Industry Insights

Industry Insights (March 2023)

The inside track on property development in March 2023.

Industry Insights

Industry Insights

2023 ended on a high, and forecasts for the new year ahead indicate more stability, reduced borrowing costs and a handle on inflation. Will it all be plain sailing though, as markets navigate another devastating war, major global elections and the risk of recession not quite quashed?

We’re looking ahead to see what the economic forecast for 2024 means for property investors.

Starting with inflation

As people sat down to their turkey dinners and trifles, 2023 ended with fairly upbeat economic news for the UK - CPI inflation dropped to 3.9% with core inflation (excluding energy, food, alcohol and tobacco prices) dipping from 5.7% to 5.1%.

December's figures, released today (17th January), show an unexpected increase to 4%, with the increased cost of tobacco said to be the main cause.

Whilst it might be short of the 2% target the Bank of England had set for the end of the year, it was a significant improvement from the 11.1% peak the previous year and better than Rishi Sunak’s 5.35% target.

Food prices

Supermarket inflation fell at its fastest monthly rate on record, with prices being just 6.7% higher in the four weeks to Christmas Eve than a year earlier, the lowest since April 2022. Good news indeed, but with food prices still 27% higher than in November 2021 and energy prices 66% higher, household budgets are still under pressure.

Services

Further dis-inflation is being somewhat hampered by service companies not easing their price hikes (sticking to the story that staff wages rather than bigger profit margins are what’s causing their increased prices), meaning core inflation only dropped by 0.6%. Whether or not service companies continue to pass on higher costs to consumers during 2024 is a key concern for the BoE and possibly the main reason why it may decide to keep the base rate higher for longer.

A disconnect between markets and rate-setters

Central bankers are hesitant to promise early rate cuts, fearing consumers will relax their spending habits, which will increase demand and re-ignite rising inflation. Meanwhile, traders have a different perspective, and expect central banks to reduce interest rates sooner than indicated to avoid risking a recession by keeping rates high, pricing in the first drop from as early as March (The Guardian).

Goldman Sachs are predicting earlier and more aggressive rate cuts, with 225 basis points of consecutive cuts, bringing the Bank Rate to three per cent by mid-2025 (City A.M).

The Israel-Palestine conflict

Complicating the intricate balancing act, and adding fresh pressure to prices, is the on-going attacks in the Red Sea shipping artery by Houthi rebels (protesting against Israel’s war on Hamas in Gaza). The strait is one of the key arteries in the global trade network en route to the Suez Canal, with around 12% of all global trade passing through the Red Sea. The disruption is likely to increase prices of rice, tea, coffee, meat and seafood by 5 – 10% over the next few weeks.

The latest attack on a shipping container caused oil prices to fluctuate during the first week of 2024 and lead to a number of businesses suspending shipments through the Red Sea and opting for the longer trip around the southern tip of Africa. The redirection is expected to cost up to $1 million extra in fuel for every round trip between Asia and northern Europe (driving shares in shipping companies up, amid expectations of higher freight rates).

Keeping inflation under control might not be as smooth as anticipated in 2024, but most economists are anticipating between 2 and 4 reductions to the base rate.

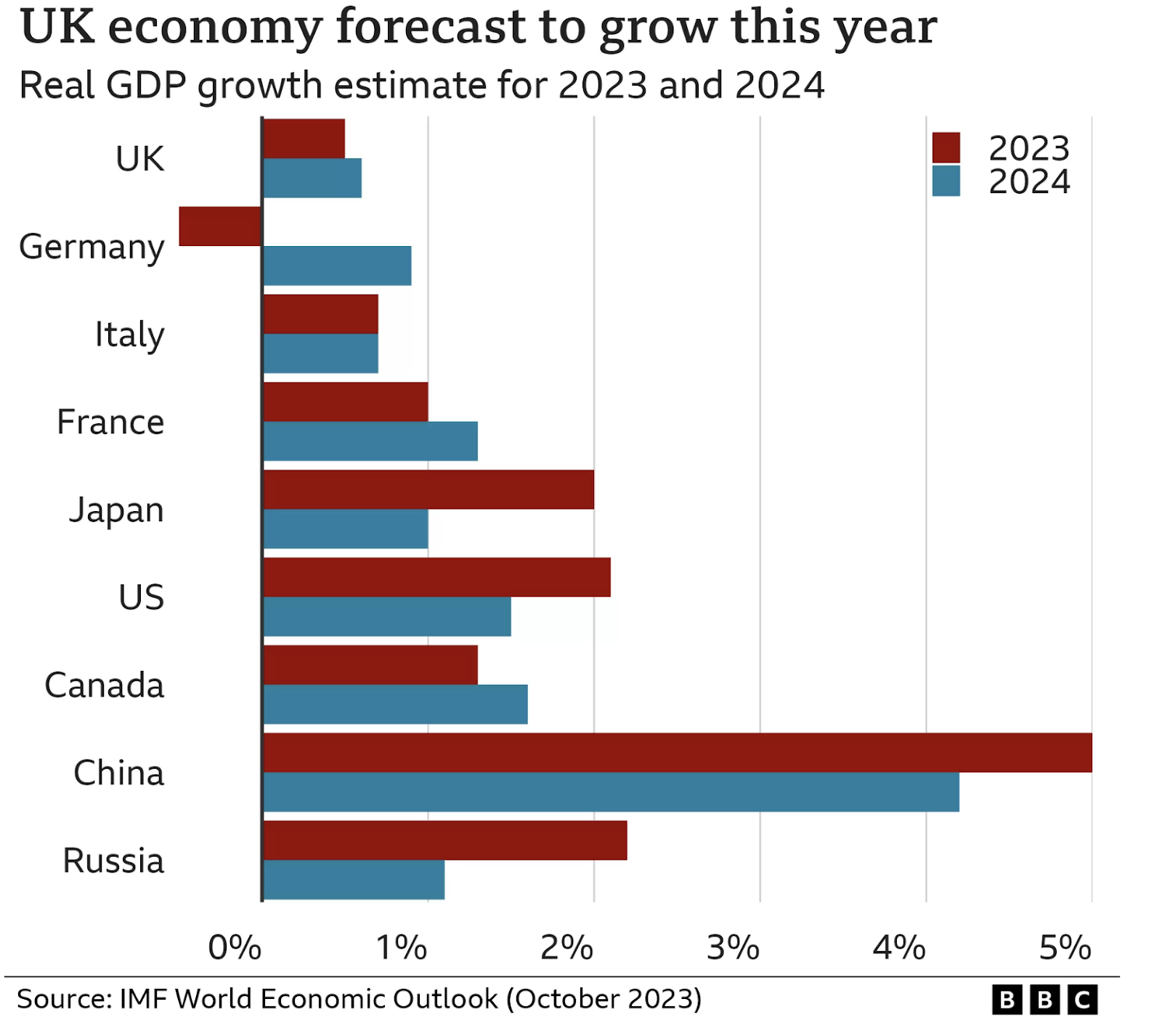

Is GDP looking hopeful?

Yes, actually, even if it’s a bit lacklustre.

‘The global economy has outperformed even our optimistic expectations in 2023.’ (Goldman Sachs)

Whether or not the UK avoided recession won’t be clear until Oct – Dec figures are released in February, but according to the Office for Budget Responsibility (OBR), the economy has shown stubborn resilience to the pandemic and energy crisis shocks.

In their latest Economic and fiscal outlook (Nov. 2023), the OBR said that it expected the UK economy to grow by 0.7% in 2024, despite the negative growth in Q3 23. It did however cut growth forecasts for the next three years:

In October, the International Monetary Fund (IMF) predicted that the UK would grow by 0.6%, which would make it the slowest growing developed country in 2024.

The Bank of England meanwhile is more pessimistic, stating that UK economic growth will flat-line in 2024, with a 50-50 chance of recession:

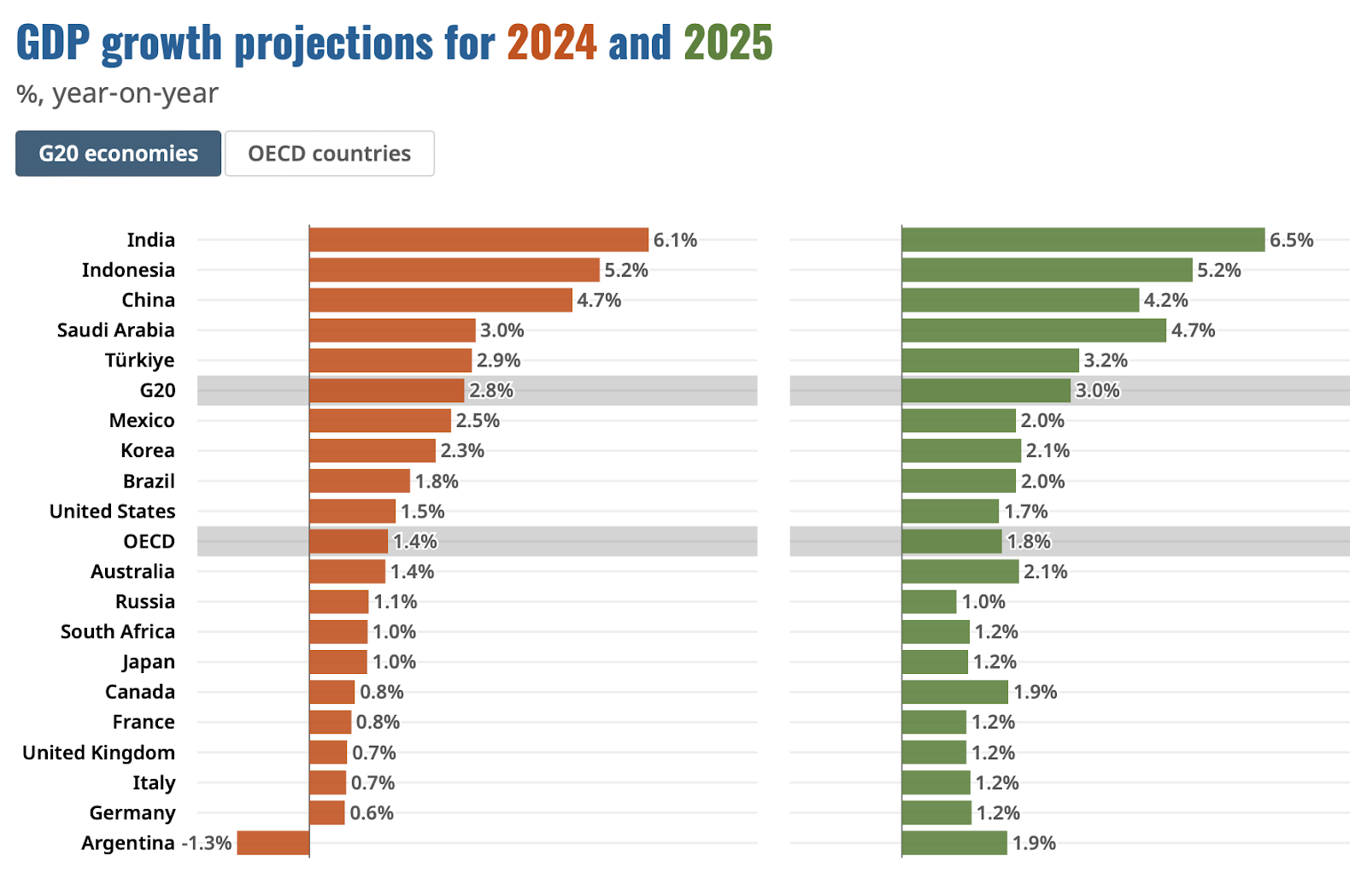

Modest growth isn’t solely a UK problem though – the impact of monetary tightening policy, weak trade and lower business and consumer confidence is stunting growth globally according to the OECD’s latest Economic Outlook.

They project global GDP growth of 2.7% in 2024 and a slight improvement to 3.0% in 2025, with Asia expected to continue to account for the bulk of global growth in 2024-25, as it did in 2023.

The IMF forecast slightly higher global growth, at 2.9% in 2024, whilst less upbeat Deutsche Bank’s analysts are suggesting a decline from 3.2% in 2023 to 2.4% next year, with 2.5% seen as the upper bound of being deemed to be in a global recession. It’s dependent on major contributions from the biggest emerging markets (EMs), with India forecast to grow by 6.0% and China by 4.7%.

The historical average for global economic growth is 3.8% for the years 2000 to 2019.

For the Eurozone, Deutsche Bank forecast a meagre 0.2% growth in GDP, with recovery beginning in mid-2024, when the European Central Bank (ECB) is likely to cut 100bps from June to the year-end.

'Silver linings' for the UK economy

Whilst GDP looks pretty stagnant, Deutsche bank has indicated reasons to be optimistic over the UK economy:

Tech and AI prop up the market

With AI’s ever expanding capabilities, the potential boost to productivity could bolster global markets, with analysts believing that it could increase US productivity well above 3% by the end of the decade. The full scale of the tech effect is unlikely to be revealed in 2024, but it’s widely acknowledged that the ‘Magnificent Seven’ (high-performing and influential companies in the U.S. stock market: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Teslatech) helped to prop up equity markets in 2023 and ease financial conditions (flow.db.com).

To the polling booths...

2024 will be a year of significant elections, with about 40% of the global population heading to the polls, including in the UK, the US, Taiwan, Russia, Ukraine and India, to name but a few.

As mentioned above, the March 6th budget offering could potentially be the Tory party’s last chance to woo voters, pushing tax cuts high up on the chancellor’s agenda. Sunak is widely expected to call a general election in the autumn, but with Labour’s near-20-point lead in the polls, he will potentially hold off until January 2025, the latest possible date that a vote must be held. Early polls indicate Labour will win a majority.

A change of government should have relatively little impact on the housing market. The current guise of Labour is a lot more moderate and their rhetoric around building houses bodes well – though as we discussed in previous Industry Insights, clearly defined plans about how they will boost building it haven’t been evidenced.

A change of government should have relatively little impact on the housing market. The current guise of Labour is a lot more moderate and their rhetoric around building houses bodes well – though as we discussed in previous Industry Insights, clearly defined plans about how they will boost building it haven’t been evidenced.

The biggest story in the financial markets though will take place across the pond, in what is set to be another polarised and fraught US election campaign between Biden and Trump.

There is concern that if Trump wins, he’ll follow a similar isolationist strategy to the one he pursued during his previous term, significantly raising import taxes, which could plunge the global economy into recession.

So what about the housing market?.

The 2023 market was more resilient than many predicted as it continued its transition from frenzy to more normality. Rightmove reflects average asking prices in Dec 23 as just 1.1% below those from 1 year ago, with prices in 11 regions higher than a year ago; Halifax’s HPI shows three months consecutive rises to average prices, with a 1.7% increase on an annual basis. Nonetheless, sales agreed were 13% lower than the same period in the more frenetic 2022.

Zoopla analysis also indicates that the housing market has adjusted to higher borrowing costs through lower sales rather than dramatic price drops. The ultra-cheap borrowing that was introduced to support economies after the 2008 crash and through Covid, are unlikely to return, and though mortgage rates seem high in comparison to recent years, by historic standards, rates between 4 - 5% are low. If mortgage rates stay around this range, house prices are likely to see low, single digit growth for the next 1-2 years. Which means, for the first time in years, house prices affordability will improve, increasing consumer confidence.

Rightmove predicts that new seller asking prices will drop nationally by an average of 1% in 2024, with motivated sellers still needing to price below their local competition to secure a sale. More stable market conditions are likely to see more family movers return to market, who had put their plans on hold with last year’s uncertainty: buyer demand in the mid-market, second-stepper sector has increased the most. And the so-called ‘Boxing Day Bounce’ saw a record number of home-sellers coming to market, with more than 10,000 new properties – the biggest number of new sellers in one day since 2011.

There will still be swathes of mortgaged households reluctant to move and give up their lower rates though. This combined with labour shortages, higher construction costs and painful planning delays mean there’s a persistent shortage of stock on the market – in fact, an estimated shortage of 4.75 million homes, as we highlighted in our white paper Solving the UK’s Housing Shortage.

Construction

Things are looking up in the construction industry, as S&P’s Global UK Construction Purchasing Managers' Index™ (PMI®) show that the downturn has started to ease: despite December’s data showing another drop in construction activity, it was the slowest decline since September, when it began declining. According to the PMI report, 41% of construction firms predict a rise in business activity over the course of 2024, while only 17% forecast a decline.

What’s faring well?

Depressed transaction volumes will keep prices subdued, but the closer we get to rate cuts the more we'll see activity increase, and expect the market to be growing again by Q3 and Q4. Any price spikes will likely happen in 2025, when wage growth and the massive undersupply of housing will affect the market - developers and investors buying this year and delivering next year are set to profit (read September’s Industry Insights for more detail).

Prime residential

Knight Frank’s research forecast a positive year for the prime residential markets, both in the UK and overseas. Their overall prime price forecast for 2024 has grown from a 2.1% to 2.5% increase in pricing since mid-2023 assessments. Early projections for 2023 had indicated a 1.7% average price increase, but by December the figure had actually surged to 2.4%.

Like the wider property market, it’s being bolstered by increased buyer confidence, receding inflation, the last of the interest rate hikes and international buyers still benefiting from comparatively weak sterling.

Stronger market in Scotland

End of year data shows the annual average price of a property in Scotland rose by 1.9% in November, with an average sale time of 33 days. In contrast, in the south east of England, it takes an average of 67 days to sell.

If you’re bringing a property to market…

The best strategy to sell in the current market is to price temptingly at the outset, rather than marketing with a higher price and a dose of hope. This will hopefully avoid reducing the asking price later and capture the early-bird buyers for 2024.

And the land market?

Data published by Statista Research Department last month indicates that, although land prices in the UK are forecast to continue to grow between now and 2026, the rate of that growth is expected to slow down:

Forecasted % change of development land value in the UK from 2022 to 2026:

Much of the residential market hinges on mortgages – what’s the latest?

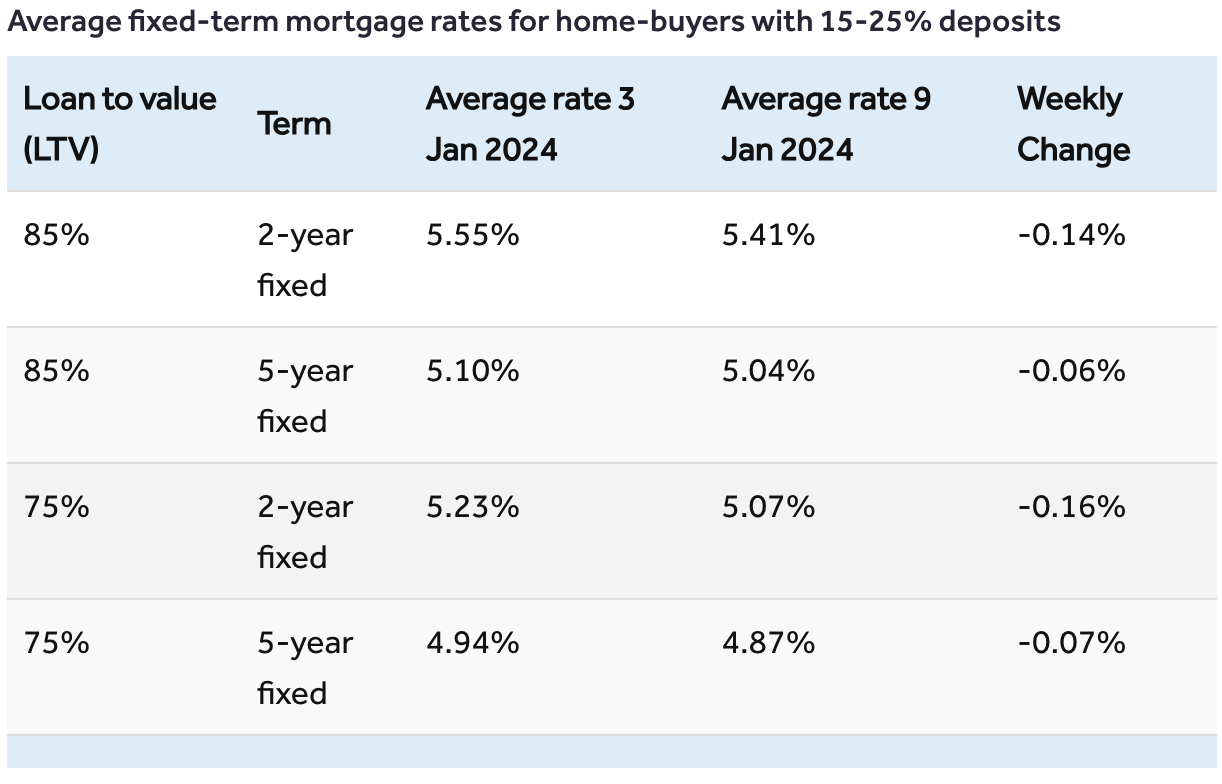

Happily, the new year kicked off with lenders slashing mortgage rates.

As people trickled back into the office, the working week began with Leeds Building Society and the UK’s largest mortgage lender, Halifax, cutting fixed mortgage rates by nearly 1 percentage point. Swiftly followed by HSBC, which is now offering a five-year deal at 3.94%. Several other lenders cut their rates just before Christmas, with Barclays reducing its deals up to 0.43 percentage points. Average mortgage rates have been falling continuously since July, and for the first time in six months, dipped below 6% in December (Sky News).

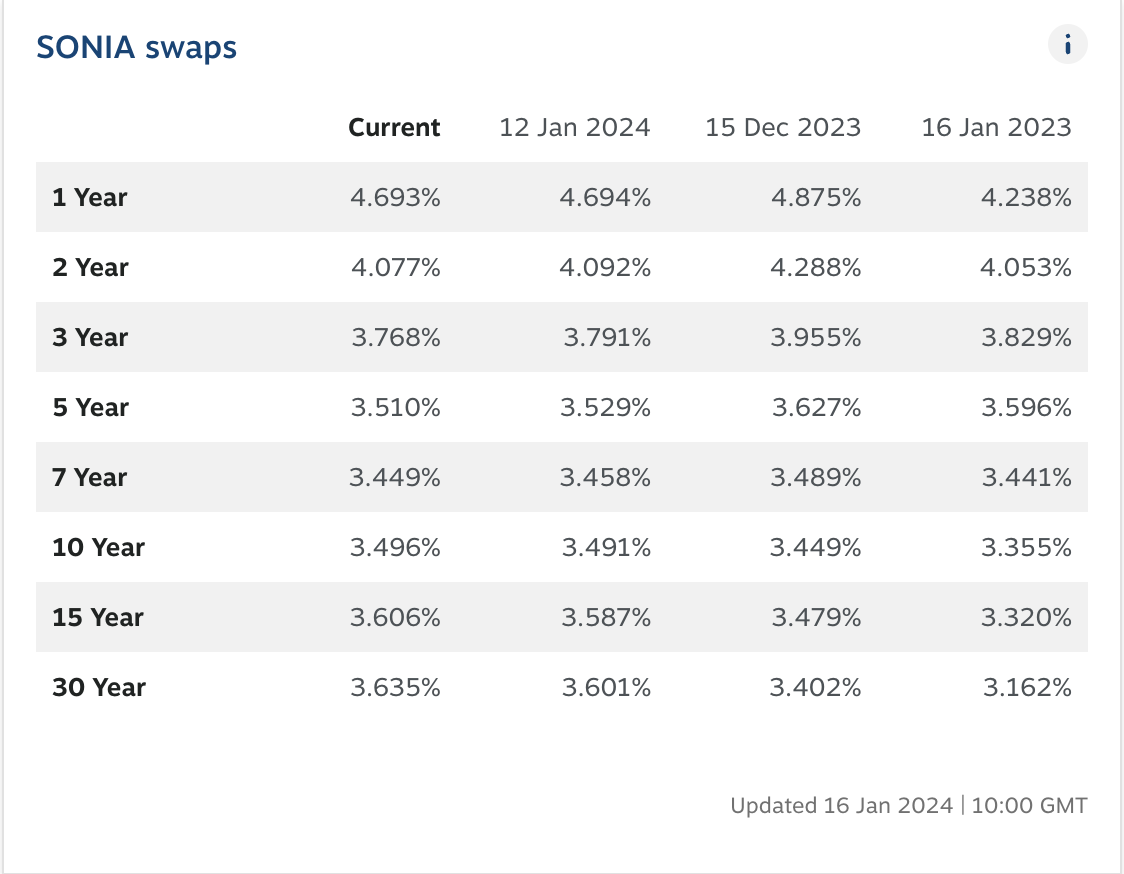

Lower swap rates have begun filtering through to mortgages, and January’s SONIA swaps show there is still room for lenders to reduce rates further. It’s highly likely that more banks and building societies will follow suit and improve their rates, fighting it out over the coming weeks to offer the cheapest rates.

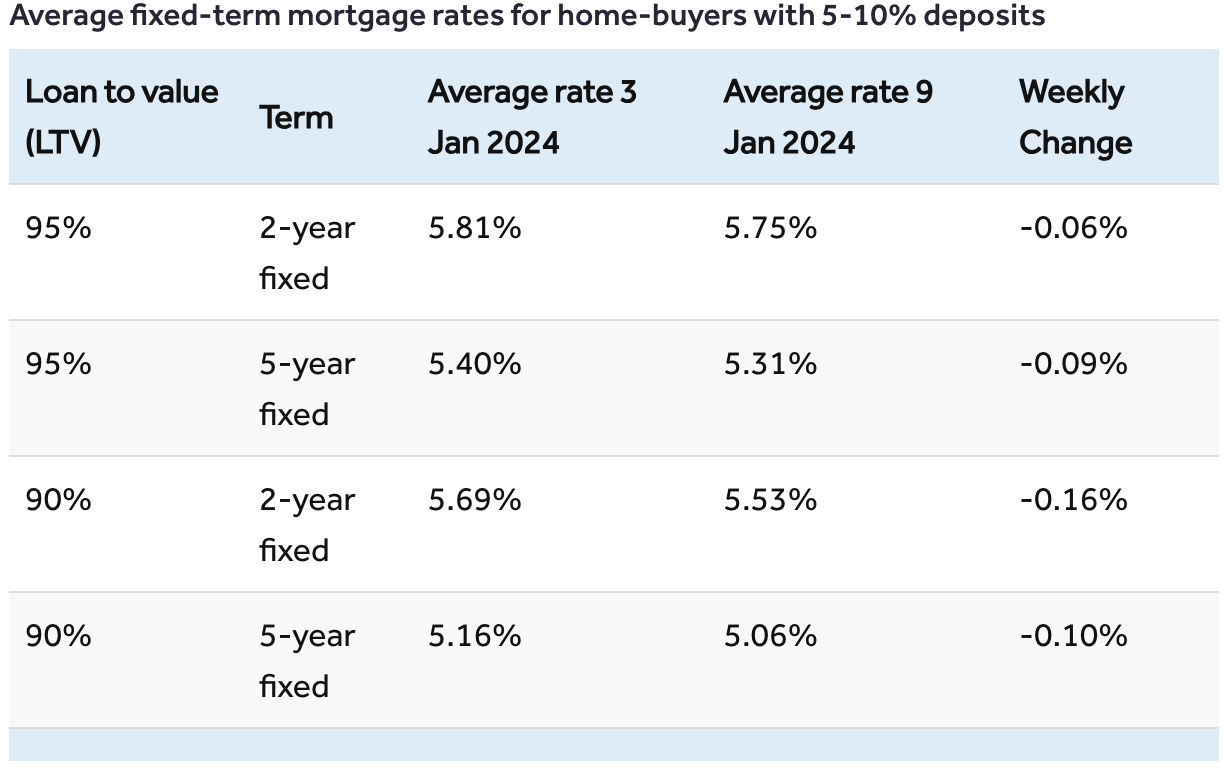

Average mortgage rates on Wednesday 9 January 2024:

Source: Rightmove

Whilst the rates are still high in comparison to the historic lows we had gotten used to, the mortgage market is much calmer and buyers can now better plan for what they can afford. Overall affordability will continue to be an issue for home-movers though, especially as banks are stress-testing new borrowers at rates of 8-9% as standard.

But it’s certainly a great start to the new year.

What all of this means for the CRE finance industry

Volatility creates opportunity. Whilst rates shouldn't rise further, the impact of the rapid rate rise has yet to be fully felt. Investors carrying too much debt, or those caught out by planning delays, will be forced to sell in suboptimal conditions, meaning there’ll be bargains to be had – and many of these will likely be found at auction.

Brokers that can get that message across to their developers and that have the lending contacts to exploit those opportunities will win big in 2024.

Residential, Commercial, Bridging

Whilst finance will remain steady for residential developments due to the chronic undersupply of new homes, we think the bridging sector is set to be very busy in 2024, as people need to move fast to secure any discounted opportunities.

Commercial won’t be as strong, but the majority of landlords haven’t refinanced since covid, so there will be an increased uptick in refinancing BTLs and portfolio mortgages.

The inside track on property development in March 2023.

The inside track on property development in February 2023.

The inside track on property development in September 2023.