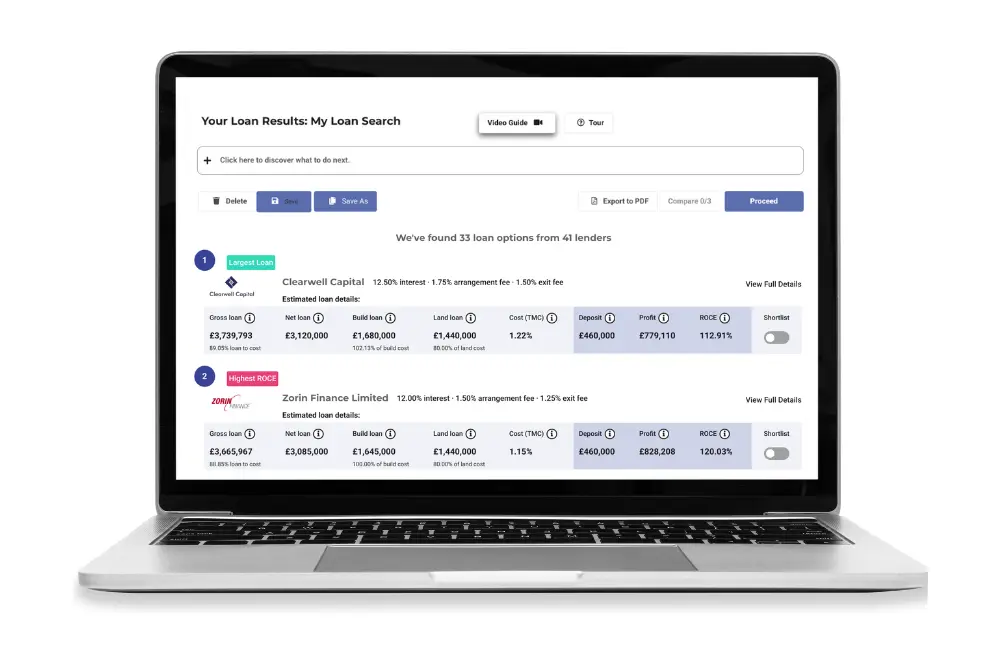

When you’re working against a deadline, The fastest way to secure bridging finance for a property acquisition is to search the whole market at once rather than approaching lenders individually. Brickflow lets you compare bridging loans from 160+ UK lenders in under 60 seconds, receive same-day Decisions in Principle, and apply to multiple lenders simultaneously through Smart Appraisal.

How to identify and shortlist fast bridging lenders

Where the traditional process of broker calls, individual applications and waiting on responses can take two to four weeks, Brickflow compresses the search-to-DIP stage into a matter of minutes.

When you're working against a deadline, whether it's an auction purchase, a prime development plot, or a deal that just won't wait, that speed advantage is the difference between securing the asset and losing it.

In urgent property transactions, it's easy to just settle for any loan, or be swayed by lenders promising to arrange a loan in ultra-fast timescales. But the what seems the fastest route is not always the right one. Deal structure, lender fit and real-time comparison can help secure funding without creating problems later or costing you tens or hundreds of thousands of pounds on the wrong deal.

This guide explains what ‘fast’ really means in bridging finance, which lenders are built for speed, and how to search the breadth of the market and shortlist options quickly without compromising on deal quality.

What counts as ‘fast’ in bridging finance?

Speed in bridging finance is relative to the deal.

At the very sharp end, some loans can complete in 3–5 days. This could only happen with unregulated bridging on straightforward cases, with experienced borrowers, and minimal underwriting friction.

More commonly, fast bridging finance in the UK completes in 7–14 days, especially where valuations or legal work introduce additional steps.

What determines where your deal sits on that spectrum comes down to a few key factors:

- Valuation approach – desktop or automated valuations can significantly reduce timelines, while full inspections add time

- Legal complexity – multiple titles, leasehold structures, or planning issues slow things down

- Borrower readiness – clear documentation, defined exit strategy, and experience all help lenders move faster

The important point is that speed is achievable, but it’s not automatic. Even the fastest lenders rely on well-structured deals to deliver quick completions.

When speed matters most (development plots, auctions, time-sensitive deals)

Fast bridging lenders are typically used when timing directly affects whether a deal can be secured or not.

Auction purchases are a clear case. Completion deadlines are fixed, often within 28 days, and traditional lenders are rarely set up to meet that timeline, while bridging lenders for auction purchases are structured specifically for this type of transaction.

Speed can also matter when securing a development plot. Opportunities often come with competition or tight seller expectations, and delays in funding can mean losing the site entirely. Land bridging loans allows investors to move before longer-term development funding is arranged. If you need short-term finance to secure a development plot quickly, comparison platforms like Brickflow can help you search the market instantly, and shortlist worthwhile lenders that offer planning bridging.

Speed can also matter when securing a development plot. Opportunities often come with competition or tight seller expectations, and delays in funding can mean losing the site entirely. Land bridging loans allows investors to move before longer-term development funding is arranged. If you need short-term finance to secure a development plot quickly, comparison platforms like Brickflow can help you search the market instantly, and shortlist worthwhile lenders that offer planning bridging.

There are also opportunity-led acquisitions, such as below-market deals, distressed assets, or time-sensitive negotiations, where speed becomes part of the commercial strategy, not just a logistical requirement.

In all of these scenarios, traditional finance tends to fall short. Processes are slower, criteria are tighter, and underwriting isn’t designed for urgent completions. Bridging sits in that gap, offering a way to secure the asset first and refinance later.

Which lenders specialise in fast bridging finance?

If you’re trying to understand which lenders specialise in fast bridging finance for UK property investors, it helps to focus on lender type rather than specific bridging lender names.

Specialist bridging lenders

These lenders are built around short-term property finance and often prioritise speed as part of their model. Streamlined underwriting, internal decision-making, and specialist bridging solicitors allow them to move quickly on suitable deals.

Private and alternative lenders

Alternative lenders, including those specialising in bridging can also be relevant, particularly in complex deals. They tend to be more flexible than traditional banks, can often offer higher leverage and can make quick credit decisions, especially when there is a clear relationship or a strong track record behind the borrower.

High-street banks

Many high-street banks don’t advertise their bridging products, and they are often only available to existing customers. Deposit-backed funding lines are subject to more regulation, and their processes are often geared towards lower-risk, longer-term lending, which naturally introduces delays. Hence high-street banks often can’t meet fast timelines.

In practice, lenders that can move quickly tend to prioritise:

- Simple or well-understood assets

- Clearly defined exit strategies

- Experienced borrowers with a track record

Rather than searching for fast bridging lenders in isolation, identify lenders who operate in the asset and transaction type specific to your deal. Using a comparison platform enables you to narrow that down at the start.

How to shortlist lenders for a fast deal

When timing is critical, the shortlisting process needs to be focused and structured.

Start by clearly defining the deal:

- Property type and condition

- Required loan amount and leverage

- Timeline to completion

- Exit strategy

Once that’s clear, use a comparison platform to filter lenders based on their ability to deliver within your timeframe. A good property finance platform searches the breadth of the market in seconds.

Key criteria to assess:

- Proven speed – do they have a track record of completing in days, not weeks?

- Valuation approach – can they use desktop or automated valuations where appropriate?

- Legal efficiency – do they work with experienced legal teams familiar with bridging timelines?

- Relevant experience – have they funded similar deals before?

When you know how to shortlist bridging lenders quickly, a broker can then offer better insights of each lender on your shortlist.

At this stage, it’s also important to look beyond the headline rate. Speed often comes with trade-offs in pricing, structure, or flexibility, so comparisons need to be made on a like-for-like basis.

Moving quickly without making costly mistakes

Urgency can push borrowers toward the first available option, but that’s where mistakes tend to happen.

Common issues include:

- Proceeding with a lender who can’t actually meet the timeline

- Overlooking total costs

- Not properly validating the exit strategy

Read more about avoiding costly mistakes in The 6 Fatal Mistakes Property Developers and Investors Make (And How to Avoid Them).

Even in fast-moving situations, decisions still need structure. A lender that can complete quickly but doesn’t fit the deal can create problems later, particularly when it comes to refinancing or exiting.

The goal is to combine speed with suitability.

Comparison tools like Brickflow allow borrowers to compare lenders based on speed, criteria, and deal fit in one place. This reduces time spent on manual research and helps move from a broad search to a focused shortlist faster.

For time-sensitive deals, that shift from urgency to speedy structured decision-making is often what determines whether the opportunity is secured or missed.