Borrower Tips

Biodiversity Net Gain - Navigating the New Legislation

What is biodiversity net gain, how do you calculate it, is it mandatory and how do you achieve 10% BNG?

Industry Insights

Industry Insights

Are we out of the woods yet? Well, not really – recession, living costs and mortgage prices continue to hold back the property market. But relaxation of PDR rules has come just at the right time to capitalise on the soaring HMO and BTR sectors.

Just as we relaxed a little over the state of the UK economy, turning our heating up a notch, and splurging on non-supermarket-basics items, a recession walks in.

The ONS confirmed a 0.3% decrease in GDP (gross domestic product) for the three months to December 2023 – meaning a technical recession, after a second quarter of decline (-0.1% in Q3 23). A significant fall in retail sales leading up to Christmas and a drop in all main economic sectors are behind the recession.

For some perspective, between Q1 of 2008 and Q2 of 2009, GDP shrank by 6%.

The UK avoided recession in the first half of 2023, but succumbed to the combined effect of weak growth in European markets and low productivity. The fall in GDP will increase pressure to cut interest rates sooner.

In an ironic twist, rising real wages will likely be the recession-busting hero, despite being positioned against the BoE last year and supposedly responsible for keeping inflation high. In 2024 the surging real wages (expected to rise by 2.6% this year) has boosted the economy and may have already dragged Britain out of recession.

With an election looming the government is under pressure to demonstrate how it will deliver it’s promised economic growth. The 6th March budget is likely to be the last major fiscal event before the general election, and speculation around what chancellor Jeremy Hunt will deliver points to income tax and NI cuts, fuel duty cuts, abolishing inheritance tax, child benefit reform and help for first-time-buyers.

According to Rightmove, market momentum is building, with average house prices up 0.9% in February compared to last month and an annual increase of 0.1%. This comes after consecutive annual decreases in every month since August 2023. The average asking price across the UK is now £362,839.

This increase has been driven by more sellers and buyers coming to market, with listings increasing by 7% and buyer enquiries up by the same. Zoopla is reporting a 12% increase in buyer demand and similar price increases, as do other key HPIs.

So things are on the up, but (there’s always a but)…the wider market still faces challenges. December’s surprise rise in inflation to 4% hung on into January, recession jitters and the ongoing Red Sea conflict putting pressure on goods supply and oil prices, could stall further rate cuts.

Market predictions are varied – Savills predicts a drop of 3% in 2024 whilst Knight Frank expects houses prices to rise by 3% (rather than their previous predictions of a 4% fall). Meanwhile, Taylor Wimpey, recorded a whopping 49% drop in annual profit last year.

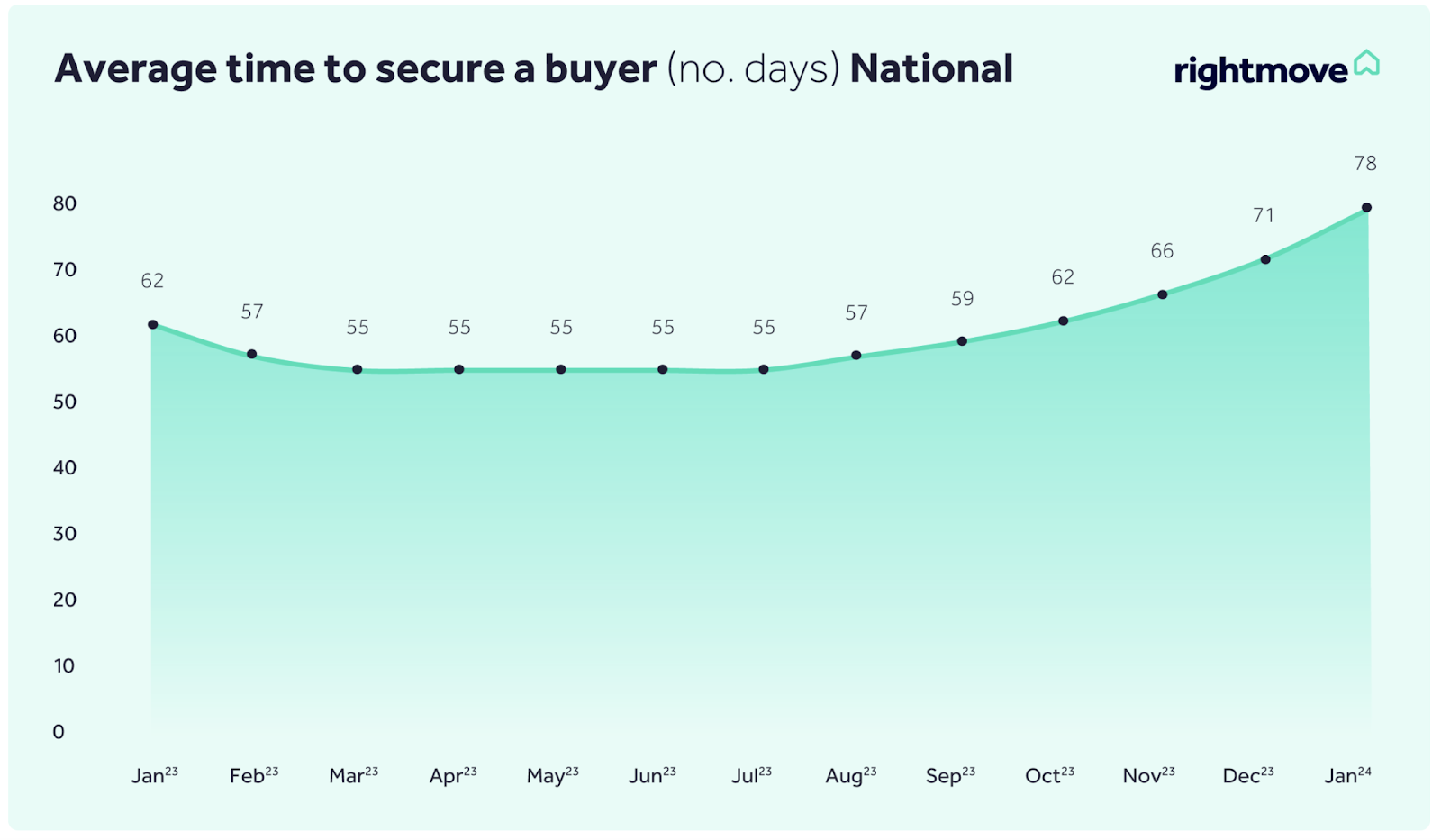

There is still some buyer sensitivity around pricing. Mortgage rates are lower, with the average for a two-year fix now 5.57% compared to the 6.86% peak in July 2023. But they are still at a level that takes some getting used to – this combined with higher living costs and the expectation that interest rates will drop soon, buyers are being cautious. Average selling times have increased, and buyers have more choice now with more properties on the market, so the ones that are priced right will sell fastest.

New plans are afoot to boost housing developments in England, with Michael Gove (Secretary of State for Levelling Up, Housing and Communities) announcing a string of new measures on February 13th. The consultation period will end on 26th March.

The proposals include:

Gove is also said to be lobbying the chancellor ahead of the spring budget for cuts in stamp duty, an extension of the mortgage guarantee scheme to cover first-time buyers with a 1% deposit and a ‘foreign ownership levy’ on international investors who buy residential property here. (insidehousing.co.uk)

Let’s take a look at Gove’s plans.

The government’s Affordable Homes Guarantee Scheme provides longer-term, lower-cost, fixed rate loans to housing providers registered to build affordable housing, enabling them to deliver more affordable homes or facilitate investment in existing affordable housing.

As of the 12th February, an extra £3bn in funding has been allocated, which the government believes will result in 20,000 new affordable homes being built. The scheme is for £6 billion in total, with a deadline to apply by April 2026.

An investment management company, ARA Venn, is acting as the delivery partner to manage the AHGS, originating, underwriting and managing the portfolio of loans to registered providers in England. The capital to fund them is raised by a Government guaranteed bond programme established and managed by ARA Venn.

The loans can have terms up to 30 years and for the first time, the scheme can also be used to upgrade existing properties, including the removal of dangerous cladding.

Backed by the Department for Levelling Up, Housing and Communities (DLUHC), the first loans were given out in November 2021, varying in size from £28m - £55m. In December last year, four housing associations received a split of £256.5m to fund the development of around 1,500 new affordable homes across the North East, the East Midlands and the East of England. A similar amount was shared between three developers to deliver 1,500 homes in Cornwall homes in March last year.

The government also announced on 13th February that every council in England ‘will need to prioritise brownfield developments [and] be less bureaucratic and more flexible in applying policies that halt housebuilding on brownfield land’ (gov.co.uk). If housebuilding drops below expected levels (locally agreed targets) in England’s 20 largest cities, the councils will have to adopt a ‘brownfield presumption’ making it easier to achieve planning permission for brownfield sites and harder for councils to reject plans.

There’s no argument against developing brownfield sites – it is in fact key to help meet housing demand in urban areas where infrastructure is already in place, but it is not a new idea. We discuss the issue in our white paper Solving the UK’s Housing Shortage, pointing out that the costs and risk of remediation of brownfield sites often makes the sites unviable, and can act as a deterrent, for many developers.

To really drive brownfield development, the government needs to support the remediation and decontamination of disused sites, or offer accurate information from detailed land assessments to allow developers to calculate viability.

The relaxing of Permitted Development rules, with effect from 5th March this year, will unlock plenty of development opportunities.

Permitted development rights (PDRs) allow individuals and developers to make certain changes to buildings or land without the need to apply for, and obtain, planning permission from the LPA.

Use Class E (commercial, business and shops)

From next month, converting all types of building in Use Class E such as offices, gyms, doctor’s surgeries, shops etc. will be easier. Currently, all buildings have to be proven to have been empty for three months prior to submitting a PDR application – the new rules scrap this waiting period. This is great news for anyone who wants to buy a tenanted commercial space because it can now generate an income up until the day development begins.

Class MA (Mercantile to Abode / from Use Class E to residential)

Also set to change is the upper limit on how much square footage you can convert to residential use on Class MA. Currently it’s 1,500 square metres, which equates to about 25-30 flats; on a large office block with multiple floors, it’s pretty restrictive, and the rest of the building has to be developed with full planning. From the 5th of March, this limit will be removed, making larger offices spaces much more viable.

Article 4

Local Planning Authorities (LPA) can restrict certain PDRs in part of its local area using an ‘article 4 direction’ (so planning permission is required to carry out development that would otherwise be covered by PDRs). Some LPAs have blanket exclusions on PDR over their entire precinct. Gove has now altered this to be only in the smallest geographical area possible and on a case by case basis.

Further proposed changes to PDR

Demand for HMO’s (House in Multiple Occupation) is dramatically increasing (more on that below) and the proposed changes to PDR will make it significantly easy to deliver more.

The proposal includes:

If passed, these changes mean freehold properties with good connectivity will be ripe for HMO conversion.

The consultation process is open until the 9th of April, and you can have your say on the government’s online survey.

It’s been well discussed that the private rental sector (PRS) is being slowly eroded and rental stock supply is dwindling. Various factors are causing the sector to be less appealing for property investors:

A house in multiple occupation is a house with up to six rooms with at least 3 tenants living there that form more than 1 household and there are shared facilities such as kitchen or bathroom. A large HMO is when there are at least 5 tenants in the house.

As mentioned, demand for HMOs is exploding, with the most sought being those with decent sized rooms and en-suites. Like most property trends, the reason for the increase in demand is multi-faceted:

More and more PRS landlords are converting their properties to HMOs, not just to meet rising demand, but because the increased interest rates mean they have to work their properties harder to cover their costs.

A permitted development of a single property into a house with multiple rooms, generating multiple rental incomes to cover costs and mortgage payments can be a lucrative and straightforward project.

Investors might have temporarily lost confidence in the BTL market when buying existing stock, but the appeal of property as an asset is still high and the imbalance between supply and demand for rental properties is driving developers to BTR.

Developers can become landlords at lower entry costs; both the lower costs of building a property versus buying existing stock, as well as avoiding having to pay the additional 3% SDLT surcharge.

BTR properties, developed specifically for renters, can be part of large-scale developments that offer tenants various lifestyle benefits, from on-site gyms, meeting-rooms, cinema spaces, outdoor spaces, concierge and they facilitate community interaction. However, BTR can be delivered on any size scheme. By offering benefits such as built-in WiFi and utility costs, as well as the green credentials that are synonymous with such schemes; living walls, low carbon, bike storage and car club membership, it is both attractive to tenants and allows investors to charge a premium.

If you’re considering a BTR scheme as a developer, here’s what you need to know:

The BTR sector is growing year-on-year and rapidly becoming a key part of the UK property market, across all regions. Developers and investors with good urban sites can capitalise on the opportunity to meet the growing demand and benefit from long-term capital growth and reliable income returns.

Whether ground up development or converting existing properties into HMOs or BTRs, they are typically funded with a bridging loan or development finance.

A bridging loan would be most suited to:

Lenders across the Brickflow platform offer bridging loans from £25,000 - £60 million. It takes less than 2 minutes to compare live bridging loan options.

Development finance would be most suited to:

Development finance loans range from £26,000 - £300 million on the platform and are structured to suit the project, covering each stage of the development separately, from purchase through to the construction phase.

Lenders now have more room to be competitive, and we’re seeing rates coming down from more and more lenders.

We also have lenders now offering Brickflow exclusive rates, where one lender reduced their rate from 1.15% to 0.99% per month on a 70% LTV bridging loan product on residential asset types, just for Brickflow users.

Data from the Brickflow platform reveals that in January 2024 we have already seen nearly 50% of the total number of searches we had throughout all of 2023.

Of course, these stats show platform growth but it also clearly signifies that borrowers are becoming more and more aware that better CRE finance deals are out there, and naturally, when margins are tighter, they want to find them.

If you or your clients want to capitalise on the booming BTR or HMO markets right now, then search for finance on Brickflow. It takes just 2 minutes and you’ll be able to compare live loan results from the breadth of the market.

If you're a broker, you can find out more about Brickflow on the broker homepage.

For borrowers, you can find out more here.

What is biodiversity net gain, how do you calculate it, is it mandatory and how do you achieve 10% BNG?

The inside track on property development in April 2023.

The inside track on property development in July 2023.