Thanks to changes to permitted development rights for agricultural buildings in early 2024, barn conversions have become a lot more feasible. In this blog we look at using bridging finance to fund a barn conversion project.

Bridging Loans for Barn Conversions: Financing Your Dream Project

Converting a disused barn into a residential home or another commercial space can be a lucrative project or a way of developing your dream home. As well as unique character, spacious rooms and idyllic rural settings, barn conversions can preserve historical architecture and bring new life into the countryside.

However, using a mortgage for barn conversion can be difficult, if not impossible. Mortgage lenders only accept habitable properties (watertight with working kitchen and bathroom) of standard construction. Naturally, most barns don’t meet these criteria.

Bridging loans for barn conversions can offer a viable funding solution.

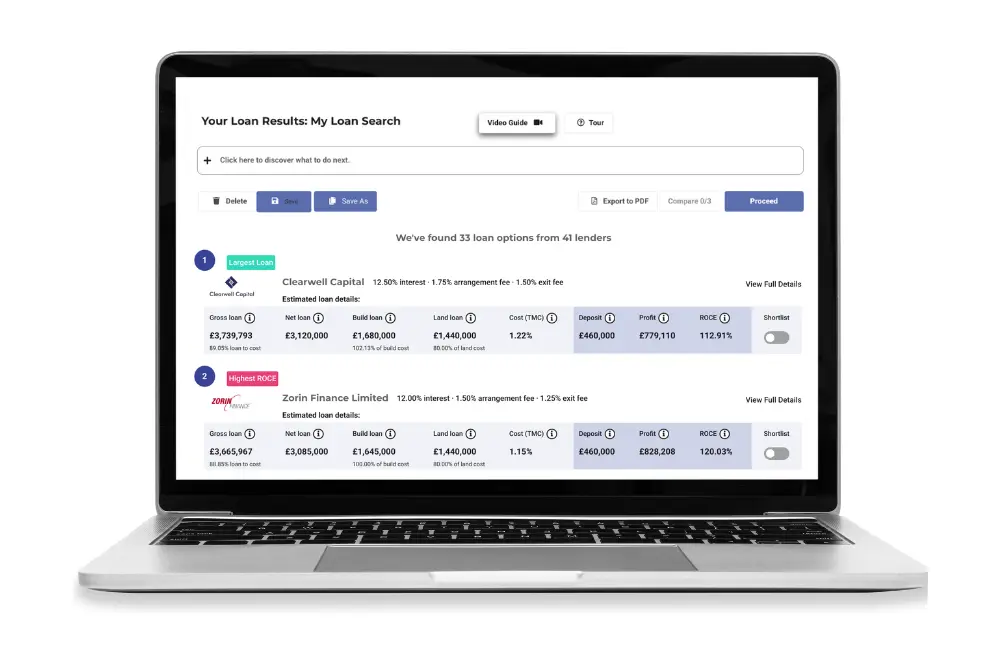

Search & compare bridging loans for barn conversions on Brickflow.

Understanding bridging loans

Bridging loans are fast, flexible, short-term finance arrangements.

When bridging loans first arrived on the market back in the ‘60’s, they were intended to ‘bridge the funding gap’ between buying and selling a property.

Today, they fund vast and varied property transactions and projects, from straightforward purchases to property flipping, buying land, auction purchases or facilitating a fast sale.

Since bridging loan lenders consider properties in all conditions, and are not restricted to habitable properties, bridging loans for barn conversions can be an ideal solution.

The loan is repaid in full at the end of the term, by which point, your barn conversion is complete, enabling you to sell or refinance on a residential or commercial mortgage.

Converting a barn into a commercial space is much less common than residential, so the loans are likely to take longer to approve and be more expensive.

Benefits of bridging loans for barn conversions

Whilst bridging loans for barn conversions are not the only finance option available to you, they do offer a handful of benefits:

- Fast: Quick arrangement makes bridging loans ideal for buying a barn at auction, or outbidding competitors on contested properties, as well as enabling you to start your project sooner.

- Flexible: Open-ended bridging loans can be repaid at any time within the maximum term, and early repayment charges are not common. Unlike mortgages, they can be secured against a wide range of property types and conditions.

- Save capital: Bridging loans for barn conversions can partially fund the property purchase as well as cover the renovation costs, meaning less capital contribution. Read more on our Refurbishment Bridging homepage.

Alternatively, bridging loans can act as an interim solution to purchase the barn before moving on to development finance. Development finance is suited to more extensive projects, with full planning permission. The application process is more complex and loan completion takes longer than bridging.

Lenders might tell you if your project requires a development loan rather than bridging. Generally, a barn conversion will be considered ‘heavy’ refurb, so check that your lender offers this type of loan.

How bridging loans work

Bridging loans for barn conversions work like any other bridging finance, and offer the same key features:

- Loan term: Typically 1-24 months (up to 36 or 60 months in some cases)

- Loan amount: £25,000-£100 million

- Loan-to-value: Up to 75% gross LTV (plus up to 100% of build costs with refurbishment bridging)

- Completion: Typically 1-6 weeks (or days if everyone pulls in the same direction)

- Interest: Rolled up or serviced

- Exit: Sale or refinance

If you have the equity to cover the cost of the works, a straight purchase or refinancing bridging loan can work. However, to fund the purchase and conversion costs, refurbishment bridging finance might be more suited. Depending on your project and scope of work, it will either be light, medium or heavy refurbishment finance.

With refurbishment bridging, lenders can offer up to 100% of the costs of the works, plus up to 75% gross loan of the purchase price. How much you can borrow is determined by:

- The barn’s value, condition and location

- The scale of your project and the costs of the works

- Your previous experience

- The gross development value (GDV)

- The lender’s lending caps

The loan is secured against the barn or other collateral. The lender can repossess these assets in the event of a default.

It’s typically drawn in one lump sum, but for heavy refurbishment projects, lenders might agree to release the loan in stages (like development finance) to align with your work schedule. In which case, lenders can appoint an Independent Monitoring Survey (IMS), who regularly inspect the refurbishment site to ensure the work is proceeding according to schedule and specifications. If the IMS sees work is not progressing as planned, they can withhold the next stage of funding.

Bridging loans for barn conversions that will be the borrower’s (or their family’s) home are regulated, therefore therefore knowing the borrower can obtain a residential mortgage for the same value as the bridge loan is important.

Otherwise, in some circumstances, lenders can carry out a desktop valuation and use title indemnity insurance, therefore the loan can be approved in a matter of days. This would only be possible in less complex property transactions.

Costs and Fees

Bridging loans for barn conversions are often secured against dilapidated properties, with no immediate income-producing possibility, and are reliant on the borrower’s ability to complete the renovation project.

They are therefore higher risk to lenders. This, plus the quick arrangement time frames, means bridging loans have higher rates and fees than traditional borrowing. However, they don’t cost as much as you might think, and the opportunities offered can outweigh the higher costs.

Costs and fees for a bridging loan for barn conversion include:

Interest Charges

Most lenders offer retained interest, meaning interest charges for the entire term are calculated upfront and deducted from the gross loan amount. Alternatively, interest can be rolled-up and paid at the end of the term. Serviced bridging loans (paid monthly) do exist, but they are less common.

Interest is calculated daily, so you only pay for the duration of your loan, even if you exit the loan early. The interest is compounded (interest is paid on interest), so you’ll pay more than if you service the loan.

The rate of interest on your loan will depend on:

- The property

- Your project

- The LTV (Loan to Value)

- Your loan term

- Your exit strategy

- You as a borrower

Other bridging loans costs

- Valuation or survey fees: A surveyor assesses the property on behalf of the lender, with costs depending on the property value, type, location and complexity.

- Legal fees: The lender’s as well as your own.

- Broker fees: Normally paid by the lender.

- Arrangement fees: Up to 2% of the gross loan and deducted at completion.

- Exit fees: Not that common for bridging finance but there can be a minimum loan term – between 1 & 6 months normally.

In order to repay your loan at the end of the term, ensure your exit strategy is realistic and achievable.

Barn conversion costs

- Purchase costs

- Price of the barn and land

- Stamp Duty Land Tax (STLD)

- Other professional fees, such as planning consultants

- Renovation / conversion costs

- Labour and material

- Equipment hire

- Professional fees, such as architects and designers

- Specialist contractors if required

There are many factors that determine your total barn conversion costs. Thorough research and detailed costings from the outset is crucial, as well as having adequate contingency funds (typically 20%) – old buildings often reveal unseen problems once the work begins.

Application process

The application process for a bridging loan for barn conversions is the same as for other bridging loans.

Firstly, search the market and model your deal against live borrowing options to make sure it’s viable. Brickflow’s bridging loan calculator enables you to do this in seconds and prevents you from taking on a losing project or presenting it to lenders.

When you’re sure your deal stacks, you can begin the application process:

- Submit your project appraisal: Demonstrate a profitable project to lenders by comprehensively covering your barn conversion, from build costs and timelines. Include market research and comparables, as well as your previous property experience.

- Terms offered: Lenders will return with their initial Decision in Principle (DIP). At Brickflow, you can receive multiple DIPs within minutes of applying, and progress to approval on the same day. Your intermediary can help explain the T&Cs of each DIP, and negotiate with lenders if necessary.

- Approval: The lender will conduct due diligence on you as a borrower, and instruct valuers to assess the barn being purchased, the project and any additional security assets. The valuation will determine their lending parameters.

- Loan drawdown: Funding typically takes around 14 days to be released, though it can be either a longer or shorter timeframe. It is dependent on the valuer completing their report, the solicitor’s property searches and any deal complexities. You can draw the loan immediately upon approval and begin your barn conversion according to the scope of work set out in your application.

Once the work is complete, the loan is repaid in full, either by the sale of the converted barn or by refinancing onto a residential, BTL or commercial mortgage.

At Brickflow, we’ve streamlined the search and application process into a single online journey, saving you hours of time applying to individual lenders, several of which might not be able to meet your requirements anyway. If you’d like to apply for bridging finance through Brickflow, we can connect you with any of our broker partners, who will facilitate and manage your application process.

Finding the best rates

When it comes to finding a bridging loan for a barn conversion, it’s easy to focus only on finding the best rates. However, the lowest interest rate doesn’t necessarily mean the best loan.

Securing a higher LTV, or 100% of the build costs can significantly reduce your capital input to give you more flexibility for your barn conversion, or the ability to invest elsewhere simultaneously.

Finding the best bridging loan for a barn conversion involves searching market-wide, including banks, non-banks and specialist lenders. Brickflow is the quickest, easiest way to search over 150 lenders and apply with your intermediary or a Brickflow broker partner.

Here’s how:

-

-

- ENTER your project criteria and model your deals

- COMPARE loans from 150+ lenders

- APPLY for a loan with your intermediary (or Brickflow partner)

The following might help you secure more favourable terms and rates with lenders:

- Good credit history

- Good financial standing

- Strong assets position and ability to offer additional security

- Proven experience of similar successful projects

- Working with a professional team with good portfolios or work

- Higher deposits (rates are typically lower with 40% deposit contribution or more)

Try our bridging comparison tool today to find the best bridging loans for barn conversions.

Secure your bridging loan for barn conversion

Converting a barn is a great way to bring an old building back to life and create a one-of-a-kind home, or new commercial space, but getting the finance right is key to a successful conversion.

Whether funding the purchase and development or simply facilitating a fast purchase, understanding bridging loans for barn conversions increases your options.

If you’ve found the barn, but have no idea where to find your finance, use Brickflow’s instant bridging loan calculator. It tells you how much you can borrow and at what cost, so you know if your barn conversion is viable before committing to it.

Run your barn conversion project numbers through Brickflow today.

FAQs

What is the typical interest rate for a bridging loan?

The interest rate you secure depends on several factors: the lender you use, the size of the loan, the property and its location and condition, the loan term and you as a borrower.

Currently, interest rates for bridging loans are from 0.58% per month (Q3 2025).

Can I get a bridging loan if I have bad credit?

It’s possible, yes. When considering bridging loan applications, lenders primarily focus on the project and whether or not the exit is viable.

However, lenders will examine your assets and liabilities, your current credit situation and also your past experiences in property development. If you have bad credit you are less likely to secure the best rates and loan terms.

How quickly can I get access to funds?

The loan can be drawn immediately upon application approval. The most common timeframe for unregulated bridging loans to be approved is two weeks, but it can be quicker or slower.

A straightforward purchase, with no complexities such as, in the case of barn conversions, agricultural restrictions, right-of-way access or listed buildings, can be completed within days. Lenders can sometimes use a desktop valuation (automated valuation model) and title indemnity insurance rather than legal searches.