Borrower Tips

Top development finance lenders

Discover how to identify the best development finance lenders in the UK for your project, maximizing profits and avoiding costly mistakes.

Borrower Tips

Borrower Tips

Mixed-use property offers strong investment opportunities, but it can also make financing more complicated. Buildings or sites that combine residential and commercial units often fall outside the criteria of standard mortgage lenders, particularly if the asset is vacant, undergoing refurbishment, or being repositioned.

This is where bridging loans for mixed-use property in the UK are commonly used. Bridging finance allows investors and developers to acquire or stabilise a mixed-use asset before refinancing onto longer-term debt or selling the property.

The key questions for most borrowers is how bridging finance works for mixed-use property in the UK, how lenders assess their specific deal, how it will be priced, and what exit strategy is required. This guide answers these questions and discusses why comparing loans from across the market is essential to get the best deal.

Yes, mixed-use property bridging loans are widely available in the UK, but bridging loan lenders assess these assets differently from purely residential or purely commercial property.

Bridging finance is designed as short-term funding, typically ranging from 1 to 24 months, allowing borrowers to secure a property while they stabilise the asset or implement a strategy that makes it suitable for long-term finance. In other words, it’s often a transitional transaction tool.

For mixed-use buildings, bridging loans are commonly used to:

Typically, lenders offer rolled-up or retained interest structures, meaning interest is added to the loan and paid on loan redemption, rather than paid monthly. This is particularly useful where the property is not yet income producing.

In mixed-use situations, lenders usually analyse the residential and commercial elements separately. The residential/commercial split, or the commercial weighting, can influence how the loan is structured and which lenders are willing to fund the deal.

Mixed-use bridging finance is often the only viable option when the building is not yet eligible for standard mortgage finance.

Bridging is frequently used to unlock deals that have issues preventing them from securing funding from long-term lenders, such as:

In these scenarios, bridging loans for mixed-use property UK-wide act as the flexible capital needed to acquire the property and stabilise it before moving onto a standard or semi-commercial mortgage once the asset meets long-term lending criteria.

Mixed-use bridging loans require more detailed underwriting than purely residential bridging because the lender must evaluate both the commercial and residential components of the asset.

Several factors typically drive lender appetite and loan terms.

One of the first things lenders consider is the percentage split between the residential and commercial spaces.

Properties with a higher residential proportion are often considered lower risk because residential demand and financing options are generally stronger. For example:

Higher commercial exposure can affect:

Lenders will scrutinise the stability of the commercial income, the type of business, the strength of the tenant covenant, and the current rental yield to determine the overall risk profile and subsequent pricing.

Mixed-use buildings are frequently purchased with the intention of changing the use of part or all of the property.

A common example is converting commercial space into residential units, either through planning permission or permitted development rights.

Bridging can be an ideal fit for any planning uplift strategies, but lenders will want clarity around:

When planning risk is involved, the lender's comfort hinges on one thing: exit clarity. Since the value of the asset may depend on successful planning approval, lenders must trust that if it fails, you have a solid Plan B (like refinancing the current mixed-use structure or selling it as is).

The strength of your exit strategy can often outweigh the asset’s complexity, and your borrower profile. Naturally, lenders want certainty that they will be repaid. The most common and preferred exit strategies for mixed-use bridging finance include:

Nonetheless, lenders will assess your track record. An experienced developer with a clear, well-articulated strategy has more chance of loan approval, more favourable terms and potentially better pricing than a novice investor can secure, even on the same asset.

Like all bridging finance, pricing for mixed-use bridging loans varies depending on the risk profile of the deal. Because these assets combine residential and commercial elements, they involve a different underwriting process from purely residential or purely commercial property, and hence different rates.

Generally, bridging loans for mixed-use properties carry a modest complexity premium compared with single-use residential buildings, so rates tend to be higher.

This is because fewer lenders are active in the mixed-use property space, valuations are more complex, additional underwriting is required, and they carry higher perceived risk due to:

While pure residential bridging loans typically have the lowest rates across bridging finance, and commercial-only bridging tends to be the most expensive, mixed-use bridging typically sits between the two.

If the residential proportion is high and the exit is straightforward, pricing can be comparable to standard bridging loans. Respectively, properties with a high commercial weighting or planning risk may be priced closer to commercial bridging finance.

Rate premiums vary, but a mixed-use bridge at 65% LTV might price 0.1% to 0.3% per month higher than a comparable single-use residential deal. That said, the spread between lenders on mixed-use is also wider, which means the difference between shopping the market and going with the first offer is often greater than for standard deals.

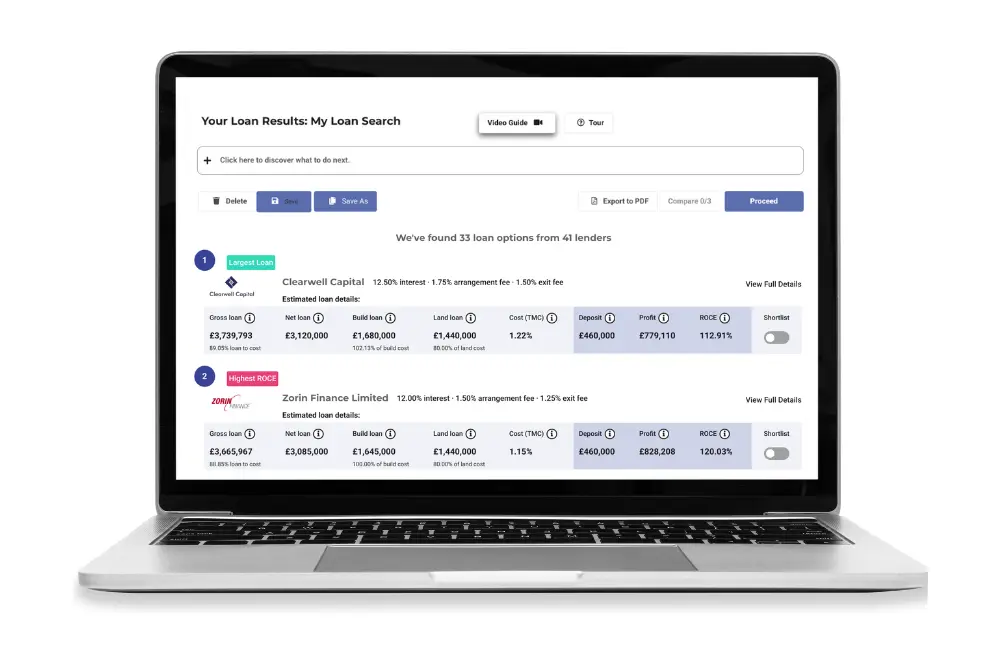

Brickflow filters lenders by property type, so you can instantly see which lenders fund mixed-use and compare their rates against single-use options for the same loan amount and LTV.

Read more about the difference between commercial and residential bridging loans.

Several factors typically influence the cost of bridging finance for mixed-use development or investment.

Key variables include:

Whether you’re buying and refurbishing part or all of a mixed-use building, bridging finance can be structured to cover both the property purchase and the subsequent refurbishment works.

Refurbishment bridging loans can typically cover up to 75% of the property purchase value, and up to 100% of the refurbishment costs. How it works depends on the scale of your project. Some lenders may determine whether the refurbishments are light or heavy based on the cost of the refurbishment works – anything less than 15% of the value of the property would be considered light.

Light refurbishment

Lighter refurbishment projects usually involve internal upgrades like replacing bathrooms and kitchens, cosmetic works, improving EPC ratings, or reconfigurations that don’t require planning permission. The bridging facility might be structured with an initial advance to cover the purchase price (minus your deposit) followed by the funds for the refurbishment work after the property sale is completed.

Heavy refurbishment

Heavy refurbishment work generally requires planning permission like structural changes, change of use, extensions, garages, and conversion. Refurbishment bridging loans work more like development finance with staged drawdowns. This means funds for the refurbishment works are released in stages linked to construction milestones, and verified by a Monitoring Surveyor. This ensures cost control and that the lender's security is increasing alongside the asset's value.

Your loan application must cover the level of work: a simple cosmetic refurbishment is treated differently from a structural redevelopment, has a lower-risk profile and can be funded with a straightforward ‘fix and flip’ bridging loan. Heavy refurbishments involve additional third parties, project monitoring and different LTV caps.

Not all bridging finance lenders approach mixed-use property in the same way. Some specialise in semi-commercial assets, while others focus primarily on residential bridging and may have strict limits on commercial exposure.

Understanding lender appetite can therefore be just as important as comparing headline interest rates.

You need to compare lenders based on their appetite for your specific deal, looking at:

Comparing bridging loan options for mixed-use property developments in the UK is essential to find the best deal for your property investment, and there are a number of ways to do this.

Work with a Specialist Broker: A broker specialising in commercial and complex property finance understands the bespoke criteria of lenders, and gives you wider access to the bridging loan market.

Use a comparison platform: Platforms like Brickflow allow investors and developers to compare bridging lenders across the market, giving unbiased, like-for-like details on rates, fees, LTVs and lender criteria

When comparing mixed-use bridging finance, look at all costs rather than just the rate, which means factoring in arrangement fees, exit fees (if applicable), legal costs, and monitoring surveyor fees to compare the true total cost of the loan.

Also, prioritise speed and certainty–the right lender is one who can process the specifics of your mixed-use deal quickly and provide certainty of funds, rather than the cheapest loan.

To understand more about how to compare loans and lender suitability, head to our bridging loan comparison page, and for detailed and accurate loan figures and costs, run your numbers through Brickflow’s bridging loan calculator.

Discover how to identify the best development finance lenders in the UK for your project, maximizing profits and avoiding costly mistakes.

What are fix and flip loans? Discover how fix and flip loans work, their benefits and risks, and tips for securing these loans to succeed in property...

Discover how bridging loans can finance your barn conversion. Learn about costs, benefits, and application tips for turning your rural dream into...