After discussing how slow transaction cycles are restricting businesses, we’re now exploring another issue property investors face - a liquidity crunch. Higher interest rates (even with the latest base rate decrease) translate to larger equity inputs on every deal with debt attached. But despite the lack of liquidity, opportunities are out there.

So what is a liquidity crunch?

We’ve all heard of a credit crunch, with 2008 being the prime example. Dubious lending habits spurred a global recession and credit availability plummeted, with lenders withdrawing products faster than NINJA's bought beachside condos in the previous years.

However, a liquidity crunch is very different. Despite the prolonged period of economic instability, from inflation to the soaring living costs, lenders have remained fully open for business. In fact, data from The Bridging and Development Lenders Association shows that bridging loan books are ballooning, with a record high of £8.1 billion in Q1 2024. That’s 6.8% higher than the previous quarter and nearly double the £4.48bn recorded in Q1 2022.

So rather than a lack of available credit, there’s a lack of cash amongst property developers and investors, in other words, a liquidity crunch.

The slower sales market combined with protracted transaction cycles, as well as higher costs of living, are all restricting borrower liquidity.

However, the most significant contributing factor to the cash shortage is higher interest rates.

Looking at the numbers - a £3 billion gap

Despite the recent news of the base rate drop, comparing where interest rates have been sitting and where they were a couple of years ago, there’s still been a c.5% upward shift. Per £1 million of borrowing, that’s £50k per year extra in interest charges.

For development finance and bridging finance, where interest isn’t paid monthly but is part of the loan, it means borrowers now need to put in an extra £50,000 per £1m of borrowing in equity to secure the same priced property as 2.5 years ago.

Considering the UK development finance industry as a whole, worth approximately £9bn per year in new borrowing, rate increases signify approximately an extra £450m in equity that developers need today compared to 2 years ago, to build the same number of houses.

Add bridging finance, c. £7.5bn of new transactions per year, and commercial mortgages, c. £ 45bn of new transactions per year, then you have a colossal equity gap of over £ 3bn - which is the main reason CRE transactions have fallen.

The recent 0.25% decrease in the base rate from 5.25% to 5% will start to have a more positive, reverse impact, although in much smaller increments. A 0.25% drop per £1 million borrowed per year equates to a £2500 reduction in interest costs, so a £5m development loan over 20 months means deposit requirements drop by £20k. Assuming that all lenders adopt the cut in their pricing.

Brickflow’s CEO and founder, Ian Humphreys, delves into the issue of the liquidity shortage in more detail on Property TV’s Election special. Ian also raises an interesting and realistic joint venture solution for the government to provide equity support for SME developers.

Watch the full episode:

How a government equity bank could boost building

The extra funding burden is currently being shouldered by the private sector, and is significantly holding developers back.

The average property development loan in the UK is £5 million, so developers could be asked to find an extra £500,000 over a typical two-year loan term. This is a huge outlay and directly reduces the available equity for other projects, and ultimately increases the price of housing delivery.

As Ian discusses in the Property TV episode, a government Joint Venture could cover the equity deficit. If it were to establish a £450 million equity bank to support SME property developers – a relatively small amount for public finances – it could take equity stakes in development projects on reasonable terms, and allow developers to access the necessary funding without the high cost of profit shares that would be commonplace in the private sector.

The fund would not only support the continued development of housing but also deliver it quicker than any of the new Labour government's proposals. It’s an innovative way to leverage government resources to maintain momentum in the property sector.

The fund would not only support the continued development of housing but also deliver it quicker than any of the new Labour government's proposals. It’s an innovative way to leverage government resources to maintain momentum in the property sector.

The effect of a liquidity crunch on a developer’s career

Recycling equity is the lifeblood of any developer's career. Slower sales (as we discussed in our previous Industry Insights) and increased equity requirements mean developers don’t have any equity to recycle, holding them up from moving on to their next project.

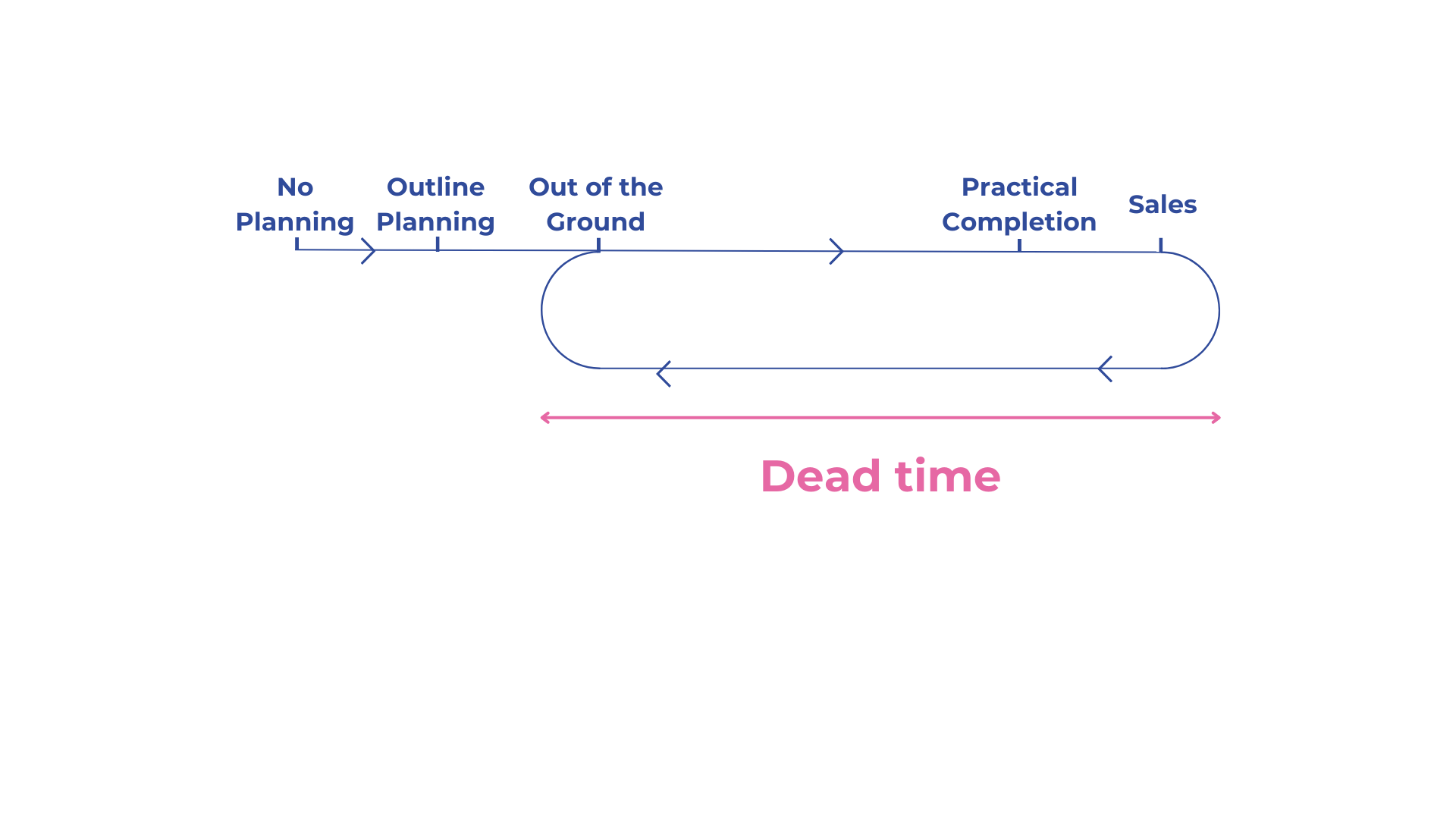

The below illustration, The Developer Lifecycle, shows the dead time between sales and getting the next project out of the ground.

The Developer Lifecycle

If this circular route expands, the amount of projects a developer completes is drastically reduced - think of the financial impact of completing a project every 4-5 years instead of every 2-3 years.

This means it's more crucial for borrowers to be educated on how to structure their finances to maximise efficiency and output. By minimising equity input, reducing the risk of dead time, and spreading their investment over multiple schemes, developers are able to maximise their profitability over their development career.

By supporting SMEs, not only does the government help kick-start the economy they also deliver the houses society needs. Win, win.

The opportunities are still out there

Here’s the thing though - savvy investors who know how to find better finance, and they or their advisers model every project (perhaps on Brickflow!) before pursuing a deal, are setting themselves up for success.

The reality of a lack of liquidity means that people are having to de-lever - developers no longer have the cash to hold onto sites they acquired for future projects. They need to cash out to get moving on other projects, meaning many developers are offloading decent sites that they would otherwise have developed.

Similarly, in another bid to access their equity, developers are pushing sales of their completed properties - but in a slow market, it inevitably leads to discounted prices and near firesale scenarios.

This is reflected in increased auction activity. According to Essential Information Group’s Q1 and Q2 data, property auctions surged this year. There was a 45.1% increase in properties offered at auction in January 2024 compared to January 2023, and a staggering 98.3% rise in total revenue (across commercial and residential properties). David Sandeman, Director of EIG, attributes the surge to the escalating appetite for property auctions, with auctioneers choosing to add more dates into their calendars to cope with the influx.

Now is the time to look for development sites and run down properties that have come back to market, or uncover lucrative rental investments lurking in the clearance rack. Lookout for discounted prices, crunch the numbers and aim to secure a below-market-value property.

How Brickflow can help you beat the liquidity crunch

Whilst we can’t deny that a liquidity crunch is problematic for the property development industry, the right funding can help you work around the equity gap.

Finance can make or break a project; accessing specialist lenders, who typically have enough lending flexibility to offer higher LTV (Loan to Value) products, can be game-changing for any developer’s career. A 75% LTGDV (Loan to Gross Development Value) on the average £5 million development finance facility compared to a 60% LTGDV is an approximate difference of £750k in equity requirements.

Avoid inefficient equity deployment and search loans on Brickflow.

The deal doesn’t stop with the senior debt though - getting the whole capital stack right is crucial to maximise returns. That’s why Brickflow has teamed up with Deallocker - a specialist property finance marketplace for second charge and equity lending.

The partnership enables brokers and their borrowers to secure senior terms on Brickflow before heading to Deallocker to arrange second charge or equity requirements. Together, we’re helping developers get on site for less, accelerate project timelines and beat the liquidity crunch.

Rather than selling off assets, or accepting discounted sale prices, find better funding on Brickflow and then plug the equity gaps with Deallocker.

Developers who are itching to move onto the next project, but have equity tied up in a near-complete development, can also refinance on a development exit loan to avoid the firesale route. And crucially, shorten the development cycle.