Industry Insights

Industry Insights (January 2023)

The inside track on property development in January 2023.

Industry Insights

Industry Insights

Welcome to February’s Industry Insights, the inside track on property development. Read our views on the current economic climate, house price correction, adapting to the new market and why 2023 will hold plenty of opportunities.

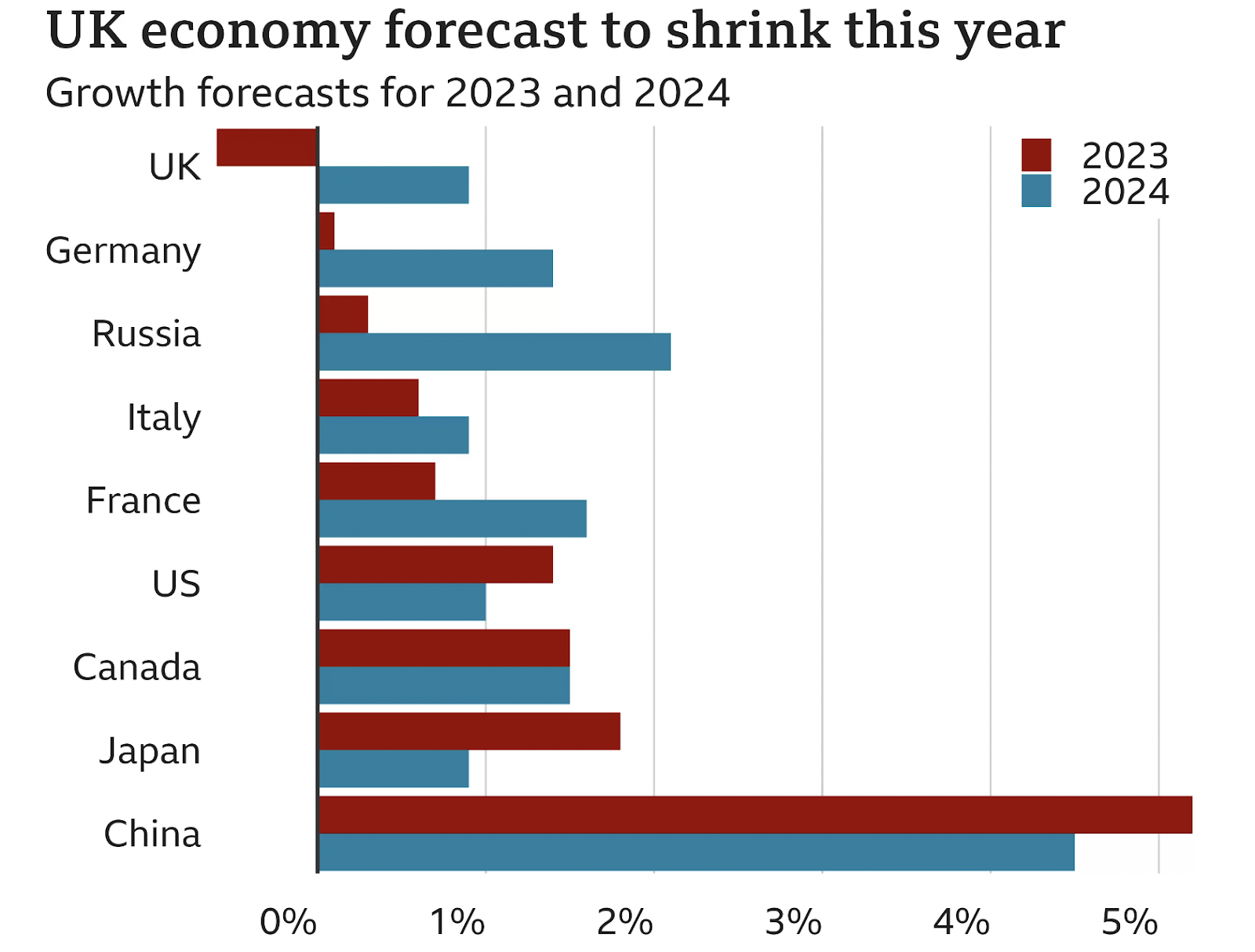

Talk of a UK recession has been looming like a raincloud over a picnic for months now. Albeit, a picnic that’s already been looted by a cost of living crisis, forty-year-high inflation and soaring interest rates. After what was thought to be two consecutive quarters of economic shrinkage, the rain cloud burst and in the first few days of February, Bank of England Governor, Andrew Bailey, announced that the UK was in recession.

However, revised figures from Q3 and Q4 of 2022 actually show a flatlining of gross domestic product and during this last week in February, unexpected surges in the service sectors indicates that a recession has indeed been avoided.

The IMF (International Monetary Fund) continues to forecast the UK as the only major economy to shrink though. The is due to, as we all know, September’s infamous mini-budget, but also the record number of job vacancies, currently 1.1 million.

According to Bailey, "what marks the UK out" is the rise in economically inactive workers (people aged 16-64 not seeking work) due to a rise in long-term sickness (predominantly long-covid) or inability to work whilst awaiting health treatments . Meanwhile, in other countries, the number of economically inactive people has fallen since the pandemic. Worker shortages create stagnant productivity levels.

Are we seeing any effects of this near-recession economy?

Unemployment

A shrinking economy typically means companies make less money, resulting in layoffs and a rise in unemployment. Many businesses had already closed or reduced opening hours due to unsustainable energy prices, Brexit trading issues and no savings-cushions after two years of covid-induced closures.

Yet contrary to expectations, unemployment rates are still lower than pre-covid and there are record job vacancies across the entire labour market.

The latter months of 2022 did see a small 0.2% unemployment increase to an estimated 3.7% overall, but we are in unchartered territory. Yes, we’re in a recession-like economy but unemployment rates are akin to a thriving economy due to our reduced labour force caused by a combination of, as mentioned, long-Covid, Brexit and failed economic policy (theguardian.com).

It’s still a job-seeker’s market.

Credit card and unsecured debt

During the 2008 recession, banks withdrew lending options at an eye-watering pace and showed reluctance to lend. Today however, credit options are abundant and the total amount of unsecured debt (credit cards, personal loans, car finance, overdrafts etc.) now exceeds £400bn, which soars beyond the £286bn peak in 2008.

It equates to a record high of £16,000 per household as people borrow more to meet higher living costs. In 2022, unsecured debt grew by 11%, or £80 million a day, the fastest growth in the past fifteen years.

Gross new consumer lending excluding student loans in the United Kingdom (UK) from January 2007 to December 2022

Statista.com

The average age group for unsecured debt in the UK is 25–34. With interest rates on borrowing going up, the priority will be paying off debt rather than saving for a property deposit, reducing the number of first-time buyers (FTB) who would have been ready to purchase in 2023.

However, 2023 will scoop up the FTBs who didn’t get swept away in the buying frenzy of the last two years and will be prepared to transact in this year’s more settled market.

Repossession rates

Industry-wide predictions are of a rise of home repossessions throughout 2023.

Households with fixed rate mortgage deals due to expire soon will be rolling off sub 1% rates onto anything from 4-6%, marking a quadrupling in cost. Combined with inflation, ludicrous energy bills, and an estimated 2.6% fall in real-term wages people can’t make ends meet, mortgage payments are missed and lenders take action.

The latter half of 2022 has seen increases in home repossessions, although rates are still significantly below pre-covid levels.

According to UK Finance, Q3 last year had 744 mortgage repossessions by county court bailiffs compared to 390 in the same period in 2021 and 15% higher than the three months previous. Mortgage repossessions orders (the legal document informing homeowners that their lender can take possession) rose to 2,491 – up from 1,229 last year, an increase of more than 100%.

However, these increases can mostly be attributed to FCA measures to suspend repossession proceedings during the pandemic. There were only 10 repossessions from April 2020 to March 2021, so courts are clearing the backlog.

But in the face of a cost-of-living crisis more repossessions are inevitable and lenders have begun increasing their customer service teams in anticipation of more borrowers going into arrears and defaulting over the next two years (financialreporter.co.uk)

Home repossessions are a last resort for lenders and there has been a more proactive approach to help struggling borrowers since 2008's spike and the pandemic measures. Also, the Chancellor recently met with lenders to discuss what support they can provide (gov.uk). As the government hangs on by its fingernails both economically and politically, soaring repossession rates won’t be palatable ahead of the 2024 General Election. So potentially, government intervention will restrict lenders repossession abilities again, a power demonstrated during the pandemic.

What it means for the housing market

Truthfully, this is the market investors and developers have been waiting for: house prices are correcting, sellers are negotiating and auction opportunities are increasing.

Also, other than a brief reactive withdrawal of some mortgage products in September - October 2022, lenders are fully open for business (a very different scenario to the 2008 recession).

There are currently 4,341 mortgage products to choose from, up nearly 700 from January 2023 (Moneyfacts Report, Clyde Property).

At Brickflow, the past three months have been some of our busiest and every lender and developer we are speaking to are busy, with developers being keen to capitalise on lower priced sites.

Auction activity

An increase in house repossessions will generate more activity in property auctions, and whilst there’s little data for this year, auction lots mostly corroborate market forecasts. Auction House had 40 lots on offer in Scotland in January 2023 in comparison to 16 in March 2022. In London, there were 191 lots offered in Dec 2022 compared with 150 in March. Of course, not every lot is a bank repossession, but gauging auction activity is a good indicator – we’ll check back in with the stats in March’s industry insights.

Reduction in prices

House price inflation has indeed slowed, with both Nationwide and Zoopla’s house price index showing prices 3–4% lower than last year’s peak. The outlier is Rightmove, who reports a 0.9% increase in average asking price during January 2023.

That said, the UK’s intrinsic housing shortage means demand for homes is still strong and a significant reduction in property prices is not anticipated.

Rightmove shows prospective buyer inquiries is up by 55% from the two weeks before Christmas, the biggest New Year bounce since 2016. Overall, buyer interest is back in line with pre-pandemic years.

This isn’t really a surprise – the past two years were exceptional for the housing market and a phenomenal kind of herd mentality saw homebuyers putting in extreme overbids to secure a property.

Now, higher mortgage rates and living costs combined with low consumer confidence has brought activity levels back to normal and there’s a more reserved approach during the negotiation stage.

But this is a market correction rather than a downward spiral of house price depreciation.

Nonetheless, when money is expensive to borrow it leads to fewer buyers financing, or waiting until they’ve accrued a larger deposit to help reduce the monthly mortgage, so transaction volumes will continue to slowdown.

For some perspective on the recent price drop, the largest reduction the UK housing market has ever seen was 13.4% over 12 months from January 2008. Increases far surpass even the most significant historic price drops; 2002 saw a 28.8% rise and 14.4% from January 2020 – December 2021. So any price drops in 2023 are likely to be smaller in comparison and could be seen as a short-term correction before continuing on the market’s natural ascent.

How to navigate the new market and what’s doing well

It’s unlikely that the residential market will regain much momentum in the very near term as economic headwinds are temporarily set to remain strong..

Any developer will be aware that if they’re buying sites now, they are most likely not delivering those properties to market until the end of 2024 or the first part of 2025 at the earliest. Higher interest rates alongside labour and material price inflation have undoubtedly made it harder and more expensive to build new homes, and less savvy investors may put their projects on hold. But build cost inflation has fallen dramatically and the reduction, or price correction on site acquisitions will rebalance profit margins for developers.

The key for developers with projects nearing completion is acknowledging that buyers have less buying power after the BOE’s rate hikes, so price according to today’s market and not the glittering prices of the previous two years.

The affordability factor is the biggest concern for buyers right now, particularly those just starting on the property ladder.

For developers who are happy to travel to find investment opportunities, it’s worth bearing in mind regional differences. In the North East, Scotland and Wales, property prices are below the national average and house price to earnings ratios (HERPs) are significantly lower. Hence demand and sales are holding up better in these regions. Market conditions are comparatively weaker in the South East, South West and East Midlands, where higher prices are exacerbating affordability pressures.

Lower HERP regions FTBs have their 20% deposit ready long before their counterparts in London, assuming both are saving 15% of their take-home pay (Nationwide HPI).

Source: Nationwide HPI

In other words, the market for first time buyer properties (one-two bed flats) is stronger in regions with greater affordability. This is also reflected in average selling times throughout January: Scotland is 36 days, whilst London is 67 (rightmove.co.uk).

The demand for flats has grown UK wide though, with the first few weeks of 2023 seeing 27% of new buyers looking for 1-2 bedroom flats, up from 22% a year ago. Contrastingly, demand for 3-bed houses has fallen by 5% (although they’re still the most in-demand homes across the UK). This is partly buyers being more value-conscious, but it’s also being driven by increasing rental costs.

In London, 1 and 2-bed flats account for 49% of demand, up from 42% a year ago, as more people return to city working post-pandemic. More affordable towns and suburbs adjacent to London have some of the biggest increase in demand for flats, such as Slough, Watford, Guildford and Dartford where the relative price differential is attracting part-remote London workers.

High value property

According to agents, although the volume of new inquiries is much below last years’ levels, the £1.5 million-plus market is showing resilience to interest rate rises. Alex Lyle, Director of Richmond estate agency Antony Roberts, says: “prices are holding…as a significant percentage of buyers within this section of the market do not require mortgage finance. We have seen three sealed bids since the start of the year, with two leading to record-breaking off-market sales. Both were cash buyers.” (thenegotiator.co.uk)

Buy-to-let market

For private buy-to-let investors, it’s a bit like the best of times and the worst of times.

The past 12 months in the rental market was nothing short of crazy, with agents reporting over 900 inquiries per flat listing. Demand like that will be hard to beat, but the number of renters invariably goes up during a recession as less people can afford to buy. Supply and demand issues have already risen the UK average (including London) rental price to £1172 PCM.

Nonetheless, landlords face hefty mortgage hikes, and legislation that will further squeeze profits: from 2025 private rental properties must have minimum EPC’s of C, and in Scotland, in what seems like a bid to reduce the private rental sector to ashes, landlords have been unable to lawfully evict non-paying tenants for up to 6 months.

Many landlords might opt out of the market altogether. Additionally, in order to refinance, buy-to-let mortgage holders have to meet affordability criteria based on a minimum interest coverage ratio (ICR). A report by credit rating agency Moody’s suggests that with the soaring interest rates, as many as 30% of those with BTL mortgages will be below their minimum ICR requirements despite higher rental prices.

All of which leads to a spiral that exacerbates the shortage of rental properties and further drives prices upwards.

Faced with shrinking profit margins, tricky legislations and possibly zero or negative capital growth in 2023, net yield will be the all-important driver for the BTL market. But if the yields stack up, the demand for rental housing indicates that investing time, money and effort into improving the private rental sector housing stock makes even more sense now, both commercially and socially.

Other considerations

We can’t finish our monthly roundup without mentioning Brexit - last month was the three-year anniversary of the UK leaving the EU..

As we all know, the main impact on the housebuilding sector has been logistical hurdles, mounting material costs and a big reduction in the construction labour force.

Increased delays, costs and difficulties in obtaining construction materials has led to a surge in demand for warehousing. As a result, the industrial construction sector exceeded all records in 2022, with £15.4bn of planning approved, far surpassing 2021’s £11.7bn and doubling the levels of 2020 (Barbour ABI).

At Brickflow, we’ve already seen requests for the funding of warehouses sky rocket in recent months, with many traditional residential developers turning their attention to commercial property whilst market conditions are good. Logically, the closer to a port, the better for any would-be warehouse developer.

As we said in January’s Industry Insights, 2023 undoubtedly holds spectacular opportunities for developers who are looking to buy, or can adapt un-started projects to meet rental demands or affordable housing stock.

That’s it for February. Check in again next month for more updates on what we’re seeing and hearing through our conversations with brokers, property entrepreneurs, estate agents and lenders.

Brickflow is a software company only. Our product is designed to be used by experienced property finance professionals to source and apply for development finance loans.

Property investors can search the finance market by using our software to model and analyse their deals, but they cannot apply for finance through Brickflow without a Broker. Speak to your Broker about Brickflow or ask us to connect you with a Broker.

Property development carries risk, including variables beyond the developer’s control. A property development loan is debt and should be procured with caution.

Brickflow does not provide information on personal mortgages, but your home and other assets are at risk if you provide a personal guarantee for a corporate loan.

The inside track on property development in January 2023.

The inside track on property development in March 2023.

The inside track on property development in September 2023.