Borrower Tips

Is property development a good career?

Is property development a good career? We’re speaking to a seasoned developer to find out.

Borrower Tips

Borrower Tips

A bridging loan for office property in the UK is commonly used when a buyer needs to move quickly on a commercial acquisition or when the asset does not yet meet criteria for long-term commercial finance. Read on to find out more about bridging loans for office property in the UK.

| What's in this guide |

Office purchases often involve timing challenges. A building may be available at auction, offered at a discount due to vacancy, or require refurbishment before a commercial mortgage lender will consider financing it. Bridging finance allows the acquisition to complete while the investor stabilises the asset.

Most office property bridging finance runs between 1 and 12 months, though many lenders go up to 24 months. Interest is typically structured as rolled-up (paid on loan redemption) or serviced (paid monthly) depending on the property and the borrower’s cash flow strategy.

Speed is one of the primary reasons investors choose bridging rather than a traditional commercial mortgage. Commercial mortgage approvals can take months because lenders perform due diligence on the property, lease agreements and borrower affordability analysis. Bridging lenders focus on asset value and exit strategy, allowing funding to complete significantly faster.

For auction or time-sensitive transactions, where completion deadlines are tight, bridging finance allows the property to be secured first, while long-term funding is arranged later, once the asset is stabilised.

Many investors therefore use commercial bridging loans for offices in a two-stage financing strategy:

Office purchases are widely eligible for bridging finance, but lender appetite depends heavily on the income profile of the building and the credibility of the exit strategy.

Vacancy is a pretty common reason for investors to use bridging loans for office property in the UK. Buildings with empty floors, short leases, or weaker tenant covenants can be problematic for securing traditional commercial mortgages.

Bridging lenders however, will adjust their underwriting accordingly to reflect the additional risk of a vacant or under-let office building. Like all bridging finance, the primary consideration is the exit strategy, so vacancy is unlikely to be a barrier to securing a loan, but it can reduce leverage and increase rates.

Partially let buildings can be easier to finance because existing tenants provide evidence of occupational demand and income stability.

Location is another major consideration, with hybrid working increasing vacancy risk in some areas. Lenders differentiate between:

This doesn’t mean commercial bridging loans for offices are limited to prime city-centre spots, but lenders may apply more caution for offices in secondary or weaker locations. If a borrower can demonstrate a clear strategy for improving occupancy, the application will be more appealing to lenders.

Lease structure also affects risk. Lenders review factors such as:

A building with several leases expiring during the bridging term introduces uncertainty around future income. Lenders therefore assess whether the local office market can realistically absorb the space within the project timeframe.

In practice, vacancy is not always a deal-breaker for office property bridging finance, but it is likely to impact the T&Cs of the loan, increase exit scrutiny and reduce LTV.

Demand for office space varies significantly between locations, and income stability can change quickly if tenants leave or leases expire, hence lenders factor in risk by assessing:

Let’s look at these in more detail.

Valuation is central to office property bridging finance because it determines both the loan size, the viability of the investment and the credibility of the exit strategy.

Where an office building produces stable rental income, valuers usually apply an investment valuation approach. They analyse the rent, lease profile, tenant and covenant strength. Longer leases with strong tenant covenants, like office space occupied by a large national corporation or global company headquarters generally support stronger valuations because the income is predictable.

For a vacant building, or building with short, unstable leases, the valuation may reflect a more transitional position. In these cases valuers rely more on comparable sales and the property’s current condition. Large voids increase uncertainty around future income, so lenders may reduce LTV and further examine the borrower’s leasing strategy and experience.

Bridging lenders have also recalibrated their valuation of office spaces in the post-covid market, with hybrid working changing the demand for space and how that space functions. Flexible set-ups, co-working, shared office spaces, and recreational areas are now the norm, so lenders want to see that.

Many office acquisitions involve repositioning before refinancing and bridging finance allows investors to complete these improvements during the short-term funding period.

Light refurbishment is common, including things like upgrading or adding communal areas, improving building services, or reconfiguring office layouts.

Environmental performance has also become increasingly important. Buildings with poor EPC ratings can struggle to attract tenants or refinance, so investors often use bridging finance to complete energy efficiency upgrades as well as social initiatives and greener governance strategies (ESG).

Tenant repositioning, like replacing weaker tenants with stronger occupiers, renegotiating leases, or subdividing larger floor-plates to attract smaller businesses is another way of de-risking an office property.

If the property was acquired with vacancy or short leases, leasing activity during the bridging term can strengthen the income profile ahead of refinancing.

Exit planning is one of the most important aspects of office property bridging finance, and lenders expect a clear route to repayment before approving any loan.

Office bridging loans are underwritten with the exit already in mind. A common exit is refinancing onto a commercial mortgage. A key question is whether the property will meet the requirements of long-term lenders by the time the bridge needs to be repaid.

Most commercial investment mortgages for UK office space operate around 60% LTV, and require a certain income cover ratio (ICR), with a margin of safety. Bridging lenders need to see that same deal viability to ensure refinancing is possible and will cover the debt owed.

Another option is to sell after refurbishment or leasing improvements increase the building’s value.

Some transactions involve a development-led exit, particularly where an older office building may be converted into alternative commercial or residential use.

A further strategy is partial pre-letting, where securing key tenants improves both valuation and refinance prospects.

The office market has become more selective, so lenders examine exit plans with a fine tooth-comb. It’s critical for borrowers to demonstrate realistic leasing assumptions or sales values to support their exit; offering additional viable exit routes can sometimes help secure bridging finance.

Yes, but the pool is smaller than for residential bridging. Many lenders active in residential or mixed-use have limited appetite for pure commercial assets like offices.

The lenders most likely to fund office purchases are challenger banks with dedicated commercial teams, specialist commercial bridging lenders, and non-bank funds.

Each varies on criteria, rates and the types of office they'll consider. Location matters significantly: lenders active in Central London offices may have no appetite for regional business parks, and vice versa.

Search office-ready bridging lenders on Brickflow to see which lenders are active in office finance for your specific deal.

Comparing office bridging offers requires looking beyond headline rate. Office valuations vary more between lenders than residential because fewer comparable transactions exist, particularly for secondary locations. Two lenders can quote the same rate but arrive at different net loan amounts because their valuations, risk pricing and total loan costs differ.

Compare rate, LTV, arrangement fees, minimum loan terms (some lenders charge a minimum of three to six months even if you exit sooner), valuation approach and completion speed.

If your exit is to refinance onto a commercial mortgage, check whether your bridging lender's valuation will be accepted by your refinance lender.

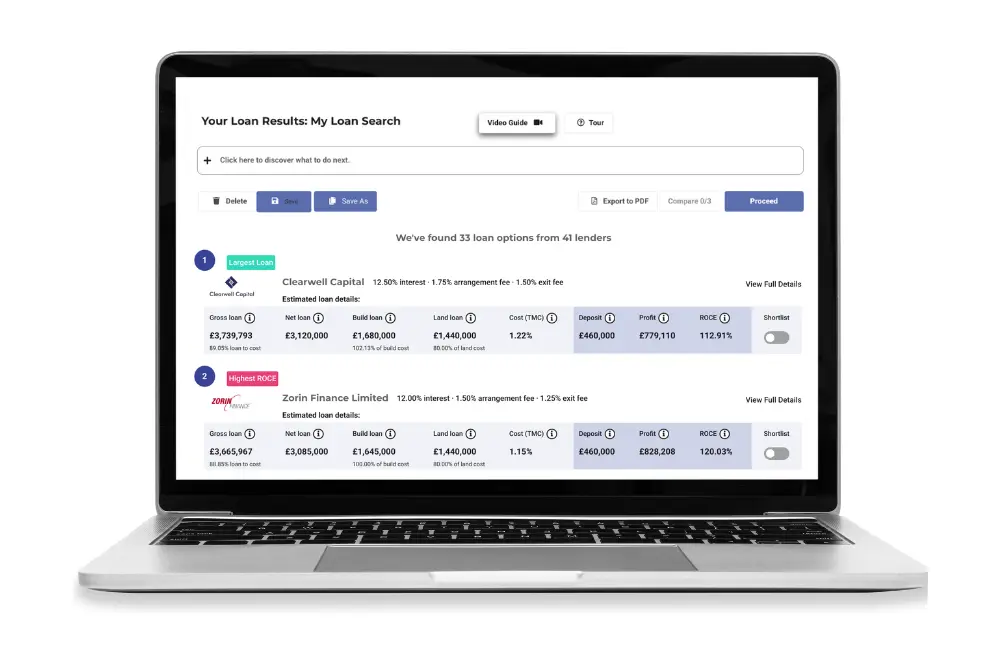

Brickflow lets you filter by commercial property type and compare like-for-like offers across office-active lenders in one instant search.

For a broader framework on what to look for, read our guide on how to compare bridging loan lenders in the UK.

Pricing for commercial bridging loans for offices reflects the level of risk associated with the property and the borrower’s strategy.

Compared with pure residential bridging, office transactions usually carry a modest risk premium because generally an office is more difficult to liquidate in the event of a default.

However, pricing may be similar to certain retail bridging finance, or mixed-use properties with a majority commercial share.

What Impacts Your Pricing Most?

Key factors influencing pricing for bridging loans for office property in the UK:

Bridging finance can be an effective tool for acquiring and repositioning office buildings, but it introduces risks that investors should consider.

One of the most obvious is market demand for office space. Changes in working patterns have affected how businesses use offices, creating varying markets depending on location and building quality, and increasing void risk.

If tenants leave or new occupiers cannot be secured quickly, the borrower may struggle to achieve the income levels required for refinancing. Bridging lenders want to be repaid, obviously, and it’s down to the borrower to ensure the building meets the criteria of commercial mortgage lenders by the end of the bridging term.

Another consideration is rental tone risk. If the investment strategy assumes significant rent increases, lenders will examine whether comparable evidence supports those assumptions.

Finally, valuation volatility can affect exit outcomes. Office values are sensitive to changes in yields, tenant demand, and economic conditions.

A realistic assessment of these risks leads to stronger financing outcomes and greater lender confidence. Using comparison platforms such as Brickflow to compare bridging loans for office property can help borrowers review deals from multiple lenders and assess whether the property investment is viable or not.

Not all lenders approach office assets in the same way and the differences between lenders can be significant. For borrowers seeking office property bridging finance, comparing lenders is therefore as much about discovering lender appetite as it is pricing.

Yes, there are bridging lenders who deal predominantly in commercial and office spaces, and others who have a broader spectrum. When it comes to office space, some lenders prefer to focus on income-generating investment properties, while others specialise in value-add opportunities, including buildings with vacancy, refurbishment requirements, or repositioning strategies.

Certain lenders are also more comfortable funding secondary or regional office markets, particularly where the borrower has a clear plan for improving the asset.

Maximum loan-to-value limits also vary across lenders. A lender's loan book at the time of application can impact the loan products available. For example, some might want to avoid over exposure to office deals if they already have plenty on their books, while others might be aiming to diversify from another dominant sector.

Because these differences are not always visible from headline criteria, comparing multiple office bridging loans is essential.

Comparing offers for a commercial bridging loan for offices involves more than reviewing the headline interest rate.

The total cost of borrowing should include arrangement fees, valuation costs, legal fees, and any exit charges. Borrowers should also consider flexibility around extensions, particularly where leasing timelines are uncertain. Underwriting speed can be another critical factor where purchase deadlines are tight.

Platforms like Brickflow allow borrowers to compare bridging loans across multiple lenders and identify the funding options that work for their particular asset, exit, timelines and borrower profile.

For office property investors, understanding lender appetite and comparing options across the market is key to securing the best bridging loan to suit each individual investment strategy.

Brickflow’s bridging loan calculator enables you to instantly compare live loans, assess the financial impact of different structures, see actual interest charges, and understand overall borrowing costs before committing to a lender

Is property development a good career? We’re speaking to a seasoned developer to find out.

Learn how to secure the best property development bridging loan with our comprehensive guide on tips, benefits, and key factors to consider for...

Can you get a bridging loan with bad credit? Yes, you can. This guide details how to secure a bridging loan despite poor credit.