The bridging loan market is continually growing and evolving, offering proven solutions for overcoming short-term funding gaps in all types of UK property transactions.

Property developers and investors are increasingly using bridging loans because they’re fast, flexible and can significantly improve access to market opportunities.

In this article, we’ll take a look at using bridging loans in property development and how using Brickflow can help you ensure you’ve got a winning deal before securing the best property development bridging loan on the market.

What is a property development bridging loan?

Bridging loans are short-term loans that can be used for various circumstances and property transactions, including property development.

They are secured against assets, either the property being funded by the loan, or additional collateral, most typically other property.

Bridging loan lenders assess and approve applications primarily on the basis of the exit strategy. In the case of a property development bridging loan, this would typically be:

- Selling the property after adding value through development/refurbishment

- Selling an existing asset

- Refinancing, possibly with development finance, a commercial mortgage, or a buy-to-let mortgage

Bridging loans usually have terms of up to 24 months, and lenders typically offer a degree of flexibility with repayment: an open-ended bridging loan allows the borrower to repay the loan at any point within the agreed maximum term. Likewise, early repayment is possible without incurring charges after a minimum term has passed.

When are bridging loans used by property developers?

There are many property deals where a developer might use a bridging loan, including opportunities to increase profits or capitalise on market opportunities.

Some typical examples of when a bridging loan might be used by a property developer:

- For speed: In a competitive market or for highly sought-after sites, quick access to funding could help you sway the seller in your favour and secure the deal. It can also help get a project off the ground sooner.

- For flexibility: Bridging finance can fund a wide range of property types and suit many borrowers, including those with poor credit history. Also, having an open-ended loan (more than one possible exit or a maximum term but no set date for repayment, and potentially more flexibility to extend) can relieve the pressure of a property sale.

- Leveraging opportunities: Development bridging loans enable developers to capitalise on unexpected lucrative opportunities, even before funding from sales proceeds is available. They also allow developers to undertake more projects simultaneously or to embark on larger, more profitable ventures.

There are also some property transactions that traditional financing can’t meet where a bridging loan can be used:

- Buying at auction: Auction purchases typically require a 10% deposit on the day and completion within 28 days – a timeline that other finance solutions can’t meet.

- Properties deemed ‘unmortgageable’: Traditional mortgage lenders won’t finance properties that are uninhabitable (no working kitchen or bathroom), of non-standard construction, or structurally unsound, whilst bridging finance can.

- Land without planning or only outline planning: A limited number of lenders offer land bridging loans, but securing planning permission on undeveloped land can be highly profitable. This allows you to either develop the site yourself or sell it at a higher value.

.jpg?width=494&height=494&name=shutterstock_716638129%20(1).jpg)

Are there specialist bridging loan types used in property development?

Some of the key types of bridging loan types used in property development include:

- Auction finance: Developers and investors often look for their next opportunity at auctions, and auction bridging finance offers a fast solution to complete the deals.

- Refurbishment finance: Can suit smaller-scale property development projects that can be completed in a shorter time frame. It is often used by investors looking to ‘flip’ a property or by landlords looking for a below-market-value property that can be refurbed to achieve a higher rental yield.

- Land bridging loan: This type of loan is used to buy land without planning, with only outline planning, or with planning that needs to be altered/ enhanced in some way.

- Fast bridging loans: Sometimes, you need to act fast to secure a property or site and expert bridging lenders can help ensure you get the funding needed, quickly.

- Large bridging loans: Lenders on the Brickflow platform can arrange bridging loans up to £100 million for larger development projects.

- Commercial bridging loans: These loans fund or refinance commercial properties, from education facilities to nightclubs or care homes to retail centres.

- Development exit bridging finance: When your development has reached practical completion, you can use a bridging loan to exit your existing senior debt ahead of sales proceeds, taking the pressure off the sale, as well as potentially enabling you to release capital.

Property development bridging loan process

Using bridging finance for property development works in the same way as any other bridging loan:

- Search the bridging market: Before committing to any property purchase, use Brickflow’s bridging loan calculator to model your deal and see if it stacks against actual loan options. It takes seconds, and can help you avoid unviable projects.

- Submit your project appraisal: Your application should comprehensively cover your project, from build costs, to your and your team's experience, and include thorough market research and comparables, to clearly demonstrate a viable project to lenders.

- Terms offered: Lenders will return with their initial Decision in Principle (DIP) for your project. At Brickflow, you can receive multiple DIPs within minutes of applying, allowing you to choose your preferred loan and progress to approval.

- Approval: The lender will conduct due diligence on you as a borrower, the property being purchased, and any additional securing assets being used.

- Loan drawdown: Funding typically takes around 14 days to be released, depending on the lender’s valuer completing their report and the solicitor’s property searches. Where lenders work with an AVM (automated valuation model) and accept title insurance, no searches are required, and completion can be in just a few days.

- Property development work: With funding in place, you can progress your project according to the scope of work set out in your application.

- Exiting the loan: After completing the property development work, the loan plus interest charges are repaid by selling the property or refinancing.

At Brickflow, we’ve streamlined the search and application process into a single digital journey, saving you hours of time applying to individual lenders, several of which might not be able to meet your requirements anyway.

Read our guide to find out more about bridging loan eligibility requirements.

Costs associated with a property development bridging loan

Below we take a look at common costs associated with property development bridging loans.

- Interest charges: The interest you pay will depend on various factors, including:

- The property, its value, its location, condition and desirability

- Your planned project

- The LTV or LTC (Loan to Value/ Cost) - a lower LTV or LTC can help secure lower interest rates (usually 40% deposit or more)

- Your loan term

- Your exit strategy

- You as a borrower, including your credit file, asset net worth and experience in investing in similar properties.

Interest is typically calculated daily, so you only pay interest on the duration of your loan, even if you exit the loan early or midway through a month (some lenders charge monthly, meaning you pay a full month’s interest regardless of when you exit). Most lenders offer rolled-up interest (paid at the end of the loan), so there are no monthly payments involved.

Your final redemption payment (to pay off the loan) will include the original amount of capital borrowed plus accrued interest.

- Valuation or survey fees: Lenders will arrange for a surveyor to assess the property, with costs depending on the property value, type and location. Lenders should provide quotes from more than one firm and let you choose your preferred option. Your intermediary should be able to help you with this.

- Legal fees: The lender’s legal fees, as well as your own.

- Broker fees: Normally the broker's fees are paid by the lender.

- Arrangement fees: Up to 2% of the gross loan.

- Exit fees: Not that common for bridging finance. Almost none of the lenders on the Brickflow platform charge exit fees, but they instead might stipulate a minimum loan term – between 1 & 6 months normally.

Are there any alternative loan options for property development?

Yes, whilst bridging finance can suit a variety of property development projects, depending on the circumstances, there are other finance options that might be more appropriate.

Development Finance

Specifically designed for large-scale property development projects, including ground-up construction of commercial or residential properties, property conversion and heavy refurbishment work. It is bespoke and tailored specifically to each project, with funding released in stages to align with the build schedule.

You can potentially borrow more with a development finance loan compared to a bridging loan, however, the application process is more complex and timeframes for loan completion are longer.

If you think development finance might be more appropriate, run your project numbers through Brickflow’s development finance comparison, the only tool on the market to search & compare live development finance loans. It’s the quickest, most accurate way to make sure your deal stacks against actual finance costs and carry out comprehensive due diligence on your project before committing to a site.

Commercial Mortgages

A long-term solution for purchasing commercial properties. They can be arranged on a capital & interest repayment basis or interest only. Where a commercial property has built up equity, you can refinance onto a new commercial mortgage and release some of the capital for development work.

You can instantly compare commercial mortgages on Brickflow.

Joint Ventures

Joint ventures typically involve an investor providing the funding for a developer’s project in return for a profit share – usually 50%. It can work when your capital is tied up, but you don’t want to miss out on an opportunity that has arisen.

Second charge loans

Second-charge loans – including mezzanine finance, investor, or equity finance – are typically arranged in addition to senior debt (development finance) and can provide further working capital for property development.

If you are unsure as to what type of finance is right for your project, speak to a specialist finance intermediary. We are happy to connect you with any of our broker partners who are amongst the best in the UK and can help you secure the best loan for your circumstances.

Find out more about development finance brokers and bridging finance brokers.

Using Brickflow to find the best bridging loan for property development

Before committing to a property development project, you need to know how much you can borrow and how much it will cost.

It’s easy to underestimate your finance costs, overestimate your profit, and consequently overpay for the property, which can be the difference between a failed or successful project.

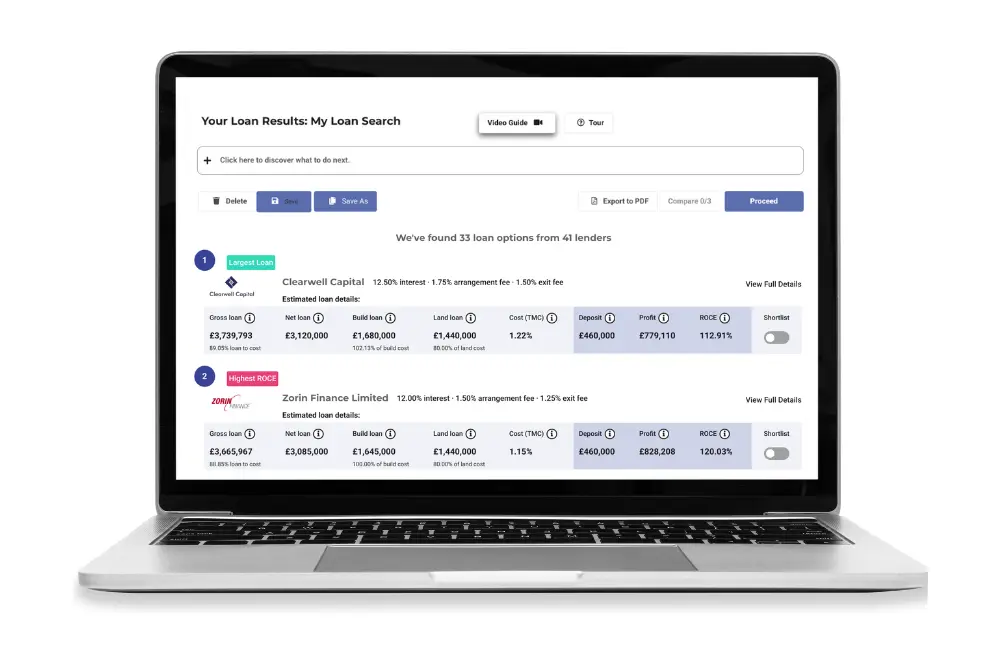

Running your project numbers though Brickflow's live bridging loan comparison tool is the easiest, most accurate way to check your deal stacks and secure the best bridging loan for property development. With instant loan results, you can adjust and play around with your figures if needed or save your project and come back to it later, before applying directly from the platform.

Here's how it works:

1. ENTER your project criteria and model your deals

- It takes seconds to enter your property details and search loans from banks, challenger banks, non-banks and specialist bridging lenders

- Find out exactly how much you can borrow on your project and how much it will cost

2. COMPARE loans from 50+ bridging lenders

- Compare LTVs, rates, fees, deposit input and more

- Filter and sort your results, and shortlist your preferred loans

- Save your search and log back in later

3. APPLY for a loan with your intermediary

- Get multiple same-day DIPs back

- Apply using Brickflow’s digital Smart Appraisal™, the only tool that directly connects with lenders

- Our lender-favoured application covers everything lenders need to know to make quick, reliable credit decisions - but if one lender says no, simply send the same application to another lender, and avoid repetitive form-filling.

Try our bridging comparison tool today to find the best bridging loan for property development.

Secure your property development bridging loan today

Using bridging finance for property development can create opportunities, help you maximise profit and ultimately scale your business sooner.

There are many fast and flexible bridging loans for property development. With the right due diligence to ensure your project is viable, you can find the right type of bridging finance. Run your project numbers through Brickflow’s bridging comparison tool today to find out what you could borrow and compare loans available for your project.

FAQs

Do I need to provide security against my property development bridging loan?

Yes, all bridging loans are secured. Typically the security is the property you’re purchasing with the bridging loan, but it can be secured against other property and assets.

You are at risk of losing any assets used as security if you can’t repay the loan.

Is it possible to get a 100% property development bridging loan?

Some lenders in some circumstances might accept additional security instead of a cash deposit, but this is assessed on a case by case basis.

You can also potentially secure 100% bridging finance in a joint venture with an investor, in return for a profit share - typically 50%.

Can I use a property development bridging loan to refurbish my house?

Yes, it’s possible to secure a bridging loan for renovations in your own home, but you would have to demonstrate a viable exit strategy to the loan. For example, even after extensive renovations, properties have a limited value, so the amount you borrow would have to be proportional to how much you can refinance your house for in order to exit the loan.

When a bridging loan is used for the borrower's own home, it is regulated by the FCA (Financial Conduct Authority) and subject to the same regulatory criteria as a conventional mortgage. Therefore, completion times are much longer than unregulated bridging loans.

Does a project need to cost a certain amount to qualify for a property development bridging loan?

Lenders on the Brickflow platform offer bridging loans from as little as £25,000.

However, they are far more likely to engage with borrowers looking for £150,000 plus. This is simply because for the same time and resource, they would earn, in this example, 6 times more.