictable repayments and reduce exposure to rate volatility, and longer terms (15-25 years) improve stability

- Availability of interest-only structures: Reviewed periodically rather than fixed at outset, interest-only repayments can keep monthly outgoings manageable and preserve cashflow

- Low stress rates: Increase borrowing capacity against a given income

- Refinancing flexibility: The ability to move lenders or restructure without punitive exit costs

- Portfolio scalability: Lenders willing to consider multiple assets, cross-collateralisation or SPV structures

- Asset class tolerance: Appetite for the types of commercial property the investor holds or plans to acquire

High-street banks can serve long-term investors well where assets are standard and LTV requirements are modest. The trade-off is rigidity; strict covenants, limited flexibility and often less appetite for portfolio-level lending.

Challenger banks and specialist lenders tend to perform better for investors building larger or more varied portfolios. They’re more likely to offer interest-only periods, consider mixed-use income, and structure lending around the portfolio rather than individual assets.

Flexible commercial mortgage terms: what to look for

Flexibility in a commercial mortgage is not always visible in the headline terms. It becomes relevant when your plans change, for example a tenant leaves, a refinance opportunity arises, or you want to overpay and reduce the balance.

Factors that define real flexibility include:

- Interest-only availability: Keeps monthly payments lower and preserves working capital

- Variable and fixed-rate hybrids: Some commercial lenders allow part of the loan to be fixed while the remainder tracks the base rate

- Overpayment allowances: The ability to reduce the balance without triggering charges

- Covenant headroom: Lenders whose interest cover thresholds give breathing room if income dips temporarily

- Lease considerations: Appetite for shorter leases, multiple tenants or less conventional lease structures

- Mixed-use acceptance: Willingness to lend against properties with both commercial and residential income

- Portfolio cross-collateralisation: Using equity across multiple assets to support individual loan applications

Flexibility may be more valuable than a lower headline rate, depending on investment strategy. An investor planning to refinance in three years should not optimise for the lowest five-year fixed rate if early repayment charges make an early exit prohibitively expensive.

Read more on Researching Commercial Mortgages.

Specialist commercial mortgage lenders

Specialist lenders cover the asset types and borrower profiles that fall outside mainstream bank criteria. For property investors, this covers a significant portion of the market.

Asset types commonly handled by specialist lenders include:

- Mixed-use and semi-commercial property: Buildings with both commercial and residential elements, assessed on blended income

- HMOs and multi-unit freehold blocks: Higher unit counts or more complex tenancy structures than standard buy-to-let

- Development exits: Refinancing onto long-term debt once a development is complete but before full stabilisation

- Value-add acquisitions: Properties being purchased below market value with a plan to improve income or occupancy

- Refurbishment-heavy assets: Where the property needs work before it qualifies for standard commercial mortgage criteria

For complex deals, non-standard properties and situations where speed or certainty matters, specialist lenders often outperform traditional banks, structuring the loan around the reality of the asset rather than standard underwriting templates.

How to compare commercial mortgage lenders effectively

Comparing commercial mortgage lenders properly means looking at the full structure of the loan and whether it fits the deal.

A practical framework for comparison:

|

What to compare

|

Why it matters

|

|

Loan term

|

Affects monthly payments and total interest paid

|

|

Fees

|

Arrangement, exit and valuation fees change total cost significantly

|

|

Flexibility

|

Interest-only, overpayments, covenant headroom

|

|

Stress test rate

|

Directly affects how much the lender will offer

|

|

Covenants

|

Breach risk if income fluctuates

|

|

Early repayment charges

|

Cost of exiting before the fixed period ends

|

|

Speed

|

Time to DIP and completion varies widely

|

|

Property suitability

|

Not all lenders accept all asset types

|

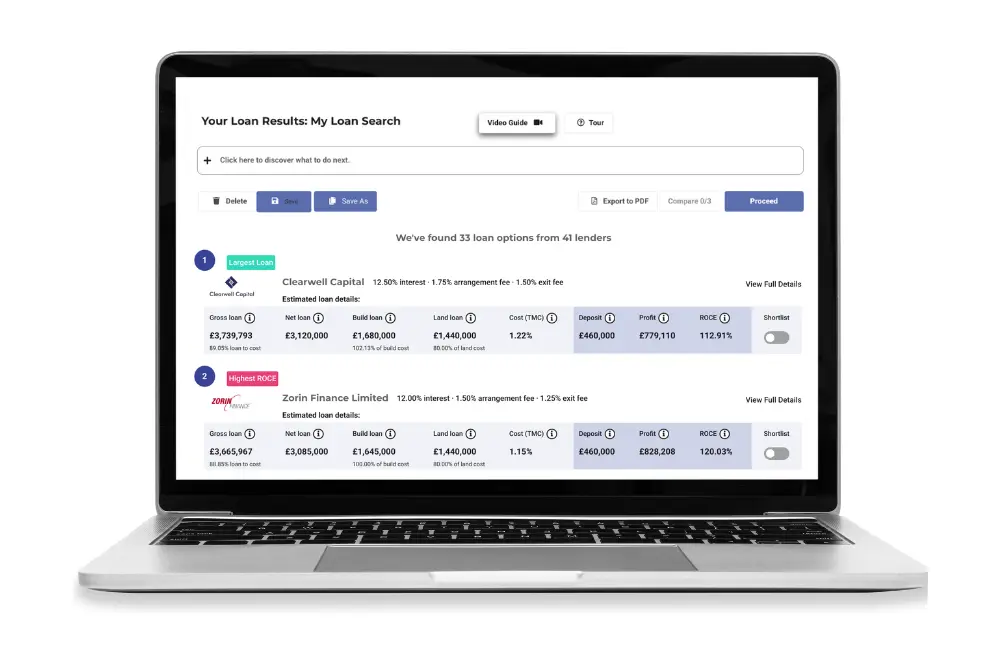

According to Brickflow's analysis of 100+ real-world £1m commercial property scenarios, the average net loan difference between the best and worst leveraged lender on the same deal is £151,000. Borrowers relying on manual loan sourcing, rather than comparing the breadth of the market, regularly leave significant funding, and capital efficiency, on the table.

Brickflow's commercial mortgage comparison tool lets borrowers and brokers instantly compare live loan options across 160+ lenders, covering rates, fees, LTV, stress test assumptions, and lender appetite, with results tailored specifically to the deal.

For borrowers considering development finance as part of a wider strategy, Brickflow also covers development finance lenders on the same platform.